China Signals IP-Driven Consumption Support, Lifts Pop Mart and Toy Stocks

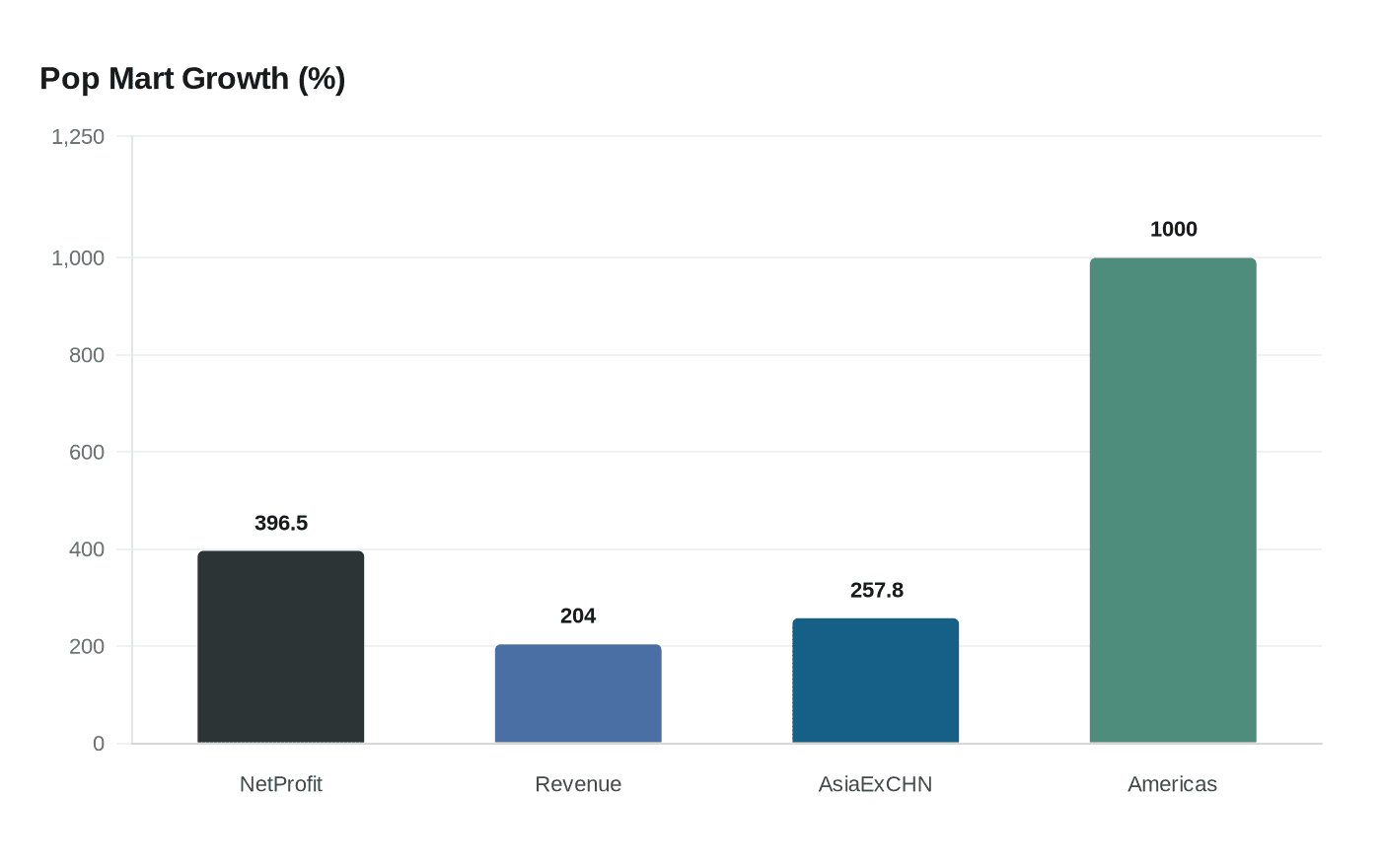

China’s NDRC flagged support for IP-driven consumption, sending Pop Mart up as much as 5.2% as the toymaker reported H1 net profit up 396.5%.

China’s push to develop IP-related consumption in its 2026 policy priorities gave a clear tailwind to Hong Kong-listed toy and IP retailers, with Pop Mart among the biggest beneficiaries. The National Development and Reform Commission signaled it would encourage collaborations between high-quality consumer resources and well-known intellectual properties, and GuruFocus reported Pop Mart International Group rose as much as 5.2% in Hong Kong after the policy signal. Miniso Group climbed up to 2.3% and Bloks Group advanced up to 3.8% on the same reaction, and a market line printed 0325.HK +1.31%.

That policy lift arrived while Pop Mart was flaunting blockbuster results. The company reported that net profit for the first six months of 2025 surged about 396.5% and revenue rose roughly 204% year-on-year. Overseas sales were a standout: Asia-Pacific excluding China rose 257.8% to 2.85 billion yuan and the Americas jumped more than 1,000% to 2.26 billion yuan, figures highlighted in CNBC’s coverage of the earnings. Those numbers helped drive a volatile trading day tied to the release, when shares initially fell nearly 5% in early trade before reversing to close up 12.5%.

Pop Mart’s corporate actions added another story thread. South China Morning Post reported the company repurchased 1.4 million shares for a total of HK$251 million, buying at prices between HK$177.70 and HK$181.20 in what was described as its first buyback in two years. Shares opened at HK$198.70 and closed 9.1% higher at HK$197.20 on the day the repurchase was disclosed, and UOB Kay Hian private wealth management chief investment officer Wang Qi said, “Pop Mart’s share buy-back signals management’s confidence and a healthy balance sheet.” SCMP also cited a cash balance above 13 billion yuan.

Analysts are split between bullish momentum and structural caution. Hao Hong, managing partner and CIO at Lotus Asset Management, said, “The stock will likely make new highs in the coming weeks.” William Ma at Grow Investment Group flagged short-covering, domestic hedge fund profit-taking and global institutional interest as drivers of choppiness. Morningstar equity analyst Jeff Zhang warned on IP durability: “We think the longevity of popularity for Pop Mart’s key IPs remain uncertain. … there is no guarantee that consumers will continue to favor them in the next 5-10 years, as their preferences may change very fast.” GuruFocus also flagged one Warning Sign for PMRTY.

Brand traction and cultural cachet remain part of the story. Pop Mart’s Labubu IP is central to the business, the company said in its earnings statement, and Labubu has surfaced in exhibitions such as “the monsters Convenience Store” in Shanghai on July 23, 2025 and on celebrities from Blackpink’s Lisa to Rihanna and Kim Kardashian. Simply Wall St notes the NDRC signal ties directly into Pop Mart’s model of turning characters into licensed products and experiences, while cautioning that stronger policy support could invite more competition for prized IPs and retail locations.

The upshot: Pop Mart sits at the intersection of a national policy nudge, blockbuster H1 results and a visible buyback, but valuation questions and the long-term popularity of Labubu-style IPs will determine whether the recent gains translate into sustainable share-price performance.

Know something we missed? Have a correction or additional information?

Submit a Tip