Conflict freezes Dubai, Israel diamond trade as 1-carat prices fall

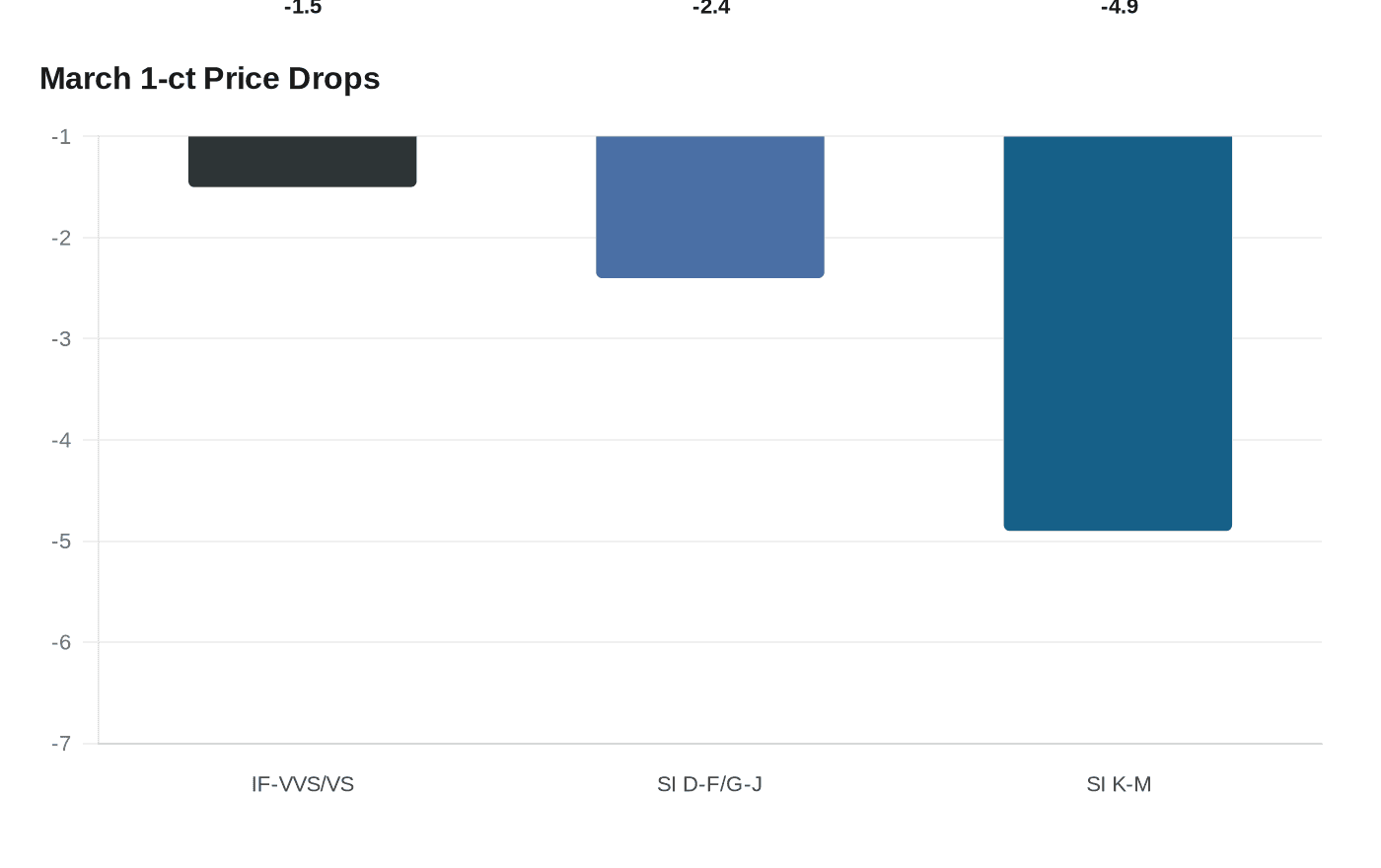

RapNet says the US–Israel–Iran conflict "effectively shut down trading in Dubai and Israel," as 1-carat D–F and G–J prices fell about 1.5% and SI grades fell faster in March.

RapNet characterizes March’s market shock bluntly: the US–Israel–Iran conflict "effectively shut down trading in Dubai and Israel," forcing rough tenders to relocate to Antwerp and creating immediate disruption for Indian manufacturers that depend on those corridors. RapNet’s April Diamond Pulse reports D–F and G–J 1-carat diamonds in IF–VVS and VS clarities fell roughly 1.5% in March, SI clarities across those colors declined about 2.4%, and K–M colors saw steeper drops, with SI down 4.9% in the month.

The operational impact was concrete and fast. Koin International postponed its Dubai rough tender originally set for March 3–5 to March 9–11, citing the "cancellation of flights into the United Arab Emirates," while Trans Atlantic Gem Sales delayed a Dubai start that had been scheduled for March 1–5 so the company could prioritize staff and customer safety. Dubai Multi Commodities Centre moved to remote working under executive chairman Ahmed Bin Sulayem’s oversight, and the Israel Diamond Exchange in Ramat Gan placed its trading floor into emergency mode with only essential services operating. With Dubai and Israel frozen, buyers and sellers shifted lots and tenders to Antwerp.

The stoppages exacerbated existing inventory imbalances. RapNet’s listings show G–J colors accounted for 58.6% of the 1-carat segment, concentrating supply where demand is already mixed; RapNet also notes stronger appetite for 2-carat-plus high-quality rounds and elongated shapes even as sub-2ct goods linger. At the retail end, Signet posted $6.8 billion in fiscal 2026 sales and its CEO pointed to continuing growth in demand for higher-quality natural diamonds, a retail signal that aligns with RapNet’s buyer-search behavior.

Supply-side shocks are now layered onto the trading freeze. Rio Tinto celebrated Diavik’s final day of production on March 26, 2026, after 23 years and more than 150 million carats; Rio Tinto says closure activities will extend to 2029 and that Diavik’s final rough will be polished and sold through 2026 and beyond. At the same time RapNet flagged De Beers’ decision to cut its sightholder list by 30% effective in July and reported Alrosa’s 6–9% rough price increases on 2–10 carat goods since January, moves that tighten supply for larger stones even as 1-carat pricing softens.

Takeaways for buyers: expect availability to shift as tenders move to Antwerp and Dubai/Israel operations pause, creating delivery timeline uncertainty documented by postponed Koin and TAGS tenders; expect near-term price volatility in 1-carat goods, especially SI and K–M colors where RapNet shows the steepest March declines; and watch supply-side changes from Diavik’s March 26 closure and De Beers’ sightholder cut, which tighten mid- and long-term supply for higher-carat goods.

Practical checklist for this month: ask your jeweler whether a stone was part of Antwerp or Dubai tenders and confirm current lead times given the Koin and TAGS postponements; request written price hold terms and consider locking a fixed quote for 30 to 90 days if the retailer offers it, because RapNet data shows rapid monthly swings in 1-carat pricing; insist on stone paperwork, lab reports, and chain-of-custody detail for any Diavik-origin goods given the mine’s final production on March 26, 2026; and expect logistical delays tied to flight cancellations and shifted tenders while Antwerp handles displaced rough volume.

The market is cautious and selective: RapNet’s overview frames March as a month of interrupted corridors and focused buying for immediate needs, leaving 1-carat buyers to weigh faster price moves against tighter supply signals for larger stones.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?