Britain’s leadership turmoil sends gilt yields to multi-year highs

Britain's 10-year gilt yield hit its highest since July 2008 as leadership jitters revived memories of the Truss bond rout.

Britain’s bond market has become the sharpest judge of the latest leadership turmoil, pushing government borrowing costs to levels not seen in years and reminding ministers that fiscal credibility can disappear fast.

Ten-year gilt yields climbed to their highest level since July 2008, while 20-year and 30-year yields rose to their highest since 1998. The selloff was driven by a mix of domestic political worries, including the prospect of Greater Manchester mayor Andy Burnham challenging Prime Minister Keir Starmer, and a renewed global fear that inflation is proving harder to contain than investors had hoped.

For markets, the comparison that matters is 2022. The Liz Truss and Kwasi Kwarteng mini-budget triggered a violent gilt rout after unfunded tax cuts shook confidence in Britain’s fiscal discipline. That episode ended in a rapid political reversal, and it still shapes investor behavior today. Asset managers and major buyers of UK debt say they are watching closely to see whether any leadership challenge would open the door to looser fiscal policy, heavier borrowing and a fresh test of the state’s commitment to restraint.

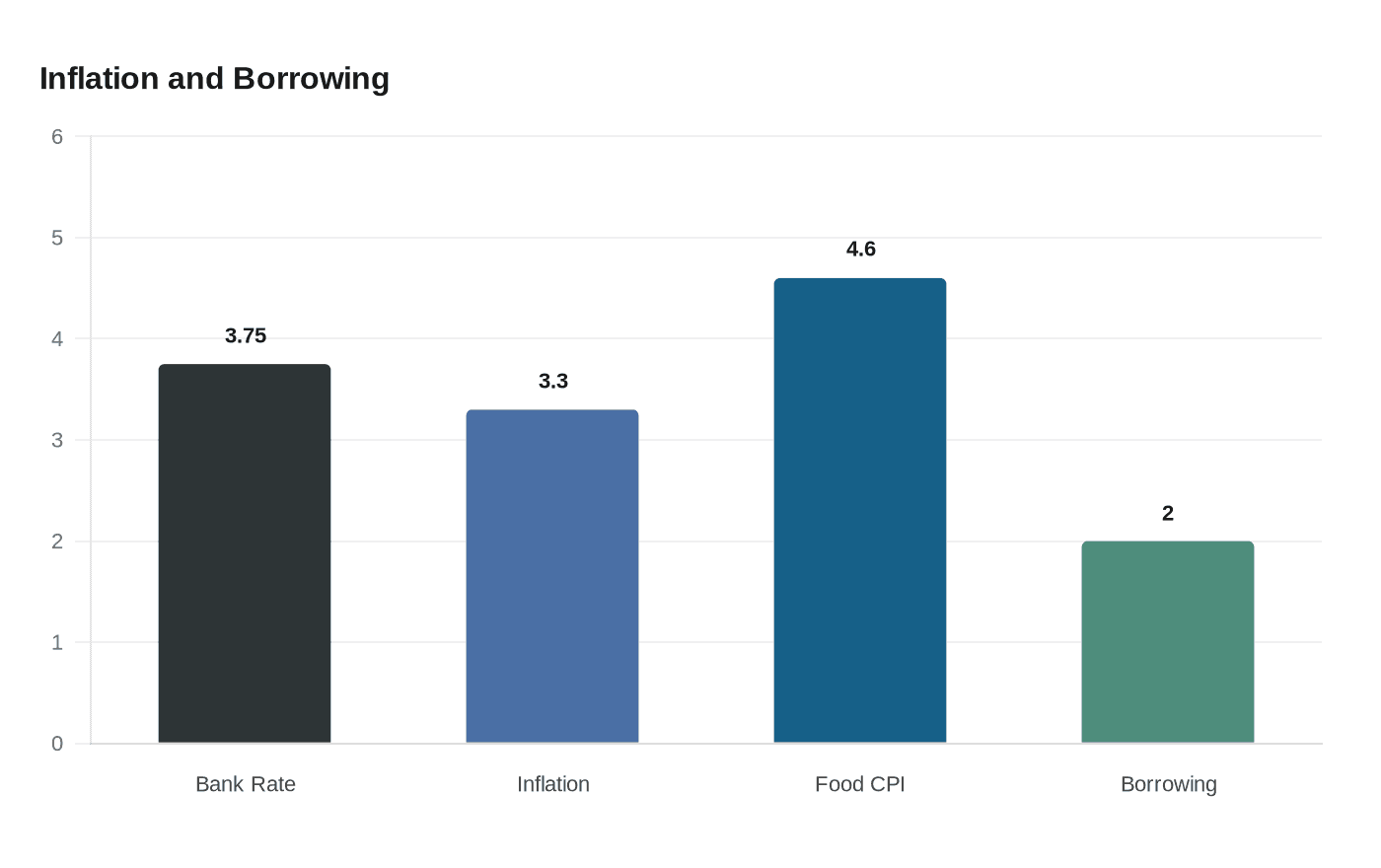

The pressure is landing at the same time as inflation is refusing to fade. The Bank of England held Bank Rate at 3.75% on April 30 and said inflation had risen to 3.3%. In its April Monetary Policy Report, the central bank warned inflation could rise further this year because of Middle East energy-price shocks. It also said consumer food price inflation was expected to reach 4.6% by September 2026 as higher energy costs feed through to imported and domestic production.

That backdrop matters because gilt yields are the benchmark for how much it costs the state to borrow, and they feed through into household borrowing costs as lenders reprice mortgages, corporate loans and other credit against higher government yields. The Office for Budget Responsibility’s March forecast said the plans set out at the November 2025 Budget were aimed at reducing borrowing to around 2% of GDP by 2030-31, a path consistent with debt stabilisation. Rising yields make that arithmetic harder.

The Bank of England publishes daily estimated gilt yield curves based on UK government bonds, and those curves now show a market demanding a larger premium to hold British debt. In practical terms, that means every leadership wobble carries a financial cost, and the bond market is making clear that Britain’s next prime minister will govern under tighter constraints than ever.

Know something we missed? Have a correction or additional information?

Submit a Tip