Cardinal Health raises profit forecast on strong specialty drug demand

Cardinal Health lifted its profit forecast as specialty drug demand surged more than 20%, showing how costly medicines keep rewarding distributors.

Cardinal Health’s latest quarter showed how much profit in drug distribution now depends on expensive medicines. Sales came in below Wall Street’s target, but stronger demand for specialty drugs and branded treatments pushed earnings higher and led the company to raise its full-year forecast.

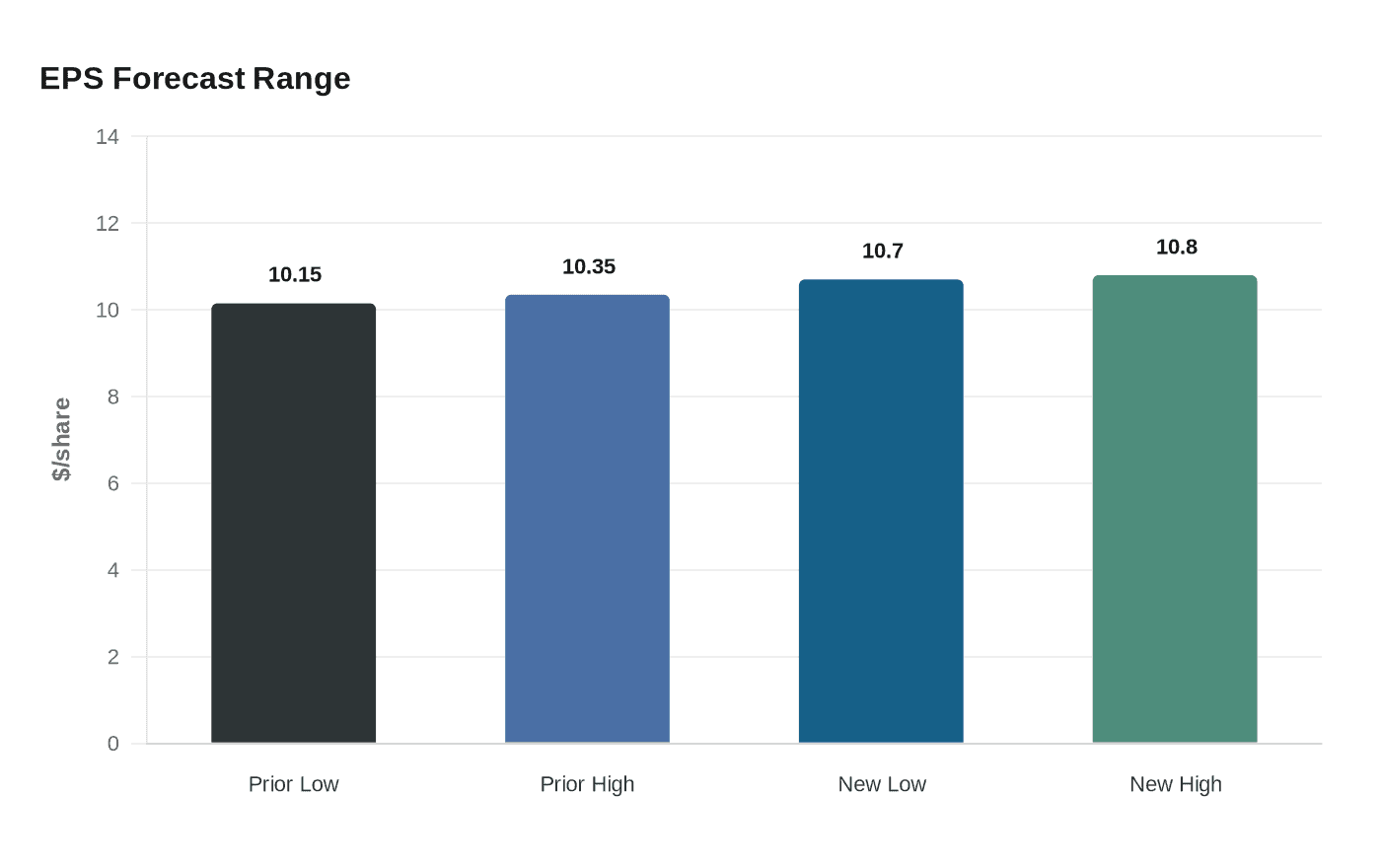

The Dublin, Ohio-based company lifted its fiscal 2026 adjusted profit outlook to $10.70 to $10.80 per share, from a prior range of $10.15 to $10.35. That topped analysts’ expectation of $10.31, and the stock rose 1.6% in premarket trading. For the quarter, Cardinal reported non-GAAP diluted earnings of $3.17 a share, well ahead of the $2.79 estimate, even as revenue of $60.9 billion fell short of the $61.7 billion forecast.

The results underscore a shift that is reshaping the economics of the health-care supply chain. Cardinal’s Pharmaceutical and Specialty Solutions segment generated $56.1 billion in quarterly sales, up 11% from a year earlier, while Specialty revenue grew more than 20% in the third quarter. The company said Specialty revenue is still expected to exceed $50 billion in fiscal 2026, a threshold that highlights how much of the business is being driven by high-cost therapies used for cancer, autoimmune disease and other complex conditions.

That mix matters. Specialty drugs tend to carry higher margins than commodity medicines, giving distributors such as Cardinal, Cencora and McKesson a clearer route to profit even when broad prescription volumes are uneven. The same trend also helps biosimilars, which are taking a larger share of the market as older blockbuster drugs lose patent protection. For patients, employers and insurers, however, the rise of costly specialty treatments means the system’s spending burden keeps climbing even when distributors are not selling more units overall.

Cardinal’s earnings details showed that contrast clearly. Revenue in the quarter rose 11% from a year earlier to $60.9 billion, GAAP diluted earnings fell 20% to $1.69, and non-GAAP operating earnings increased 18% to $956 million. The company also completed an additional $250 million share repurchase, bringing fiscal 2026 buybacks to $1.0 billion, and continued reducing debt.

Beyond distribution, Cardinal is moving deeper into specialty care. It bought Specialty Networks for $1.2 billion in 2024 and announced the $1.9 billion purchase of Solaris Health in 2025, moves that widen its access to physician practices and specialty-care networks. The strategy suggests the company sees the specialty-drug boom not as a one-quarter boost, but as a durable engine for earnings in a system where expensive medicine is becoming the defining profit pool.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)