Central banks buy more gold, raising questions about secure storage

Central banks are piling into gold, but the bigger question is where to keep it when crisis hits, and why that location can matter as much as the metal itself.

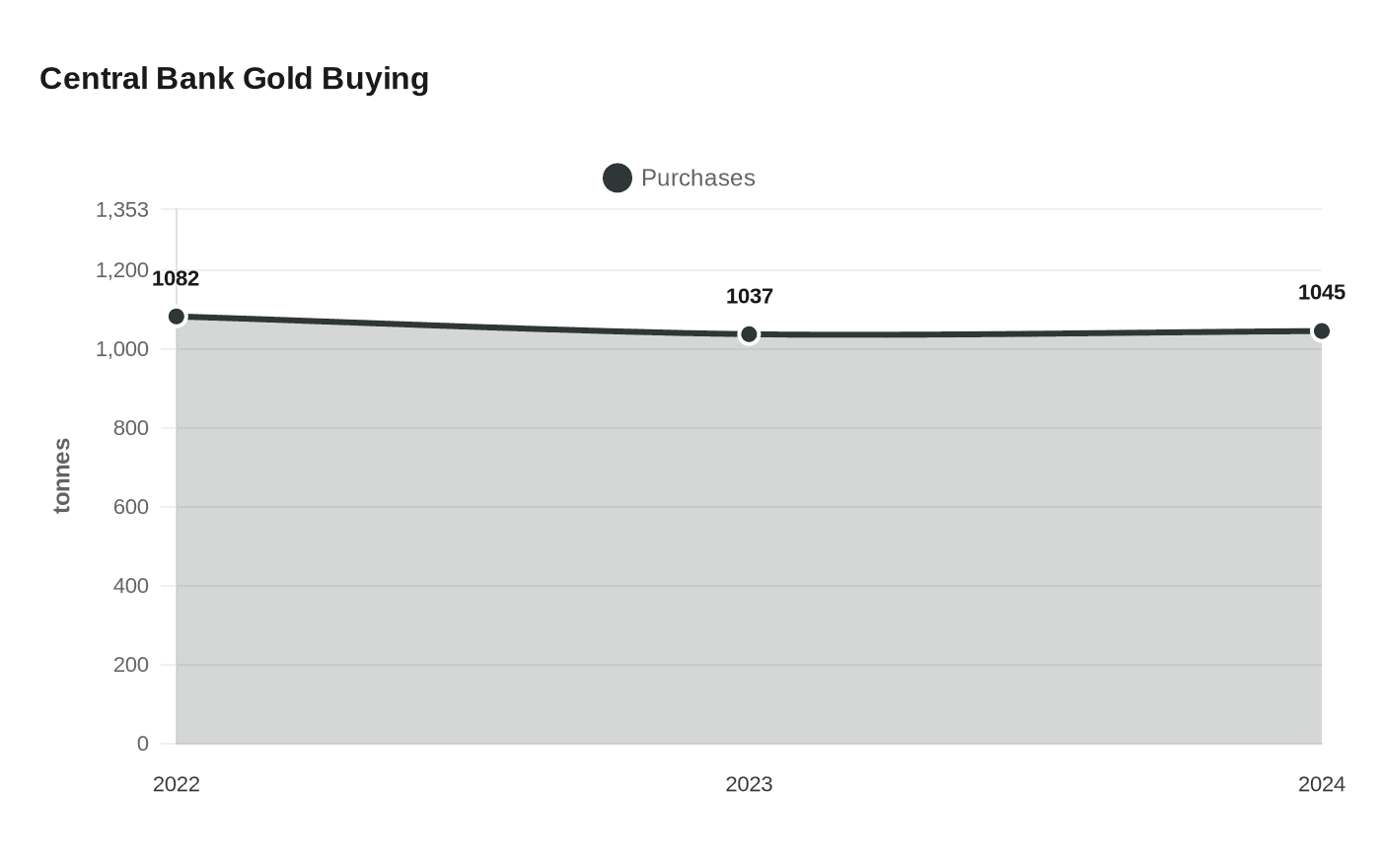

Gold is back at the center of reserve strategy

Central banks are buying gold at a pace that has turned storage from a back-office detail into a strategic question. They added 1,037 tonnes in 2023, the second-highest annual purchase on record after 1,082 tonnes in 2022, and the World Gold Council says the buying continued with another 1,045 tonnes in 2024. That scale matters because gold is not just a line item on a balance sheet. It is a liquid reserve asset that central banks want secure, accessible and, if needed, ready to move when markets are under stress.

