Elevance Health lifts profit forecast as medical costs stabilize

Elevance raised its 2026 profit outlook as claims trends eased, but Medicaid pressure, network changes and a CMS dispute still threaten patients and earnings.

Elevance Health lifted its 2026 profit forecast after claims trends improved, but the upside came with a familiar catch for patients: tighter medical-cost control, especially in Medicaid, is still shaping where people can go for care and how quickly they can get it.

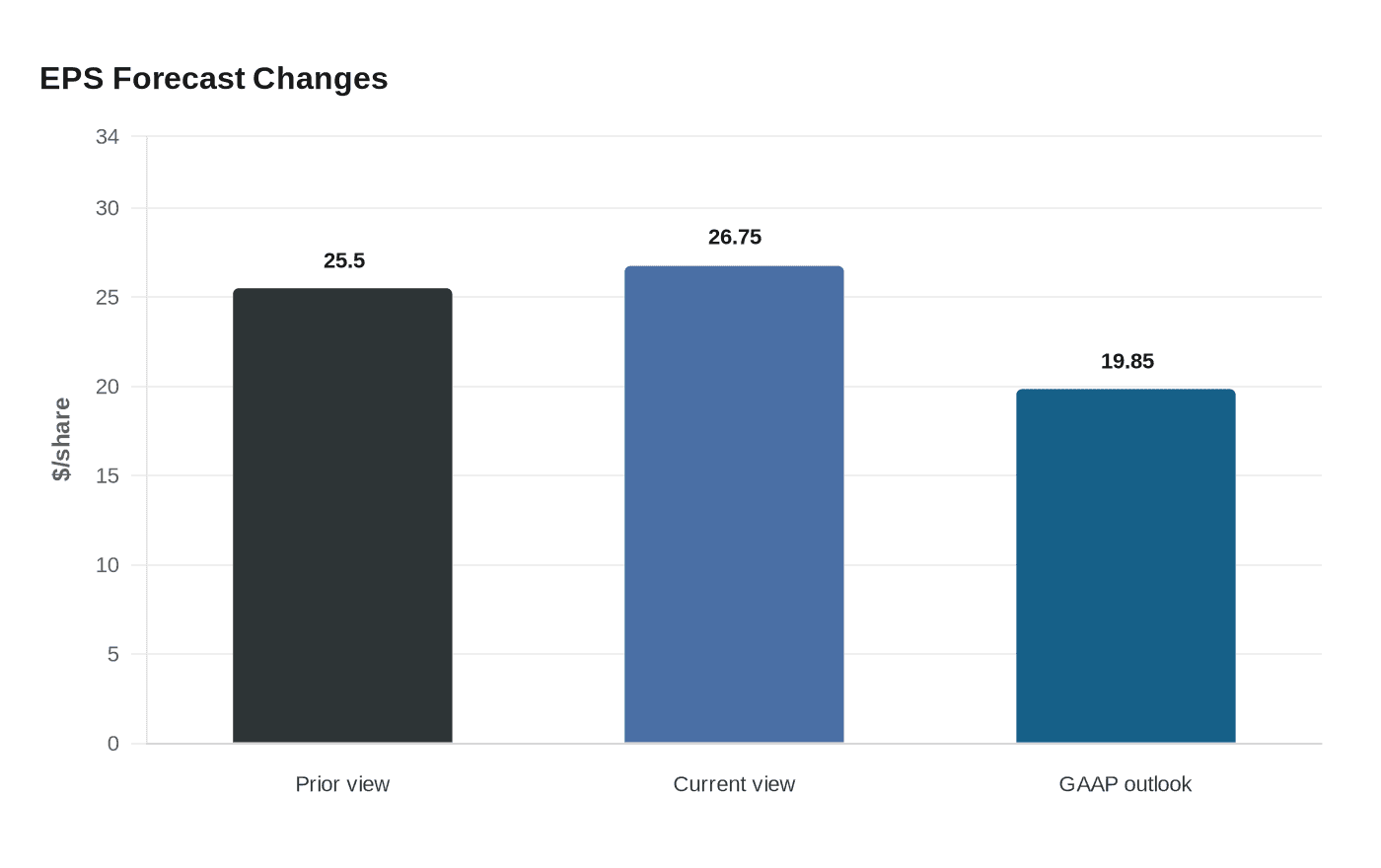

The Indianapolis-based insurer said adjusted diluted earnings per share should reach at least $26.75 this year, up from a prior view of at least $25.50. The company also trimmed its GAAP diluted earnings outlook to at least $19.85 because of the estimated financial impact of a Medicare Advantage data-reporting dispute with the Centers for Medicare & Medicaid Services. Even as it raised profit guidance, Elevance said full-year operating revenue would decline by a low-single-digit percentage range.

