Ares Management to Acquire Whitestone REIT in $1.7 Billion Deal

Ares Management agreed to buy Whitestone REIT at $19 a share in cash, a 12.2% premium crystallizing shareholder value from 56 Sun Belt neighborhood retail centers worth $1.7 billion.

Ares Management's all-cash bid for Whitestone REIT at $19 per share cuts to the core of where private real estate capital is finding value: neighborhood retail centers anchored by necessity-driven tenants in high-population-growth markets, priced at levels the public equity market has persistently underwritten below replacement cost.

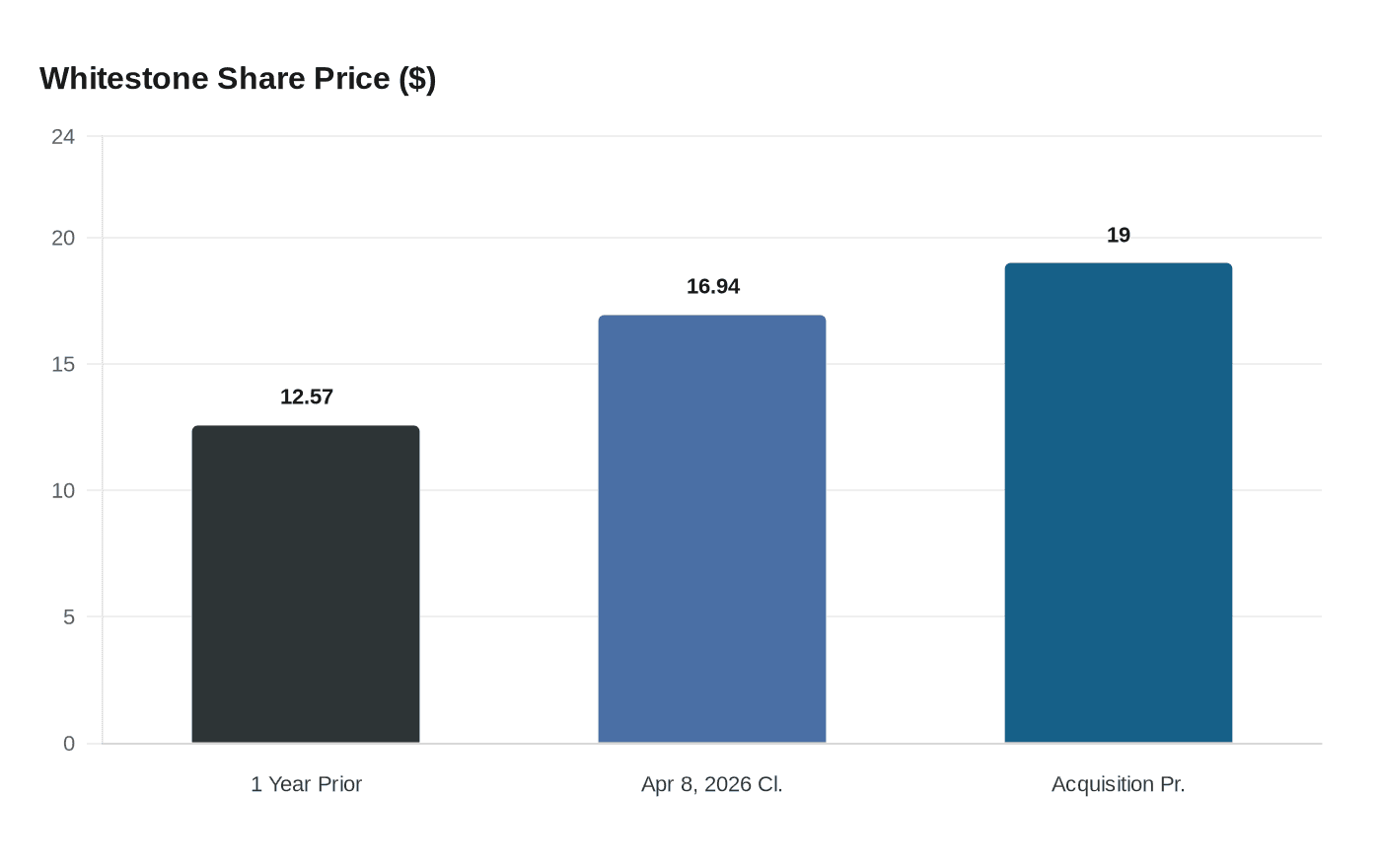

Ares Management Corp. and Whitestone REIT entered into a merger agreement that will allow Ares to take the REIT private in a $1.7 billion deal, with Ares acquiring all Whitestone common shares for $19.00 per share. Whitestone's shares had closed at $16.94 on April 8, themselves up nearly 35 percent from $12.57 a year prior, which made the premium look moderate in isolation. But the $19 price represents both a 12.2% premium to the April 8, 2026 close and a 26.5% premium to earlier pre-announcement price levels, reflecting the gap between where public investors had anchored their bids and what a well-capitalized private buyer was willing to pay to own the cash flows outright.

Before finalizing its agreement with Ares, Whitestone drew interest from multiple potential acquirers, including private equity giants Blackstone and TPG, which had shown acquisition interest in the company during March. Ares emerged as the winning bidder, with its real estate investment funds preparing to integrate Whitestone's property portfolio following deal closure. That competitive tension underscores the appetite private capital has built for mid-cap REITs with concentrated Sun Belt exposure and defensible tenant bases, even as borrowing costs remain elevated and public real estate valuations lag private market appraisals.

Whitestone is a Houston-based REIT focused on open-air neighborhood retail markets whose portfolio, as of March 2026, comprised 56 retail properties totaling approximately 3.9 million square feet in Phoenix, Austin, the Dallas-Fort Worth metro, Houston and San Antonio. The convenience-oriented merchandising strategy underpinning that portfolio is what CEO Dave Holeman cited directly in the deal announcement: "We believe Whitestone has shown the value of high-return smaller spaces occupied by a well-diversified mix of tenants." Those smaller-format leases, shorter in term and reset more frequently than big-box anchors, give the portfolio a degree of inflation sensitivity that long-duration retail cannot match, a feature private buyers are now paying a control premium to own.

The Ares acquisition of Whitestone is the firm's second public-to-private deal of the year; in January, Ares Alternative Credit Funds along with Makarora Management acquired Plymouth Industrial REIT in an all-cash deal valued at $2.1 billion at $22.00 per share. As of December 2025, Ares had nearly $623 billion in assets under management globally, giving it the capital and duration tolerance to absorb the refinancing and repositioning work that public REIT shareholders are unwilling to fund at current valuations.

Shares of Whitestone surged roughly 11% on April 9 when the deal was announced. Shares of Ares Management climbed modestly in premarket activity, even as broader S&P 500 futures declined approximately 0.4%.

On the advisory side, BofA Securities and JLL are acting as Whitestone's financial advisors, with Bass Berry and Sims serving as legal counsel; Citigroup Global Markets and Morgan Stanley are advising Ares, with Kirkland and Ellis handling legal work.

The parties anticipate finalizing the transaction during the third quarter of 2026, pending customary closing conditions, most notably shareholder approval. Following completion, Whitestone will delist and cease trading as a public entity on the New York Stock Exchange. For investors who held through the stock's 35-percent run over the prior year, the $19 cash offer crystallizes that gain without the risk of carrying a small-cap REIT through another rate cycle. For the broader market, the question is how many other neighborhood retail REITs, trading below private-market net asset value while sitting on inflation-resistant lease rolls in Sun Belt metros, are next on private capital's list.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?