Grand Traverse Commissioners Confront Treasurer Over Delayed Financial Reconciliations

Grand Traverse County commissioners confronted Treasurer Jamie Callahan as auditors are due to arrive April 20 and a second consecutive formal finding on missed reconciliation deadlines looks nearly certain.

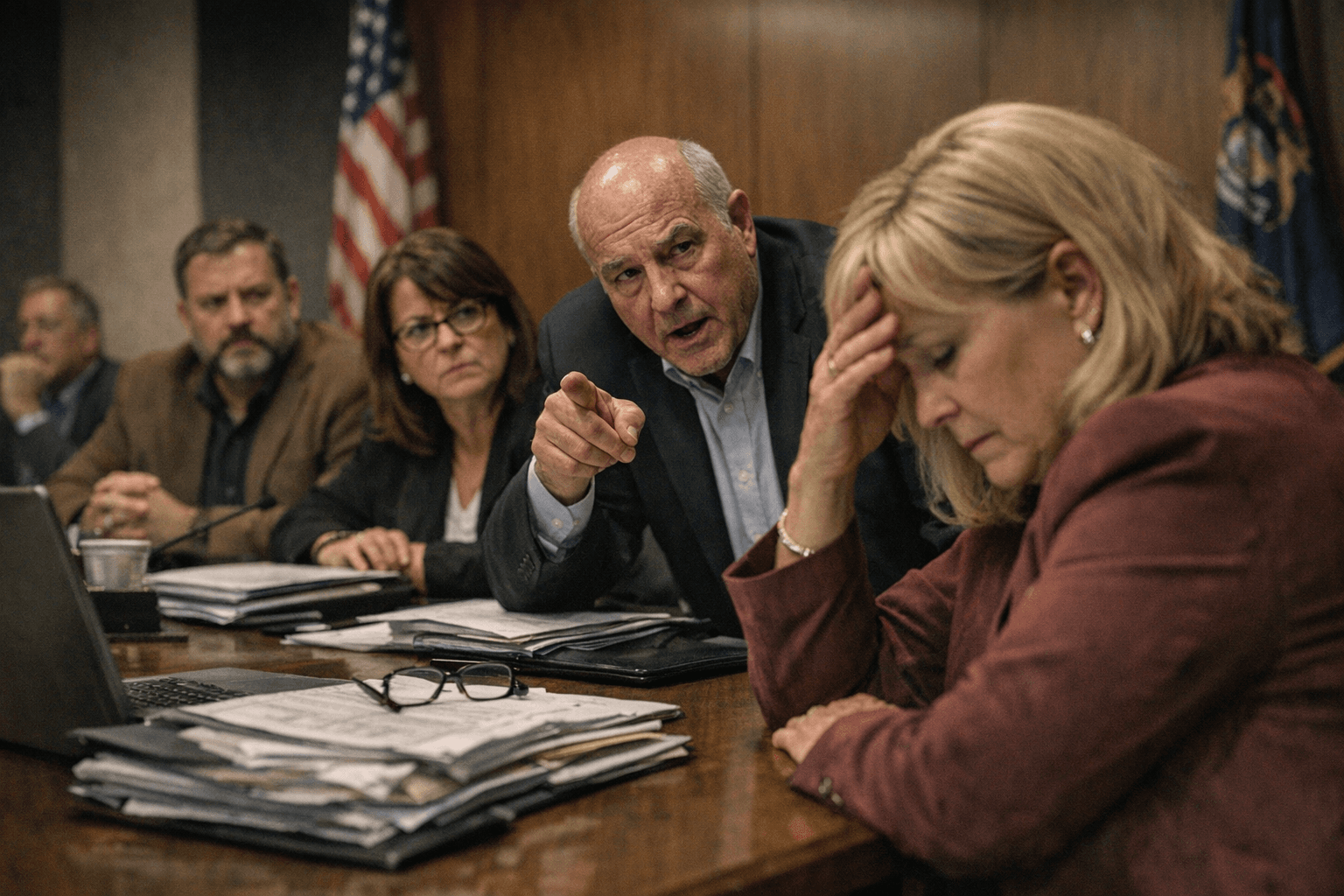

With county auditors scheduled to arrive in Traverse City on April 20, Grand Traverse County Treasurer Jamie Callahan sat before the Board of Commissioners on Wednesday and acknowledged his office will almost certainly receive the same formal written citation it received after the 2024 audit: failure to reconcile bank accounts within 30 days.

That citation, issued to a county office that manages nearly $170 million in annual receipts, has not been corrected in the nearly five months since the treasurer's office was told to fix it. County Financial Director Dean Bott told commissioners the verdict on the coming 2025 audit was already clear. "I believe we will receive the same audit finding in 2025, because we were not able to reconcile the accounts within the 30 days that they recommended," Bott said.

The 30-day standard is not arcane: it refers to the basic monthly process in which the county's accounting software balances against its actual bank accounts, catching errors, discrepancies, and missing entries before they compound. The treasurer's office missed that window repeatedly through 2025 and has not yet completed first-quarter 2026 reconciliations. Three final journal entries also still need to be made to formally close out the 2025 fiscal year.

Commissioner TJ Andrews, who said the board has been raising this concern since at least last September, did not conceal her frustration. "I'm a little Groundhog Day here," she said. "We had this precise conversation. We were told repeatedly we're imminently getting on track, and we are now in April, and we're still not on track." In a separate exchange, Andrews framed the longer pattern directly: "I feel like this board has been told repeatedly, 'We're imminently getting on track. We're almost there.' We are now in April and we're still not on track, and it becomes an oversight challenge on our part."

Callahan offered a partial defense. He said his office brought in outside assistance from Gratiot County to help close the gap, and that the underlying numbers are sound: ledger balances and cash balances now match for 2025. "From our reconciliations perspective, which is the most important part, we are completely reconciled," Callahan said. "Our ledger and our cash match. We don't have any outstanding reconciliations right now for 2025." What auditors will weigh, commissioners noted, is not just whether the numbers ultimately balanced, but whether they were reconciled on time as required. Timing is the finding.

That distinction carries real-dollar consequences. Grand Traverse County approved a $27.8 million plan in March to build a new 911 center and emergency operations facility, along with a resolution authorizing up to $30 million in bonds to fund it. Bond markets assess an issuer's audit history and internal controls when pricing debt. A pattern of repeat findings can translate directly into higher borrowing costs or tighter terms on that financing. One formal audit finding is explainable. Two consecutive ones signals a systemic failure, a distinction Callahan's own financial director did not dispute.

Commissioners signaled they are watching for visible progress before auditors walk in, and left open the possibility of additional oversight steps or staffing changes if the backlog is not resolved. Bott attributed the delays in part to staffing shortages in the treasurer's office.

What to watch: Auditors arrive April 20, giving the treasurer's office less than two weeks to close the three remaining 2025 journal entries and demonstrate the kind of internal discipline that prevents a third consecutive finding. The county's first-quarter 2026 reconciliations remain outstanding. Commissioners have also asked for a written catch-up plan with specific timelines, a document that will be a public benchmark when the board reconvenes. Whether Callahan can satisfy both the auditors and the board before that deadline will determine whether this dispute moves from frustrating pattern to formal governance problem.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?