The case for gold has strengthened alongside the broader reserve-management backdrop. Inflation has been a persistent concern, geopolitical instability has raised the premium on assets outside any one country’s control, and trade conflicts or tariffs can complicate how reserve managers think about liquidity and access. Gold sits at the intersection of all three risks: it is tangible, globally recognized and widely accepted in emergency conditions.

What central banks say they want from gold

The World Gold Council’s 2025 Central Bank Gold Reserves survey shows that demand is not only about owning more gold, but about what gold represents in a shaky world. The survey drew 73 responses, the highest participation since the survey began eight years earlier, and 76% of respondents said gold will make up a higher share of total reserves five years from now.

That optimism is grounded in how reserve managers view gold’s role. In the same survey, 85% of respondents said gold’s performance during times of crisis is highly or somewhat relevant, 81% cited its diversification role, and 80% cited its function as a store of value. The methodology note says the fieldwork ran from 25 February to 20 May 2025 and represented a 49% response rate among contacted central banks. Those figures suggest that gold is not being treated as a relic of an earlier monetary era, but as a tool for managing modern uncertainty.

Where the gold actually sits

The physical location of reserve gold matters because security is only one part of the equation. It also has to be tradable, auditable and quickly mobilized if conditions deteriorate. That is why so much sovereign gold remains concentrated in major financial centers, especially New York and Frankfurt am Main.

The Federal Reserve Bank of New York says its gold vault is on the basement floor of its main office building in Manhattan, a structure built in the early 1920s. The New York Fed says it acts only as custodian, holding gold for account holders that include the U.S. government, foreign governments, other central banks and international organizations. It also says it is the only Federal Reserve Bank that stores gold. That arrangement reflects more than convenience. It shows how trust in a custodial center can become part of the architecture of global finance.

The concentration also reflects liquidity. Gold stored in a trusted financial hub can be easier to pledge, swap or transfer in a crisis than gold kept in a remote location with slower logistics or weaker institutional guarantees. In practice, reserve managers are balancing the symbolic comfort of domestic storage against the market value of proximity to the world’s deepest financial plumbing.

Germany’s decision to bring gold home

Germany offers one of the clearest examples of how politics and reserve management intersect. The Deutsche Bundesbank said the transfer of significant gold holdings from New York and Paris to Frankfurt drew public attention, which is not surprising given how closely Germans have watched the location of their reserves. In 2017, the Bundesbank said it had completed the transfer three years ahead of schedule and that more than half of Germany’s gold reserves were then located in Germany.

That shift was not just logistical. It was a statement about control, transparency and national confidence. By bringing more gold home, Germany reduced reliance on foreign vaults for a larger share of its reserves while still maintaining access to internationally recognized storage points. The Bundesbank’s 2024 annual accounts put gold and gold receivables at €270,580 million at year-end 2024, a reminder that these holdings are not only politically sensitive but also enormous in financial terms.

The scale helps explain why the issue persists. When reserve assets run into the hundreds of billions of euros, storage is no longer a simple matter of safekeeping. It becomes a policy choice about how much risk to centralize abroad and how much to keep under domestic control.

Why location is a question of trust, liquidity and risk

The more gold central banks buy, the more important it becomes to decide where that gold should live. Domestic storage offers political reassurance and direct control. Foreign storage in centers such as New York can offer deep custodial expertise, established settlement links and easier access to international markets. Each option carries trade-offs, and the best answer depends on what a central bank is trying to protect against.

If the main concern is physical security, the long-established vaults of major financial centers have strong credentials. If the concern is geopolitical risk, holding too much abroad can look like a vulnerability. If the concern is crisis response, then the ability to move gold quickly, or use it in swaps and other reserve operations, can matter as much as the location itself. That is why the policy question is not simply how much gold central banks should own, but how much should be held domestically versus abroad, and how quickly it can be mobilized if markets seize up.

The recent buying wave has made that question harder to ignore. With 2023 and 2024 both showing exceptional central-bank demand, and with the latest survey indicating that most respondents expect gold to claim a larger share of reserves five years from now, the hidden infrastructure behind reserve management is getting more scrutiny. In a world shaped by inflation risk, geopolitical tension and trade friction, the vault is no longer just where gold sleeps. It is part of the strategy.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?