$500,000 Retirement Savers Face IRS Rules on Required Withdrawals

At age 73, a $500,000 account can force an $18,868 withdrawal, and the IRS penalty for missing it can quickly turn a planning error into a costly tax bill.

How a $500,000 retirement account turns into a required withdrawal

A $500,000 retirement account is not fully under the saver’s control once IRS required minimum distribution rules kick in. For traditional IRAs, SEP IRAs, SIMPLE IRAs and many employer plans, withdrawals generally begin at age 73, and the government’s message is blunt: retirement funds are not meant to stay sheltered forever. The account owner may take more than the minimum, but not less, and the distribution is usually taxable income unless part of it was already taxed or can be received tax-free.

How the IRS calculates the minimum

The formula is straightforward, even if the implications are not: take the account balance from the end of the prior calendar year and divide it by the IRS distribution period from the Uniform Lifetime Table. For most account owners, that table is the one that applies. If the sole beneficiary is a spouse who is more than 10 years younger, a different table may be used, which can lower the required amount.

At age 73, the Uniform Lifetime Table uses a distribution factor of 26.5. That means a $500,000 account produces a minimum required withdrawal of about $18,868 for the year, using the basic IRS formula. The number is not arbitrary. It reflects a government attempt to pace withdrawals over life expectancy rather than let tax-deferred money sit untouched for decades.

When the first RMD starts

The first required withdrawal is generally due by April 1 of the year after the saver reaches age 73. After that, the deadline shifts to December 31 for each later year, which can create a trap for retirees who delay the first one. If someone reaches 73 in 2024, the IRS says the first RMD is due by April 1, 2025, based on the December 31, 2023 balance, and the second RMD is due by December 31, 2025, based on the December 31, 2024 balance.

That timing matters because taking the first RMD in the next calendar year can mean two taxable withdrawals in the same year. For many retirees, that creates a real planning fork: take the first required amount by April 1 and potentially crowd income into one tax year, or take it before year-end and avoid stacking two RMDs in the same calendar year. The IRS rule itself does not change, but the tax bill often does.

Which accounts are covered, and which are not

The lifetime RMD rule applies to traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k) plans, 403(b) plans, 457(b) plans, profit-sharing plans and other defined contribution plans. Workplace plan participants can sometimes delay RMDs until retirement, but that exception does not help a 5% owner of the sponsoring business. The IRS also says Roth IRAs and designated Roth accounts in 401(k) or 403(b) plans are generally not subject to lifetime RMDs for the original owner.

There is an important inheritance catch. Beneficiaries of Roth IRAs and designated Roth accounts are subject to RMD rules, even though the original owner is not. Inherited accounts also follow separate rules and tables, which means a family member stepping into the account often faces a different distribution timetable than the person who built the balance.

