Can debt collectors freeze joint bank accounts? Here's what to know

A creditor usually needs a court judgment to reach a bank account, but a joint account can still be exposed even if only one owner owes the debt.

A joint account can turn one person’s debt into everyone’s problem

A debt collector generally cannot just reach into a bank account and pull out money. In most cases, the collector must sue, win a judgment, and then get a court order before it can garnish or levy funds. That basic rule matters most when the account is joint, because the law often treats each owner as having equal rights to the money, even if only one person incurred the debt.

That is why spouses, parents, roommates, and other co-owners can get caught in the middle. A joint account may be vulnerable to collection activity tied to someone else’s debt, and the result can be a freeze, a levy, or a bank hold that leaves both owners scrambling to cover rent, groceries, or bills.

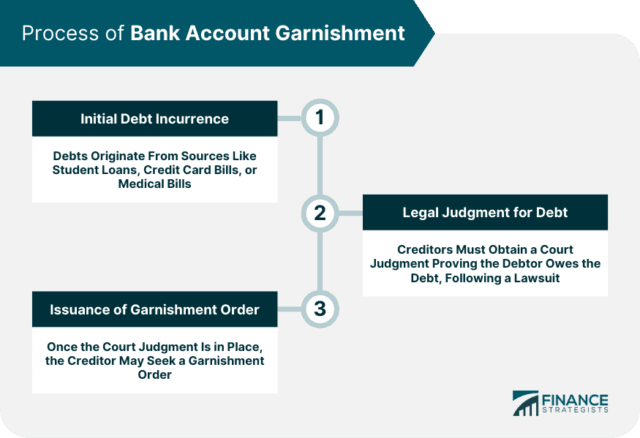

When a creditor can freeze money

The first threshold is a legal one: a creditor or collector usually has to sue and win before it can garnish wages or tap a bank account. The Federal Trade Commission says a collector can get a court order to take money from a bank account, and the Consumer Financial Protection Bureau says garnishments generally flow from a judgment. There is an important exception for some government debts, which can be collected differently.

That means a freeze is usually not the opening move in ordinary private debt collection. It is more often the result of a lawsuit that has already moved through court. Once that happens, a bank may be ordered to turn over money from an account, and the customer may not learn about the order until funds are already restricted.

Why joint accounts are especially exposed

Joint ownership complicates everything. The law usually presumes each owner has equal access to the full balance, not just a split share on paper. Because of that presumption, creditors may be able to levy a jointly owned savings or checking account even if one account holder does not owe the debt.

That is the part many people miss. A joint account does not always function like two separate personal balances inside one wrapper. In collection cases, the account can look like a single pool of money that is vulnerable to seizure, even when one owner is completely innocent of the underlying debt. Nolo notes that a creditor might be able to garnish a joint account in exactly that situation.

At the same time, joint checking accounts usually give both owners broad control. In most circumstances, either person on the account can withdraw money and close it, depending on the account agreement and state law. That creates a practical tension: the account may be easy for either owner to use day to day, but also easier for a creditor to target if one owner has a judgment against them.

Which money has the strongest protections

Not all money in an account is treated the same way. Federal and state law can protect some wages, benefits, or bank-account funds through exemptions or limits, so a debtor is left with enough to live on. The strongest protections often apply to federal benefits, including Social Security and Veterans Affairs payments.

Those benefits have special rules when they are directly deposited. The CFPB says banks must protect two months’ worth of Social Security or VA benefits that arrive by direct deposit. That protection can make a major difference in a frozen account, especially for households that rely on benefit income to cover basic expenses.

The delivery method matters. The CFPB says the key to protecting federal benefits is direct deposit into a bank account or prepaid card. If benefit money is coming in another way, it may not receive the same automatic safeguard. For households living on fixed income, that detail can determine whether protected money is identifiable or swept into a broader collection action.

What state law and the account agreement can change

Federal rules set the baseline, but state law can change the outcome in meaningful ways. The CFPB says state laws may provide additional protections against unfair or deceptive collection practices, and they may also affect how bank-account funds are handled once a collector seeks a levy.

The account agreement matters too. It can affect who can withdraw money, who can close the account, and how the bank responds when a court order arrives. That is why two people can have the same bank account type and still face different outcomes depending on where they live and how the account was set up.

In practice, that means joint-account risk is not uniform across the country. A creditor’s ability to freeze funds can depend on the judgment itself, the type of debt, the bank’s procedures, the account contract, and the state’s exemption rules. The legal label may be the same everywhere, but the result can look very different from one jurisdiction to another.

What to do immediately if the account is locked

If a joint account suddenly stops working, move quickly and focus on the paperwork behind the freeze. The first step is to ask the bank what court order it received and whether the hold is tied to a judgment, a levy, or a garnishment. That tells you whether the collector had to go through court and whether any funds may be exempt.

Then check whether protected money is in the account. If Social Security or VA benefits were directly deposited, tell the bank immediately that those funds may be covered by federal protections. Because the CFPB says banks must protect two months’ worth of those direct-deposited benefits, that information can be crucial in getting the right amount released.

It also helps to gather account statements that show where the money came from and to review the account agreement and state law. If the account is joint, the innocent co-owner should not assume the freeze is final or that all money is automatically available for collection. In many cases, the legal fight turns on whether the funds are exempt and how the bank was instructed to treat them.

- Ask the bank for the exact legal basis of the freeze.

- Identify any direct-deposited Social Security or VA payments.

- Save statements that show the source of funds.

- Review the account agreement and the governing state rules.

- Get legal help quickly if protected benefits or a joint account are involved.

The bottom line

A joint bank account can expose one person’s money to another person’s debt, and that risk becomes real once a creditor has a judgment and a court order. Federal benefits, state exemptions, and account-specific rules can limit what gets taken, but the safest assumption is simple: if your name is on the account, someone else’s debt dispute can land on your doorstep fast.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?