Bank of England warns rate hikes could shake gilt market

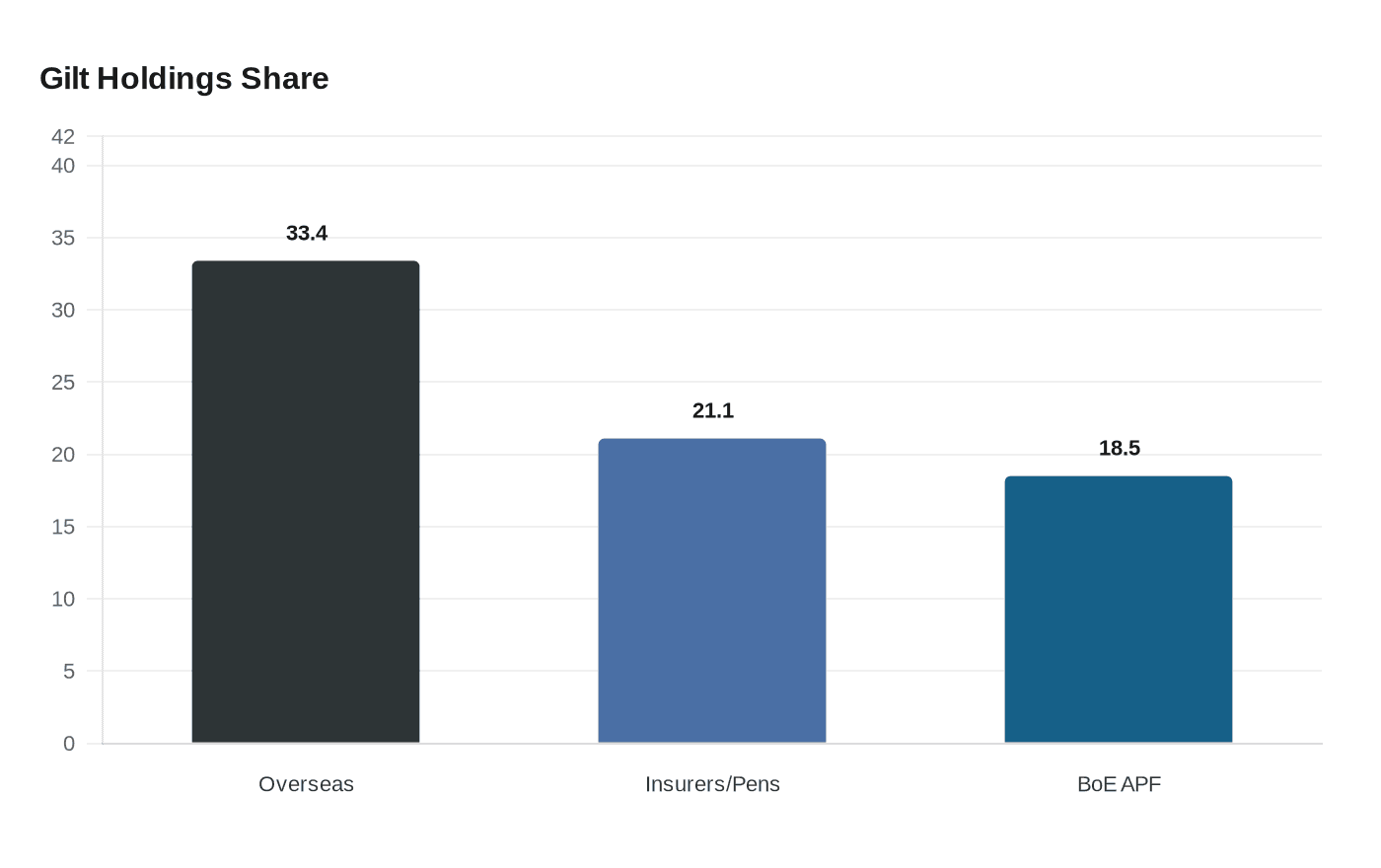

Catherine Mann warned that gilts are more fragile than they look, with overseas investors now holding 33.4% and past pension-fund fire sales showing how fast shocks can spread.

Catherine Mann warned that another round of Bank of England rate hikes could unsettle Britain’s gilt market, where the investor base has shifted sharply toward overseas buyers and other price-sensitive holders. That matters because gilts are the benchmark for mortgages, corporate borrowing and government financing, so any sudden jump in yields would ripple well beyond London’s trading desks.

The concern is not simply that higher interest rates would lift borrowing costs in the usual way. Mann’s point is that the market structure itself has become more fragile. The UK Debt Management Office said overseas investors held 33.4% of all gilts at the end of September 2025, making them the largest investor group. Insurance companies and pension funds held 21.1%, while the Bank of England’s Asset Purchase Facility still held 18.5%. With more debt in the hands of investors who can move quickly, a tightening cycle could trigger faster selling, sharper yield swings and a more abrupt repricing of government debt.

That risk is easier to understand in light of the September-October 2022 gilt crisis. The Bank of England said the market suffered extreme stress after liability-driven investment funds came under pressure, with deteriorating derivative and repo positions driving selling that drained liquidity. The Bank later launched a temporary backstop gilt purchase facility to prevent dysfunction in core funding markets. In a working paper, the Bank said forced sales by LDI funds created price discounts of about 10% and accounted for roughly half the total decline in gilt prices during the episode.

The lesson from that shock is that leverage can turn a policy move into a market event. The Bank’s 2025 discussion paper said repo markets are central to gilt-market resilience because they support short-term secured borrowing and leveraged strategies. That makes the plumbing of the market almost as important as the policy rate itself. If heavily leveraged investors are forced to unwind at the same time, even a justified rise in rates can amplify moves in prices and yields.

The current holdings data show how much the market has changed since the UK Debt Management Office took over gilt issuance from the Bank of England in April 1998. The DMO now publishes detailed information on gilt prices, yields, issuance, turnover and holdings, reflecting a market that is far larger and more globally owned than in earlier decades. Mann’s warning suggests that in such a market, the next inflation-fighting move from Threadneedle Street could arrive with more financial strain than policymakers may want.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)