What happens if you miss it

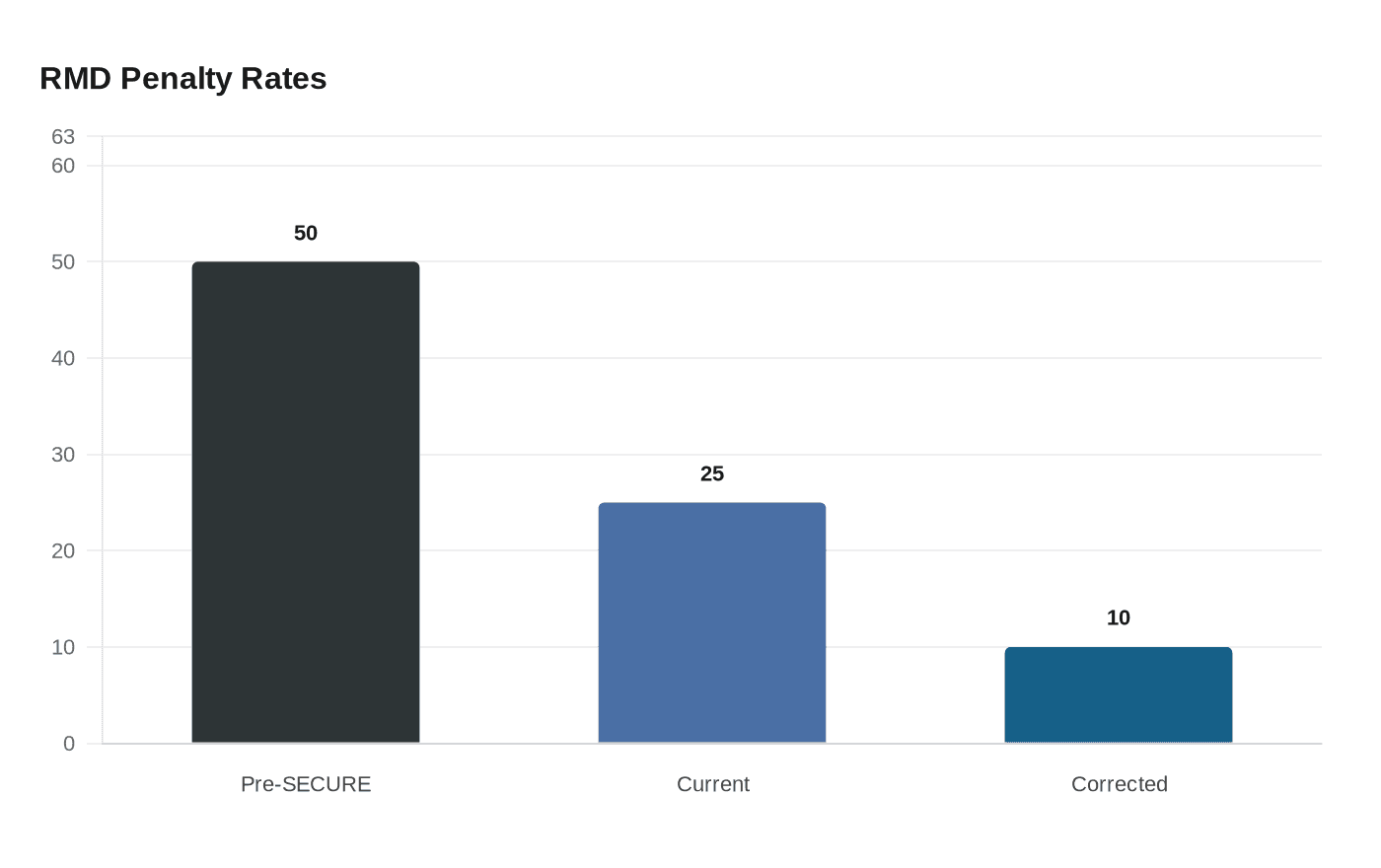

Missing an RMD is expensive because the shortfall can be hit with an IRS excise tax. Under SECURE 2.0, the penalty was reduced from 50% to 25% of the amount not distributed, and in some cases it can be cut to 10% if corrected within two years. The IRS also told taxpayers in Notice 2024-35 that it would not assert an excise tax in 2024 for certain missed RMDs if specified requirements were met.

The tax damage is not limited to the penalty itself. The RMD is also generally included in taxable income, which means a missed withdrawal can create a second layer of trouble when the money is finally taken. The IRS says Form 5329 may be needed to report the excise tax, so the mistake can become a tax-return problem as well as a cash-flow problem.

Why inherited accounts are different

Heirs do not simply inherit the same schedule the original owner followed. For many defined contribution accounts inherited after deaths occurring after December 31, 2019, the balance generally must be fully distributed within 10 years, subject to exceptions for surviving spouses, minor children, disabled or chronically ill beneficiaries and certain beneficiaries who are not more than 10 years younger than the deceased owner. The IRS says these rules changed with the SECURE Act and now apply whether the owner died before, on or after the required beginning date.

That is why the RMD question is really two questions at once: how much must come out this year, and whose rules apply. For a retiree with a $500,000 account, the first answer is usually a formula driven by the prior year-end balance and the Uniform Lifetime Table. The second answer can change everything if the account is inherited, if the spouse is much younger, or if the money sits in a workplace plan with a retirement-delay option.

The decision point for retirees

The practical choice is not whether the IRS wants a withdrawal, because it does. The choice is how to meet the deadline while keeping taxable income, penalties and timing problems under control. For savers with a $500,000 balance, the math is large enough that even a small calendar mistake can turn into a four- or five-figure tax issue, which is exactly why the IRS has built a detailed system of tables, deadlines and penalties around these withdrawals.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?