$15,000 in a money market account can still earn meaningful interest now

A $15,000 money market account is still producing real cash, but the gap between average and top-tier rates is wide enough to matter.

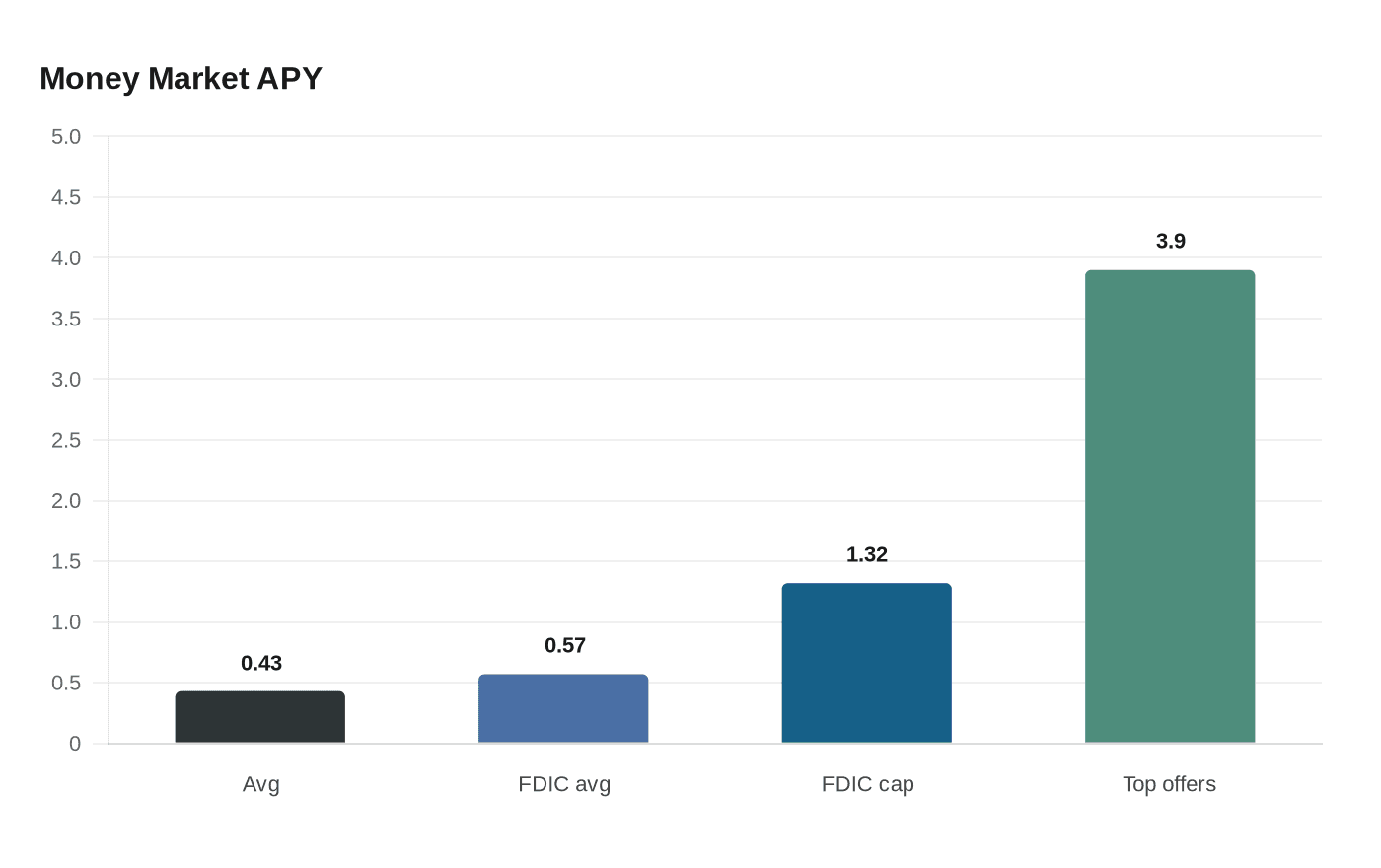

The return on $15,000 depends far more on the rate than the label

A money market account is not a place to park cash and ignore the math. At today’s average yield of 0.43% APY, a $15,000 balance would bring in about $64.50 a year, which is real interest but not much buying power. At the FDIC’s national average money market rate of 0.57%, that same balance would earn slightly more, while the FDIC’s 1.32% rate-cap benchmark would lift the annual return to about $198.

