Seagate forecasts upbeat revenue, profit as AI storage demand surges

Seagate’s upbeat forecast showed AI is lifting storage makers, not just chip stocks, as enterprises build out the data pipes behind large models.

Seagate Technology used its latest forecast to make a simple case: the AI boom is creating a second wave of winners beyond semiconductors, and hard drives are one of them.

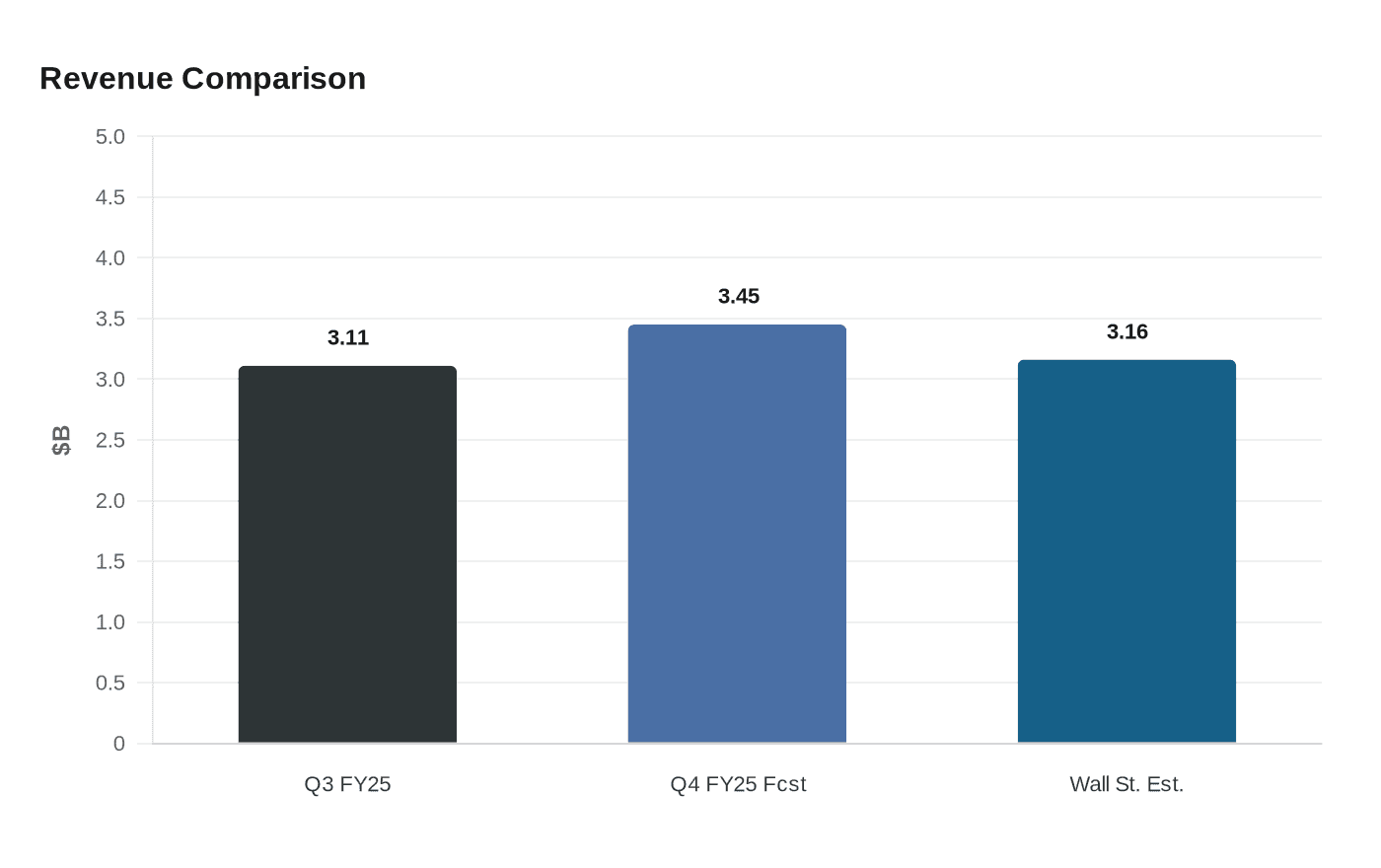

The company projected fiscal fourth-quarter revenue of $3.45 billion, plus or minus $100 million, well above Wall Street’s $3.16 billion estimate, and adjusted earnings of $5 a share, plus or minus 20 cents, versus expectations of $3.97. Shares jumped about 10% in extended trading, a sign that investors are still rewarding the infrastructure suppliers feeding artificial intelligence.

Seagate’s pitch rests on demand that is broader than model training alone. The company said businesses are using AI to speed up processes and cut costs, but are also pouring money into storage to manage the huge volumes of data needed to create and run large models. That demand is showing up in cloud contracts, enterprise systems and sovereign-cloud builds, where data-sovereignty rules are pushing more storage onshore.

The company’s fiscal third quarter, ended April 3, underscored the scale of the opportunity. Seagate reported revenue of $3.11 billion and GAAP diluted earnings per share of $3.27, both ahead of expectations. It generated $1.1 billion in cash from operations and $953 million in free cash flow, retired about $641 million in debt and returned $191 million to shareholders through dividends and buybacks. Seagate ended the quarter with $1.1 billion in cash and cash equivalents.

Chief executive Dave Mosley said Seagate believes it is entering “a new era of structural growth” as AI applications amplify data creation and sustain storage demand. That message is now backed by a more aggressive financial framework. At its May 22, 2025 investor day, the company set targets through fiscal 2028 for low-to-mid teens revenue growth, about 40% non-GAAP gross margin and a $5 billion share-repurchase authorization.

Seagate has also been leaning into capacity gains. On July 15, 2025, it launched up to 30TB Exos M and IronWolf Pro drives and said more than one million Mozaic hard drives had already shipped. The company’s areal-density strategy is aimed at higher-capacity storage that uses less energy and capital per terabyte, a pitch that matters as hyperscalers and enterprise data centers keep building out AI infrastructure. Seagate cited IDC’s Ed Burns as saying those customers were in the early stages of an “all-out arms race” to build that infrastructure.

The market backdrop is also helping. Memory-chip prices jumped 80% to 90% sequentially in the first quarter, tightening supply and improving pricing power for vendors that can secure inventory. Western Digital has offered a similar read on the industry, with CEO Irving Tan saying in March that AI demand is pushing the company toward higher-capacity drives rather than simply more drives.

For Seagate, the question is no longer whether AI spending is real. It is whether the current rush becomes a durable infrastructure build-out or a cycle that cools if capital spending slows. For now, the storage side of AI is looking less like a sideshow than a core trade.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?