Arif Habib Consortium Wins Rs135 Billion Purchase of PIA Stake

A consortium led by Arif Habib secured a 75 percent stake in Pakistan International Airlines for Rs135 billion, a deal that could reshape the national carrier and Pakistan’s privatisation agenda. The transaction promises immediate fiscal relief and private management, but regulatory approvals, debt treatment, and execution will determine whether the airline can be turned around.

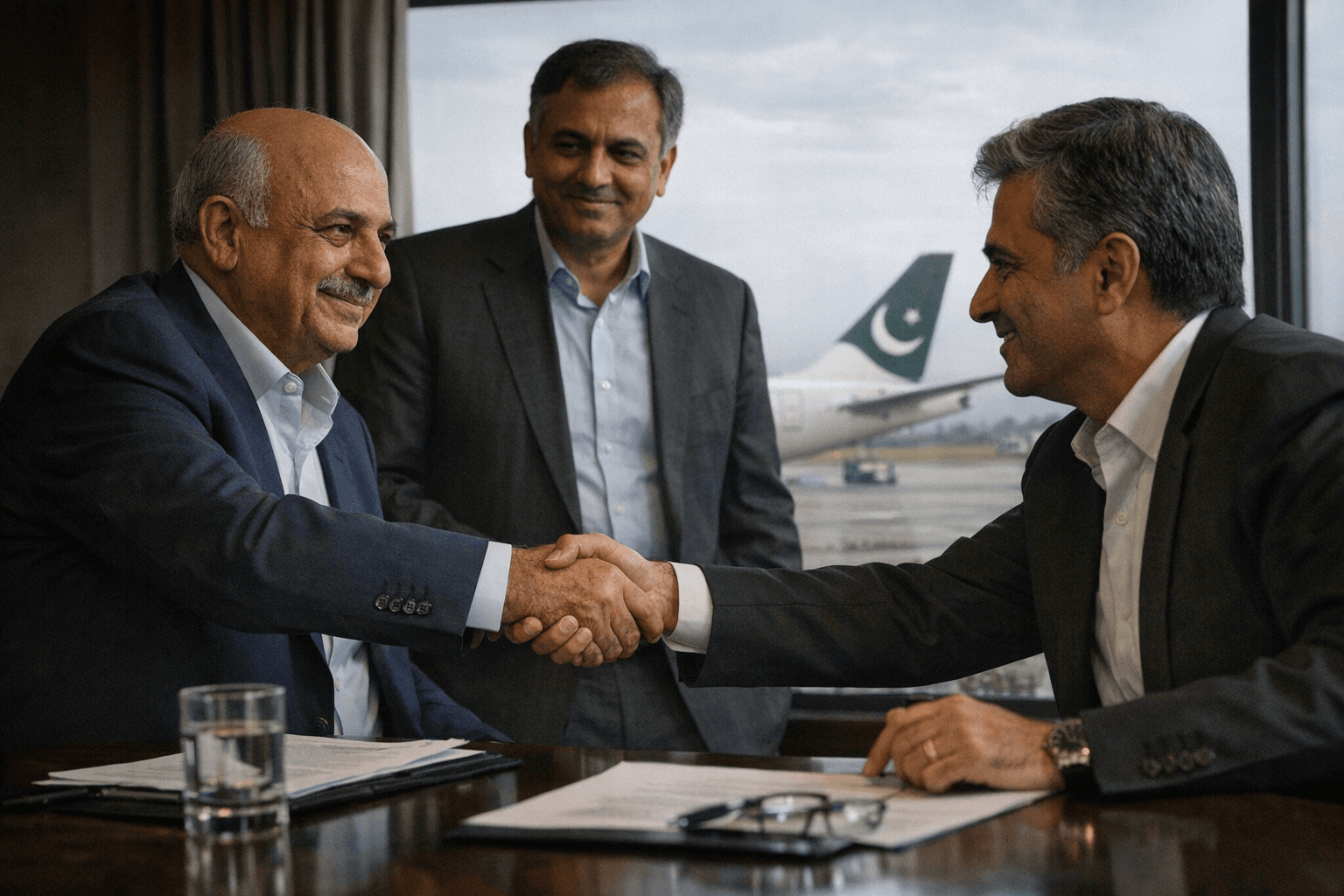

A consortium led by Pakistani financier Arif Habib emerged as the winning bidder on December 23, 2025 for a 75 percent stake in state owned Pakistan International Airlines, offering Rs135 billion for control of the national carrier. The accepted price converts to roughly US 482 million, and marks one of the largest privatisation moves in Pakistan in nearly two decades.

The Arif Habib group’s winning team reportedly includes Fatima Fertiliser Company, Lake City Holdings, AKD Group Holding, and City Schools among its partners, reflecting a consortium drawn from finance, industry, education and manufacturing. Two other groups made serious bids in a televised, multiple round auction stage. Budget carrier Airblue made an early offer of Rs26.5 billion and withdrew from later rounds. A rival led by Lucky Cement pushed competition to the wire, advancing from about Rs101.5 billion to a final Rs134 billion before the Arif Habib consortium increased its bid to the winning figure.

Officials said sources varied on the government reference price used to resume the sale, with figures cited between Rs100 billion and Rs125 billion, but the final accepted bid was consistent across accounts at Rs135 billion. Under the financial terms disclosed, the government will receive about Rs10.12 billion in cash immediately, while the remainder of the bid value will be injected back into PIA to support operations and restructuring.

The Privatisation Ministry described the outcome as the successful completion of a transparent and highly competitive bidding process and framed the sale as an important milestone in the wider privatisation programme. The transfer still requires regulatory clearances and formal closing mechanics, and the precise timetable for management handover was not immediately disclosed.

Market implications are significant. For the Treasury, even a partly cash financed sale provides near term fiscal relief and reduces direct exposure to PIA’s operating losses. For the airline industry, private control under a diversified corporate group could accelerate fleet renewal, network rationalisation and commercial discipline, potentially heightening competition on domestic and regional routes. Financial investors will watch whether the consortium assumes legacy liabilities such as outstanding debt and pension obligations or negotiates those with the state, a determinant of the deal’s ultimate value.

Policy wise, the transaction signals renewed government emphasis on selling non core assets to attract private capital, a longstanding IMF conditionality and domestic reform objective. The sale follows a failed privatisation attempt last year that drew insufficient bids, and comes after regulatory and operational changes that some industry observers say improved PIA’s viability, including relief on certain operational bans.

Longer term the deal underscores a trend of conglomerates and cross sector consortia taking stakes in strategic industries, leveraging diversified cash flows to underwrite complex turnarounds. The success or failure of the Arif Habib consortium in stabilising PIA will be a test case for Pakistan’s capacity to hand over legacy state enterprises to private ownership while protecting service continuity, labour rights and fiscal stability.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?