The spread gets much more dramatic at the top of the market. Bankrate says some of the best money market accounts pay more than nine times the average, with offers above 3.9% APY. On $15,000, that works out to about $585 a year. That difference is the entire story for anyone weighing where cash should sit right now: the account type matters, but the rate tier matters much more.

What the current rate backdrop means for savers

The Federal Reserve kept its target range for the federal funds rate unchanged at 3.5% to 3.75% at its March 18, 2026 meeting. That matters because deposit products tend to move with the broader interest-rate environment, even if they do so unevenly and with delays. When the policy rate stays elevated, cash is still capable of earning something meaningful, but banks do not all pass that value through in the same way.

That is why a money market account can look decent on paper and still underperform what the market is actually offering. The gap between the average 0.43% APY and the 3.9% APY top end is not a rounding error. It is the difference between a basic parking spot for cash and a genuinely competitive short-term home for savings.

Why the account still has a role

Money market accounts are appealing because they can combine yield with convenience. Unlike many regular savings accounts, they may offer check-writing privileges or debit-card access, which makes them useful for people who want a reserve fund that is still fairly liquid. For an emergency fund, a home-repair stash, or money set aside for a tax bill, that flexibility can matter as much as the headline APY.

Safety also remains a major draw. FDIC deposit insurance protects money market deposit accounts at FDIC-insured banks up to $250,000 per depositor, per insured bank, per ownership category. For many households, that makes the account a low-friction place to keep cash without taking market risk. The key question is not whether the money is protected, but whether the yield is high enough to justify keeping it there instead of in a better-paying cash option.

The practical consumer reality check on $15,000

A $15,000 balance earning $64.50 a year at 0.43% APY is modest compensation for parked cash. Even the FDIC benchmark of 1.32% only gets that return to about $198 a year, which is better but still limited once inflation and taxes are taken into account. The top end changes the picture: $585 a year on the same balance can start to feel meaningful, especially for households trying to make idle cash work harder without taking investment risk.

That is the consumer test now. If your money market account is paying close to the national average, it is mostly a convenience product. If it is paying near the top of the market, it becomes a serious contender for liquid cash. The difference can be hundreds of dollars a year on a balance that is large enough to matter but small enough to remain typical for many households.

How it compares with high-yield savings, CDs, and Treasury bills

The most important comparison is not just rate, but access. High-yield savings accounts usually compete directly with money market accounts for cash that needs to stay available, while CDs generally trade liquidity for a fixed rate over a set term. Treasury bills also sit in the short-term cash conversation, especially for savers who are willing to tie money up for a brief period in exchange for a government-backed instrument.

That means the right choice depends on what you need the money to do. If you may need to write checks or tap a debit card, a money market account can still win on convenience. If you want a set-and-forget return and do not need daily access, a CD may fit better. If you are chasing the strongest cash yield available, Treasury bills and top money market accounts often enter the same decision set, but the best choice depends on how soon you may need the money.

What to check before opening or keeping one

The advertised APY is only part of the story. Some money market accounts require larger balances to unlock the best rates, so a teaser yield may not be available unless you meet a minimum balance threshold. That makes it important to know whether the rate you see is the rate your balance will actually receive.

- Confirm the APY that applies to your balance tier.

- Check whether the account has minimum balance rules.

- Look at withdrawal access, including check-writing and debit-card features.

- Make sure FDIC insurance applies through an insured bank and that your total deposits stay within coverage limits if you use multiple accounts.

A quick checklist helps:

Bottom line

For a $15,000 balance, a money market account can still earn meaningful interest, but only if you land at the right rate. At the average, the cash return is small. At the top end, it becomes much more noticeable, and that is enough to make money market accounts worth a second look for savers who want liquidity, insurance, and a better shot at keeping pace with the current rate environment.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?