6-month CDs still offer savers a sweet spot above 4% APY

A $35,000 CD at 4.25% APY earns about $736 in six months, but inflation cuts the real gain to roughly $76 before taxes.

A $35,000 six-month CD at 4.25% APY would earn about $736 and end at roughly $35,736, but 3.8% inflation leaves only about $76 of real purchasing power before taxes. The headline yield still looks appealing, yet the buying-power gain is thin once prices are taken out of the equation.

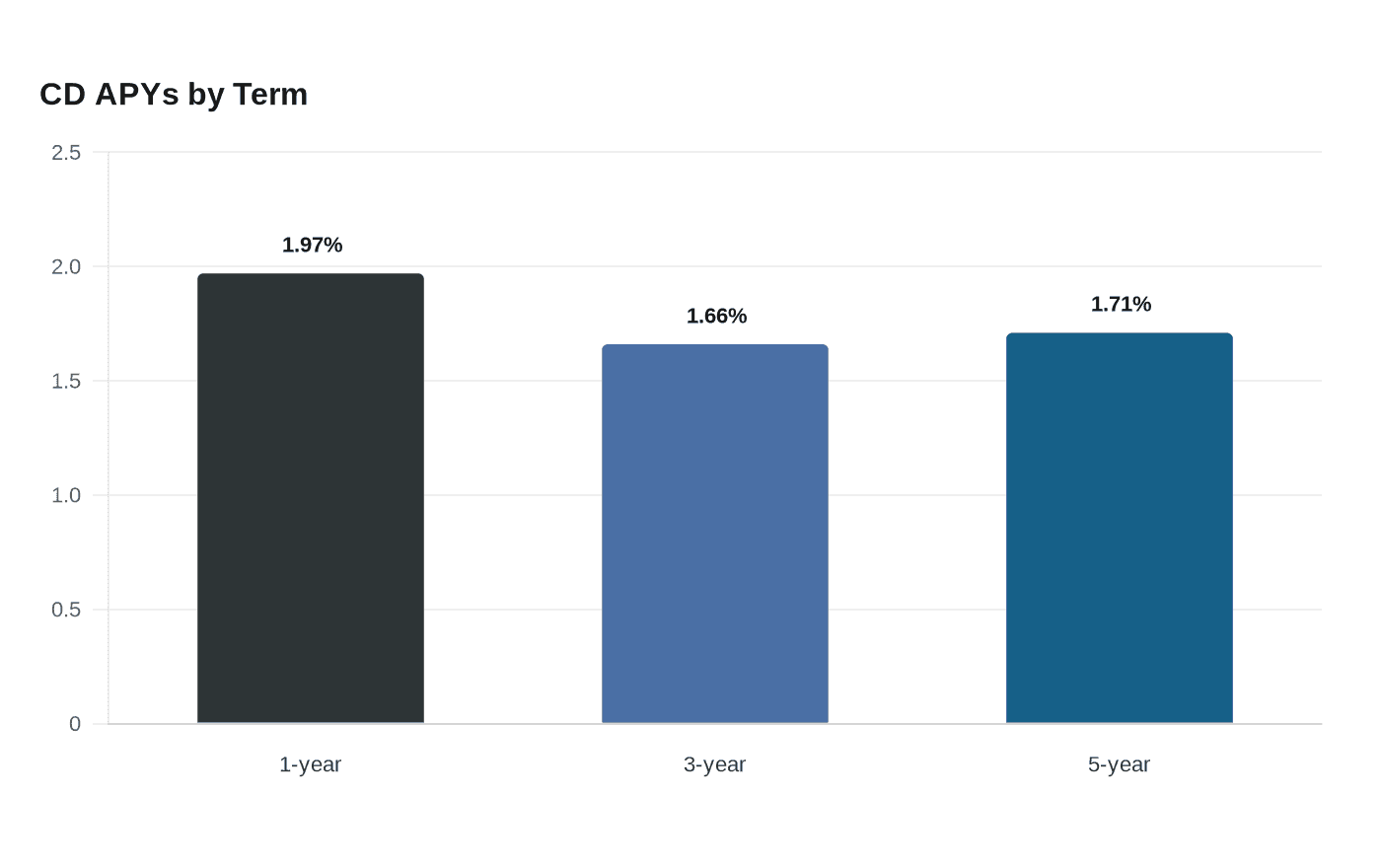

Bankrate said the best CD rates in June 2026 were still around 4% APY, with First National Bank of America, a Michigan-based bank offering CDs online nationwide, at the top tracked rate of 4.25%. National average APYs were 1.97% for 1-year CDs, 1.66% for 3-year CDs and 1.71% for 5-year CDs, and Bankrate said CDs are federally insured up to $250,000. Short-term CDs remain the part of the market where the strongest rates are concentrated.

The alternative is a high-yield savings account. Bankrate’s top savings rate was 4.10% at CIT Bank, which would generate about $710 over six months on the same $35,000, or about $51 in real purchasing power after inflation. That is only about $25 less in real gain than the top CD, while the national average savings account rate of 0.61% would produce only about $107 over the same period. The difference is flexibility as much as yield: the savings account keeps cash accessible, while the CD asks savers to give up that access for a small rate bump.

Treasurys tighten the comparison further. The Treasury’s 26-week bill rate was 3.80% on June 12, which would generate about $659 on $35,000 over six months, and the IRS says Treasury bill interest is subject to federal income tax but exempt from state and local income taxes. The FDIC’s May 18 rate-cap update showed a 6-month CD national deposit rate of 1.35% and said the cap framework is updated monthly; less well capitalized institutions cannot pay rates that significantly exceed prevailing market levels. FDIC-insured institutions reported $80.5 billion in first-quarter 2026 net income and a 1.26% return on assets, suggesting banks entered mid-2026 profitable and liquid enough to keep competing for deposits. For savers, that leaves a narrow question: whether a small, inflation-beaten premium is worth locking money up when liquid options come close.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip