Can Debt Collectors Pursue Borrowers From Two Directions at Once

Debt collectors can legally hit wages and bank accounts at the same time, but only after clearing a specific legal gauntlet — knowing each step gives borrowers real room to fight back.

The Two-Front Reality

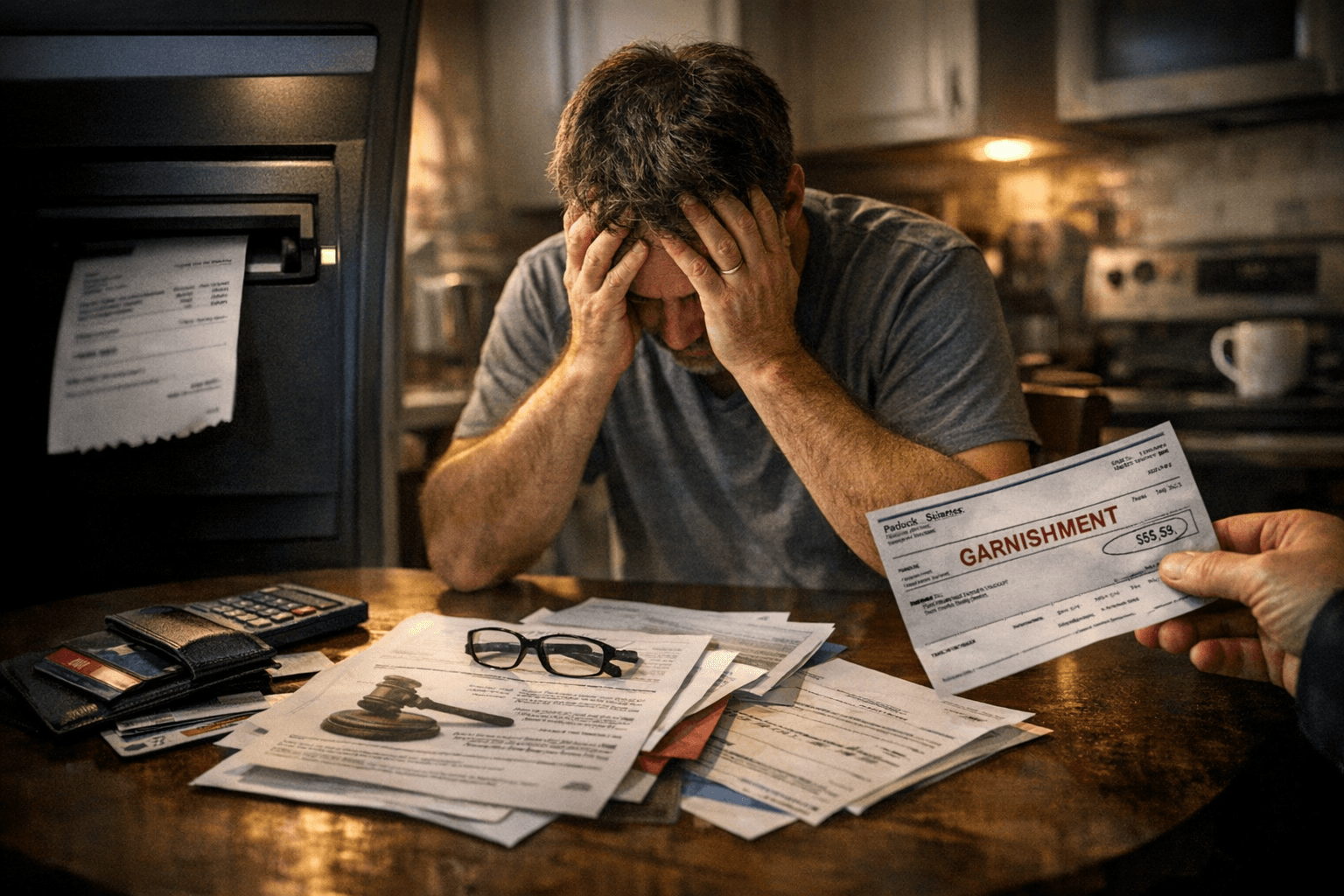

Most people assume a debt collector comes at you one way at a time. The reality is more aggressive. Once a creditor clears the legal prerequisites, nothing in federal law prevents it from simultaneously directing a writ to your employer to garnish wages and a separate writ to your bank to freeze whatever cash sits in your account. A creditor who obtains a judgment can then take steps to collect such as garnishment of wages or bank accounts, or seizure of property. The two instruments work independently, which means a single unpaid debt can drain your paycheck on Friday and lock your checking account on Monday.

The critical word, though, is "judgment." That requirement is not a formality — it is the entire legal gateway, and understanding each step between an unpaid bill and a frozen bank balance is where you find room to act.

The Legal Gauntlet: Judgment, Writ, and Notice

No private debt collector can touch your wages or your bank account without first winning in court. A collector must first sue you to get a court order — called a garnishment — that says it can take money from your paycheck to pay your debts. A collector can also get a court order to take money from your bank account. This means a lawsuit, a served summons, and a hearing you have the right to attend and contest.

After the court enters a judgment, the creditor applies for a writ of garnishment specific to each target: one directed at your employer, another at your financial institution. These are separate instruments and separate processes. Wage garnishment typically requires prior notification to the debtor, allowing time to contest the action. In contrast, bank account garnishment can occur with minimal notice, often freezing funds immediately upon the bank's receipt of the levy. That asymmetry is the practical core of the two-front threat: the paycheck attack telegraphs itself; the bank account freeze often does not.

Wage Garnishment: The Federal Floor and What States Add

At the federal level, wage garnishment is governed primarily by the Consumer Credit Protection Act (CCPA). The CCPA limits the amount a creditor can withhold from your wages in a single pay period. Under federal law, the garnished amount can't exceed the lesser of 25% of your disposable earnings or the amount by which your weekly income exceeds 30 times the federal minimum wage. Disposable earnings are your income after legally required deductions, such as federal taxes, Social Security, and Medicare. Voluntary paycheck deductions — a 401(k) contribution or a health insurance premium — do not reduce the disposable earnings calculation, which catches many workers off guard. A maximum of 25 percent can be garnished if disposable income earnings are $290.00 or more per week.

Child support and alimony operate under different, stricter rules: the garnishment law allows up to 50 percent of a worker's disposable earnings to be garnished for these purposes if the worker is supporting another spouse or child.

Federal law also provides one additional layer of job protection: federal law prohibits employers from firing employees for wage garnishment for one debt. However, if you have garnishments for two or more separate debts, that protection no longer applies.

State-by-State Guardrails

Four states go substantially further than the federal baseline. Wage garnishment by private debt collectors is fully prohibited in Texas, Pennsylvania, North Carolina, and South Carolina, giving residents of those states a significant layer of legal protection that most Americans don't have. In these states, debt collectors who hold civil court judgments cannot reach your paycheck, a protection that holds regardless of how much you owe or how long the debt has gone unpaid.

Living in one of those four states does not mean you are untouchable, however. Creditors can still pursue other collection avenues, including levying bank accounts. Texas makes this explicit: once wages are deposited into a bank account, the funds can be frozen. The protection covers the paycheck itself, not the moment those dollars arrive in your account.

Several other states cap garnishment below the federal 25% ceiling. Illinois limits garnishment to 15% of gross earnings (versus the federal 25% of disposable), while West Virginia and Wisconsin each cap it at 20%. Oregon's protections are set to rise further: starting July 1, 2027, the protected amount will be based on Oregon's state minimum wage, meaning that as the minimum wage increases, so does the share of a paycheck that is shielded.

A 2023 study of payroll data conducted by professors from Northwestern and MIT found that roughly 1 in 100 workers are subject to wage garnishment and lose an average of 10% of their gross earnings to creditors, with garnishments lasting from several months to years.

Bank Account Levies: The Faster-Moving Threat

The bank levy is structurally different from wage garnishment in one critical way: a bank levy is a one-time action, but the creditor can keep returning to repeat the process. There is no ongoing withholding order sitting at the bank; the creditor must actively re-levy to capture new deposits. That does not make it less dangerous — a freeze on an account can strand rent payments, utility drafts, and grocery money before you receive any notice.

Whether your funds are shielded from a levy depends largely on where the money came from in the first place. Federal law builds in automatic protections for certain sources. Under the Treasury Department's garnishment rules, financial institutions are required to automatically protect a certain amount of federally exempt funds deposited within the preceding two months, even before account holders have to take any action.

The most significant of those automatic protections covers Social Security. Section 207 of the Social Security Act states that Social Security benefits are exempt from garnishment, levy, attachment, or other legal processes by most creditors. The CCPA also provides strong protections for Social Security benefits after they hit your bank account, meaning private creditors such as credit card companies, personal lenders, or medical debt collectors typically cannot take these benefits to satisfy a debt. Two months of Social Security funds that are directly deposited into your account usually get automatic special protection from garnishment by judgment creditors. VA benefits carry equivalent protections under federal law.

The phrase "directly deposited" matters enormously. The key to making sure your federal benefits are legally protected from being frozen or garnished is to use direct deposit to put the money into your account or prepaid card. If you receive a paper check and deposit it manually, you may have to fight in court for protection that direct deposit recipients receive automatically.

Contesting Improper Garnishment

When a levy hits funds you believe are protected, the clock starts immediately. In California, you have only 10 days from the date of the levy to file a claim of exemption — plus 5 days if the notice was sent by mail — with the sheriff, and you must show that the funds taken came from a source of income that is exempt from collection.

To formally contest a bank levy, you will generally need two documents: a Certification in Objection to Levy — a detailed statement explaining why the levied funds are exempt — and a Certification of Service, which is proof that you have provided copies of your documents to the relevant parties. The Consumer Financial Protection Bureau advises that you should notify the court, the bank, and the person or business garnishing your account immediately in writing, and seek help from a lawyer, noting that you may qualify for free legal help.

For wage garnishment, the process runs through the same court that issued the original judgment. To have a garnishment reduced or dismissed, you must demonstrate that the withheld amount violates federal or state exemption thresholds, or that the underlying funds — if the wages were deposited before the writ was served — qualify for a protected category.

Prioritizing Your Response: Stop the Fastest Threat First

Because a bank levy can freeze your account the same day the bank receives the writ, it represents the more urgent tactical problem. Wage garnishment, with its notification requirements, typically gives you slightly more lead time to act. That said, both threats dissolve if the underlying judgment never happens — which makes contesting the lawsuit itself, before a default judgment is entered, the highest-leverage point in the entire process.

If negotiating with a creditor before judgment, focus on a lump-sum settlement or a formal payment agreement, both of which creditors are often willing to accept for less than the full balance rather than incurring the cost and delay of litigation. Once a judgment is entered, the negotiating dynamic shifts: the creditor holds legal enforcement tools and has less incentive to discount the debt. No state permanently suspends wage garnishment for consumer credit card debt; your wages can get garnished once a creditor wins a court judgment against you. Temporary suspensions happen only during bankruptcy, when an automatic stay pauses all collections.

A bankruptcy filing does impose an immediate automatic stay on all collection activity, including active garnishments and pending levies. For borrowers already facing simultaneous wage and bank garnishment, it can be the only instrument that stops both fronts at once — though it carries its own long-term credit consequences that must be weighed carefully against the immediate financial relief it provides.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?