Centene lifts profit forecast after beating estimates on cost control progress

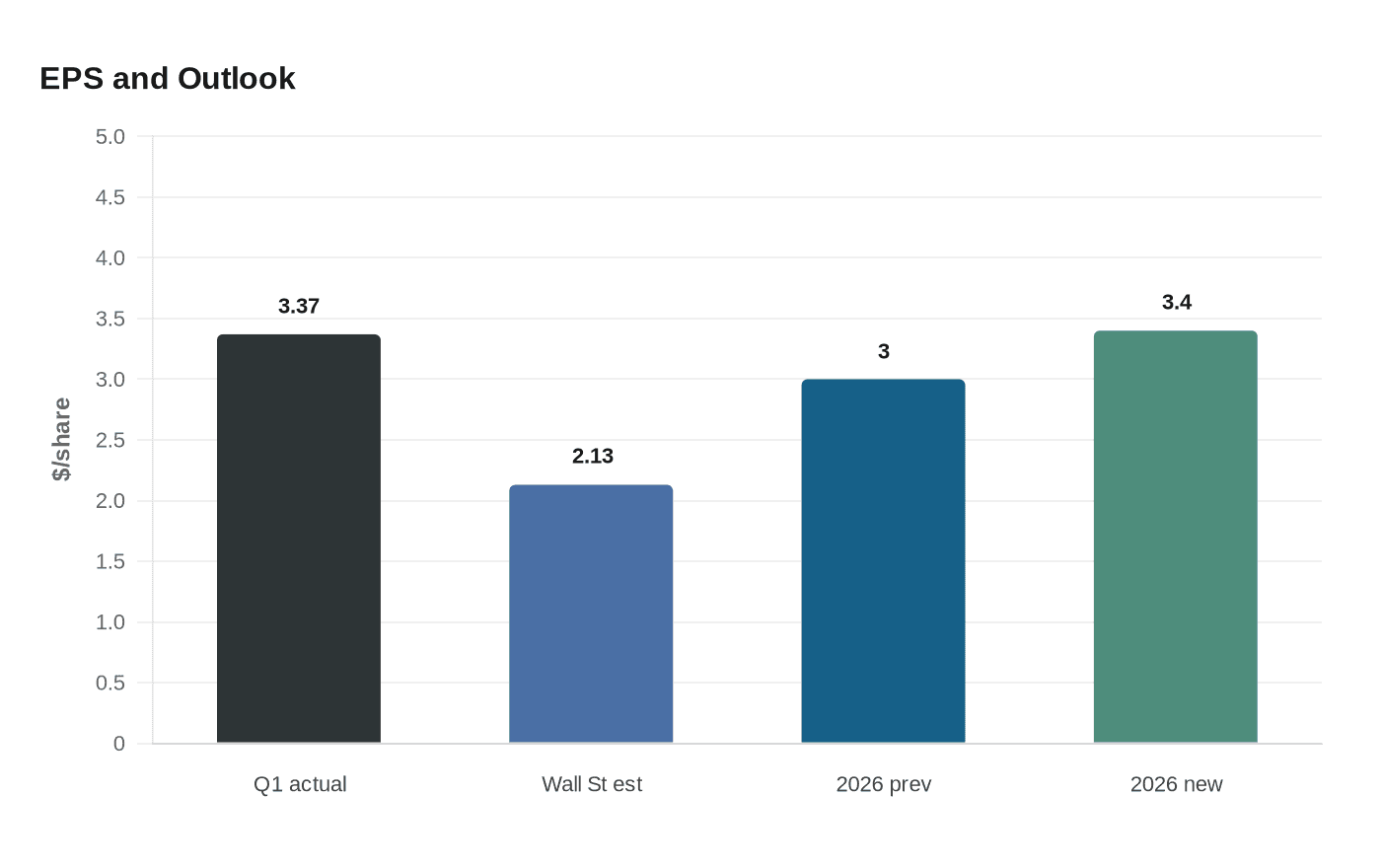

Centene raised its 2026 profit outlook to above $3.40 a share after a first-quarter beat, helped by an 87.3% medical-cost ratio that came in better than expected.

Centene lifted its 2026 profit forecast on Tuesday after topping quarterly expectations, a sign that one of the country’s biggest Medicaid and Affordable Care Act insurers is making progress in controlling medical costs that have squeezed the sector for more than two years.

The St. Louis-based company now sees adjusted diluted earnings above $3.40 a share, up from a prior outlook of more than $3.00. In the first quarter, Centene earned $3.37 a share on an adjusted basis, far ahead of Wall Street’s $2.13 estimate. Revenue reached $49.944 billion, while premium and service revenue totaled $44.655 billion. Shares rose in premarket trading after the announcement.

Chief Executive Officer Sarah London said the company was making “tangible progress in our margin recovery efforts,” and that is the key question for investors, patients and taxpayers alike: what does cost control actually mean inside a managed-care giant? In Centene’s case, it appears to be a mix of tighter operations, better management of medical spending and a more favorable balance between premiums collected and care delivered.

The company said its first-quarter health benefits ratio, a closely watched measure of how much premium revenue goes to medical care, was 87.3%, better than the 89.42% analysts had expected. Centene’s Medicaid health benefits ratio was 93.1%, its Medicare segment ratio was 84.9% and its Commercial ratio was 75.3%. Centene said the commercial result reflected higher acuity among Marketplace Silver Tier members before an anticipated 2026 net risk adjustment benefit.

The quarter also showed more financial discipline on the balance sheet. Centene said it generated $4.366 billion in cash flow from operations and reduced debt by $1.0 billion. Adjusted SG&A expense ratio was 7.6%, underscoring the company’s effort to rein in overhead even as it works through volatile medical trends.

The broader backdrop remains difficult. Insurers are still dealing with elevated care costs, shifting reimbursement rates and the effects of Trump-era tax and budget policy that will reduce Medicaid funding for low-income Americans. Expiring pandemic-era subsidies have also left a sicker pool of Affordable Care Act members, pressuring margins across the marketplace business.

Centene’s own numbers suggest that the turnaround is real, but not simple. Some of the improvement may reflect better care management and moderate flu activity. Some may reflect pricing changes and member mix. The company’s results, and the higher outlook that followed, point to a managed-care rebound that extends beyond Centene, with UnitedHealth and Elevance also raising guidance.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?