Brunello Cucinelli Sees 10% 2026 Growth After Strong 2025 Results

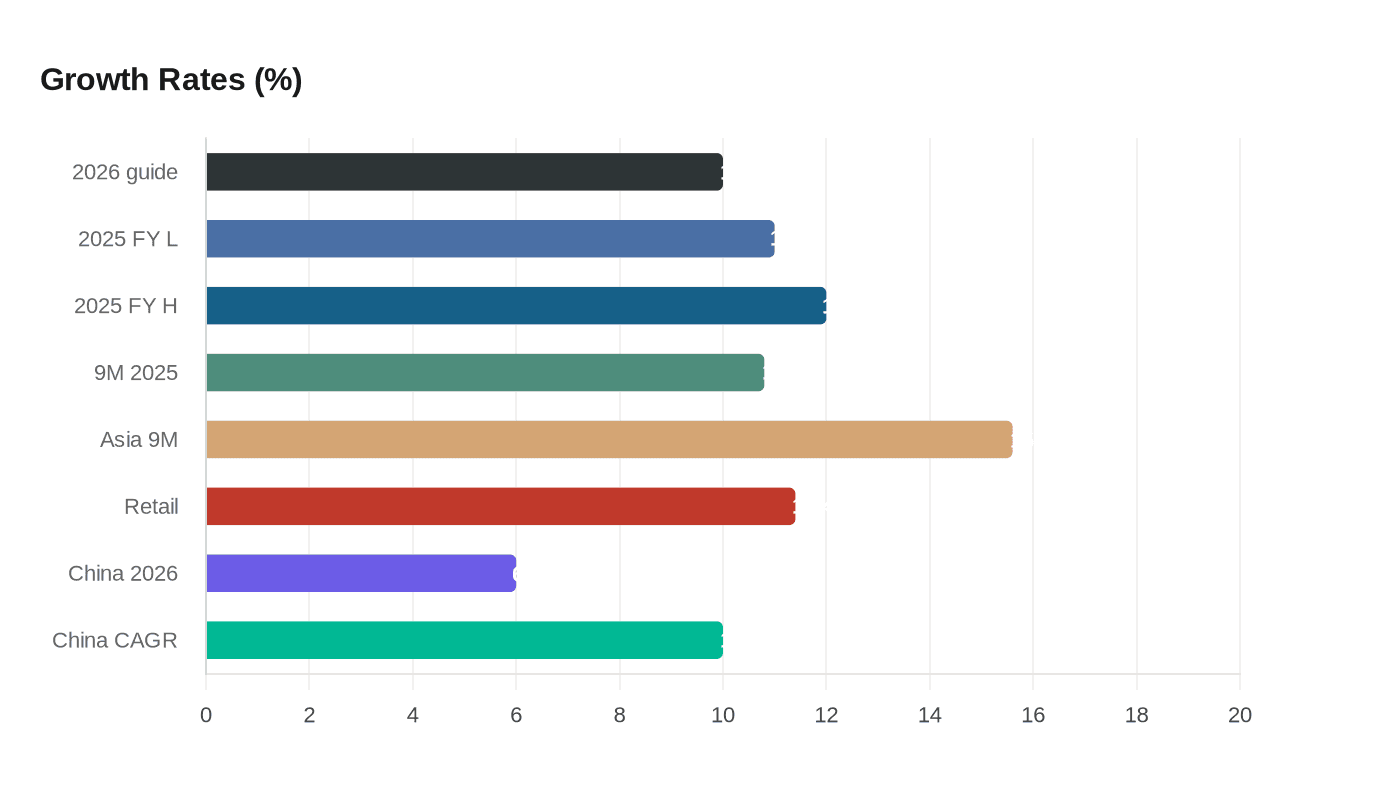

Brunello Cucinelli said strong early retail and healthy order books pushed 2025 revenue to about €1.4bn and management reiterated roughly 10% revenue growth for 2026.

Brunello Cucinelli has translated its craft-led, humanistic-capitalism stance into measurable momentum: management reported roughly €1.4 billion in full-year revenue for 2025 and reiterated an expectation of around 10 percent revenue growth for 2026, citing strong early-year retail and robust order books for fall and spring-summer collections. That trajectory underlines the brand's decision to favor curated assortments and like-for-like retail productivity over rapid store expansion.

Market-facing metrics back the claim. Preliminary reporting showed full-year 2025 revenues up roughly 11–12 percent at constant exchange rates, while nine-month sales had already surpassed €1.02 billion, up 10.8 percent, with Asia delivering particularly sharp gains. The nine-month Asian performance climbed about 15.6 percent, and company commentary highlighted retail channel growth of approximately 11.4 percent as a key driver of the year’s results.

Order intake and sell-through provide the operational case for the guidance. Management flagged a strong order intake for the Spring/Summer 2026 collection and a solid winter sell-out performance; as the company put it, “multi-brand clients worldwide have closed a strong winter season with us and opened the summer season with sell-out levels that are even better than last year.” CFO Luca Lisandroni underlined the retail rebound, saying, “Retail showed an excellent performance in the beginning of the year and wholesale has also been very positive, with growth across the board in markets and in both men’s and women’s categories.” He added that North America accelerated in the fourth quarter and is showing an “excellent” performance in 2026 so far.

The commercial posture remains deliberately calibrated. Freedom24 and company materials describe Brunello Cucinelli as an Italian luxury apparel brand and Casa di Moda that prioritizes Made in Italy craftsmanship; management has reiterated a disciplined growth strategy and a long-term ambition to reach roughly €1.8 billion in revenue by 2028. The investor presentation forecasted “healthy and balanced growth of around 10%, slight improvement in EBIT,” and signaled that growth will be concentrated in retail and distributed across regions to improve geographic balance.

The balance sheet and shareholder return plan reflect that discipline. Net debt for the core business stood at €198.4 million after significant investments and a distribution of €68.8 million in dividends; the board will propose a dividend of €1.04 per share, a payout of about 51 percent, at the Shareholders Meeting called for 23 April 2026.

Analysts and macro forecasters give the company room to execute. BNP Paribas projects China’s luxury market could grow about 6 percent in 2026 and a 10 percent CAGR through 2027–2031, supporting the brand’s Asia-first momentum. Market commentary placed Brunello Cucinelli’s share price near €82–€84 in January 2026, with a cluster of 12-month analyst targets in the low- to mid-€100s and a central tendency in the low-€110s.

One item in external briefings — an AI e-commerce project named Callimacus — has not appeared in the company’s investor presentation or press materials and remains unconfirmed. For now, the tangible story is clearer: tactile cashmere, measured merchandising and steady orders have driven a record sales base of about €1.4 billion and positioned Brunello Cucinelli to pursue roughly 10 percent growth in 2026 while protecting the brand’s craftsmanship-led wardrobe proposition.

Know something we missed? Have a correction or additional information?

Submit a Tip