Carlyle Private Credit Fund Gates Redemptions After Requests Triple Quarterly Limit

Carlyle's CTAC private credit fund received redemption requests tripling its 5% quarterly cap, the sharpest stress test yet for the semi-liquid structures sold to retail and institutional investors.

Carlyle's Tactical Private Credit Fund received withdrawal requests covering 15.7% of its outstanding shares for the first quarter of 2026, more than three times the 5% quarterly repurchase limit built into its structure, forcing the firm to cap redemptions and leaving the majority of exiting investors locked in until at least the next repurchase window.

The Carlyle Tactical Private Credit Fund, known as CTAC, received repurchase requests amounting to roughly 15.7% of shares outstanding, according to a shareholder letter. Carlyle's flagship private-credit interval fund is the latest to be hit with a wave of share-redemption requests. The fund, which carried net assets of approximately $4.6 billion as of January 2026, invests across loans, direct lending, and structured credit, products marketed to retail and institutional investors as a way to capture private-market yields while retaining at least quarterly liquidity options.

Those liquidity options have a hard ceiling. Interval fund structures allow managers to set quarterly repurchase limits, and when requests exceed them, the gate closes. Honoring CTAC's full 15.7% request would have required Carlyle to liquidate a significant portion of its holdings or tap external credit lines in a market where illiquid loan portfolios are already under pressure from shifting rate and credit conditions. Instead, the firm restricted repurchases to the contractual 5% limit, meaning investors who sought an exit will receive, at most, roughly one-third of what they requested this quarter.

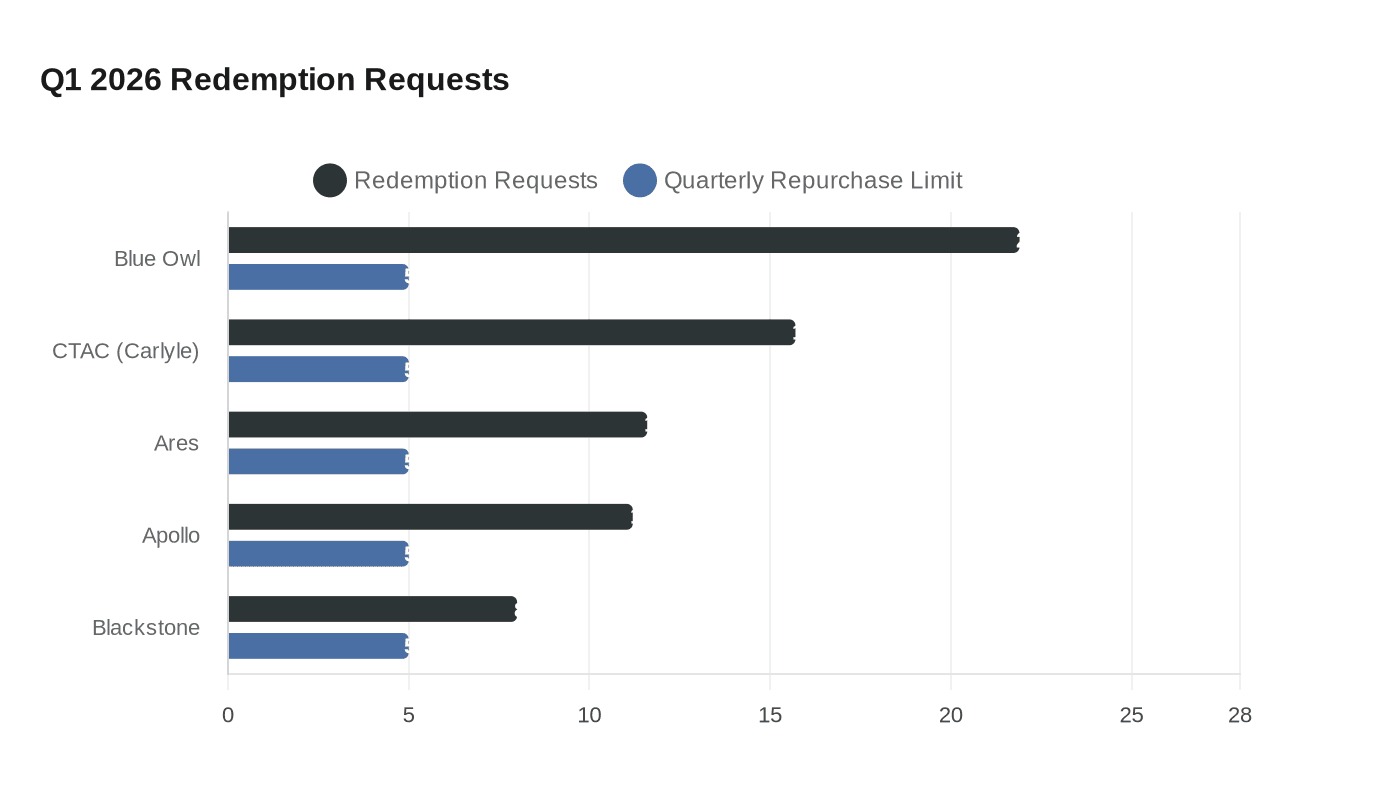

The episode fits a pattern that has spread across the private credit industry since January. In the first quarter of 2026, redemption requests hit 8% at Blackstone's private credit fund, 11.2% at Apollo, 11.6% at Ares, and 21.9% at Blue Owl. Both Apollo and Ares fulfilled roughly 43% to 45% of their respective requested redemptions, sticking to their 5% limits, while emphasizing their focus on large-cap borrowers with EBITDA exceeding $250 million. Blue Owl moved further: as news of Blue Owl's decision to halt quarterly redemptions in favor of capital distributions spread, Blue Owl, Blackstone, BlackRock, Ares Management and other publicly traded managers of private credit BDCs saw their shares slide substantially.

The structural mechanics behind these gates are not new, but the simultaneity of their activation across multiple major funds is. In November 2022, Blackstone's non-traded real estate trust BREIT triggered this gate for the first time, marking the first systemic liquidity event in a perpetual semi-liquid structure. That episode unfolded in a single asset class and a single fund; the current pressure spans direct lending, structured credit, and several managers simultaneously, raising the systemic stakes considerably.

The central tension in these products has always been the gap between portfolio liquidity and investor expectations. Private credit loans are, by nature, illiquid: they cannot be sold in minutes on an exchange the way a Treasury or a public corporate bond can. Quarterly redemption windows create the appearance of access without the underlying market depth to support it at scale. When a large enough share of investors decides to leave at the same moment, whether because of rate anxiety, portfolio rebalancing, or broader macro unease, the mismatch becomes visible. Gates protect remaining investors from forced sales at distressed prices, but they simultaneously confirm the illiquidity that spooked investors in the first place, a feedback loop that managers now have to navigate carefully.

The private credit industry has grown to a staggering $3.5 trillion in assets under management, after a decade of explosive growth, and the first quarter of 2026 has signaled a painful transition as retail investors, who drove much of that expansion, pull back in record numbers. Regulators and wealth advisers are watching the space for signs that investor protections designed for institutional capital are insufficient for the retail channels through which much of this recent growth flowed. Whether CTAC's gate becomes a one-quarter correction or the opening move in a prolonged liquidity reckoning depends largely on whether the withdrawal pressure subsides before the next repurchase window opens in the second quarter.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?