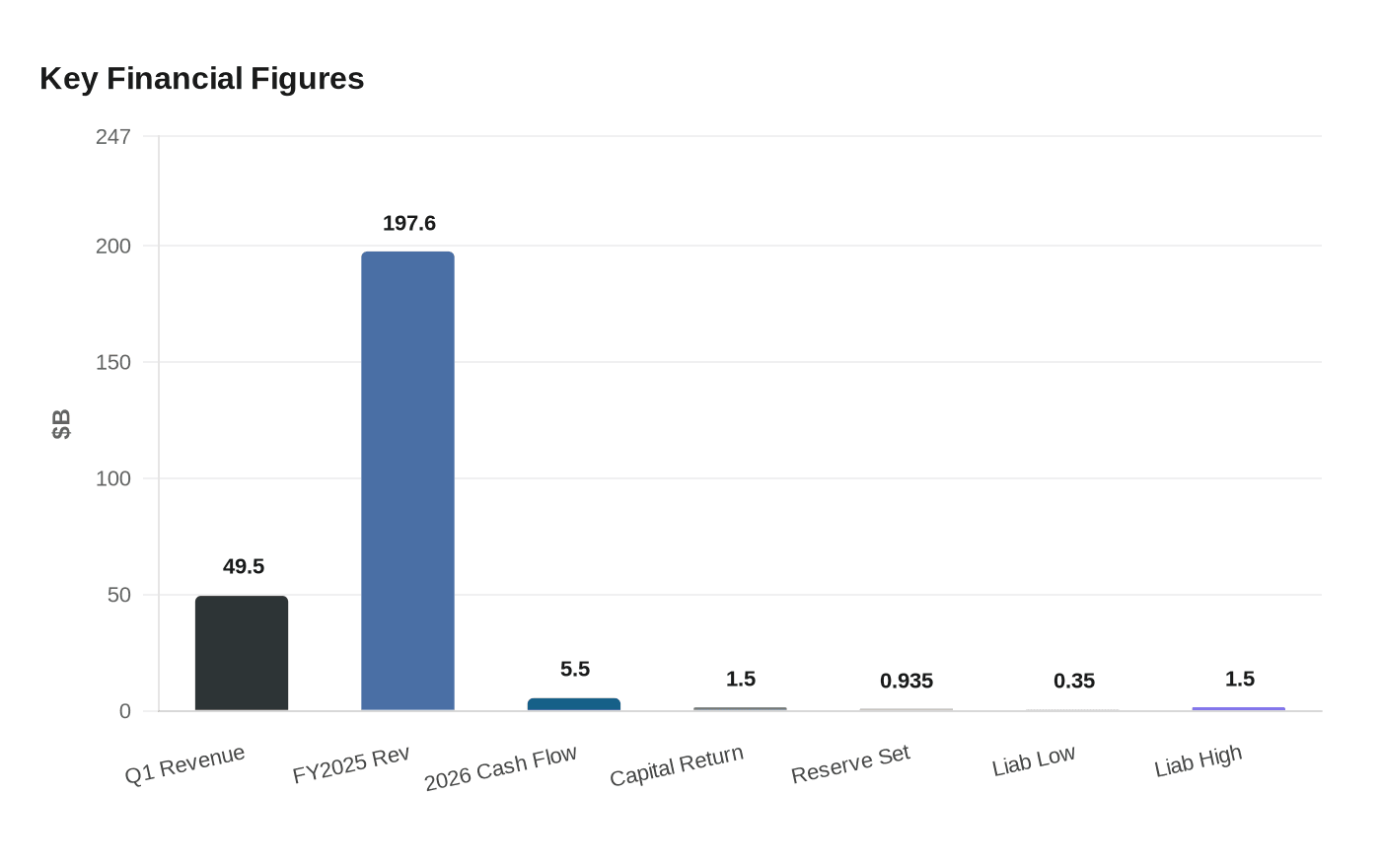

First-quarter operating revenue reached $49.5 billion, up 1.5% from a year earlier, and adjusted diluted earnings per share came to $12.58. Elevance said that result included about $1 per share from non-recurring investment income. The company’s benefit expense ratio rose to 86.8%, up 40 basis points from a year earlier, reflecting elevated medical-cost trend concentrated in Medicaid. Operating gain fell to $2.1 billion from $3.2 billion a year earlier.

Gail K. Boudreaux, Elevance’s president and chief executive, said the quarter reflected “underlying business strength and improving claims experience” and that the company’s actions were driving more consistent performance. Those actions include deliberate changes to health plans and exits from select locations as Elevance tries to manage pressure in Medicaid, a strategy that can protect margins but can also leave consumers with fewer choices or more friction when they seek care.

That tension sits at the center of the managed-care market. Insurers have been battling higher use of services in government-backed plans, as well as stubborn spending on behavioral health care and specialty drugs. Elevance’s improved outlook suggests it has more visibility into the rest of the year, but not that the cost problem has disappeared. In January, the company had already warned that 2026 would be a year of execution and repositioning across Medicaid, Medicare Advantage and Obamacare plans.

The numbers also show how quickly the story can turn. Elevance reported a 93.5% benefit expense ratio in the fourth quarter of 2025 and 90.0% for the full year, after revenue reached $197.6 billion. Now it expects operating cash flow of at least $5.5 billion in 2026 and returned $1.5 billion of capital to shareholders in the first quarter, signs that management still has room to reward investors even as it trims risk.

But the CMS matter remains a major overhang. The company said it had set aside $935 million related to the issue, with a possible liability range of roughly $350 million to $1.5 billion. CMS had warned in February that Elevance could face sanctions, including a halt on new Medicare Advantage enrollment, if the data problems were not fixed. The agency later extended the deadline to May 30, 2026. For now, Elevance is showing that better pricing and tighter controls can lift profits, even as many patients still feel the burden in narrower networks, more prior authorization and higher out-of-pocket costs.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?