Companies Rush to Close Deals Despite Market Volatility and Rising Oil Prices

Antitrust approvals under Trump fueled a $2.3 trillion U.S. M&A surge in 2025, and dealmakers are pressing forward in 2026 despite oil shocks and stock gyrations.

The logic defies instinct: as oil prices swing sharply and equity markets lurch, corporate boardrooms are accelerating, not delaying, their merger timelines. The calculus is rooted less in macroeconomic confidence than in a narrowing regulatory window that dealmakers believe may not stay open forever.

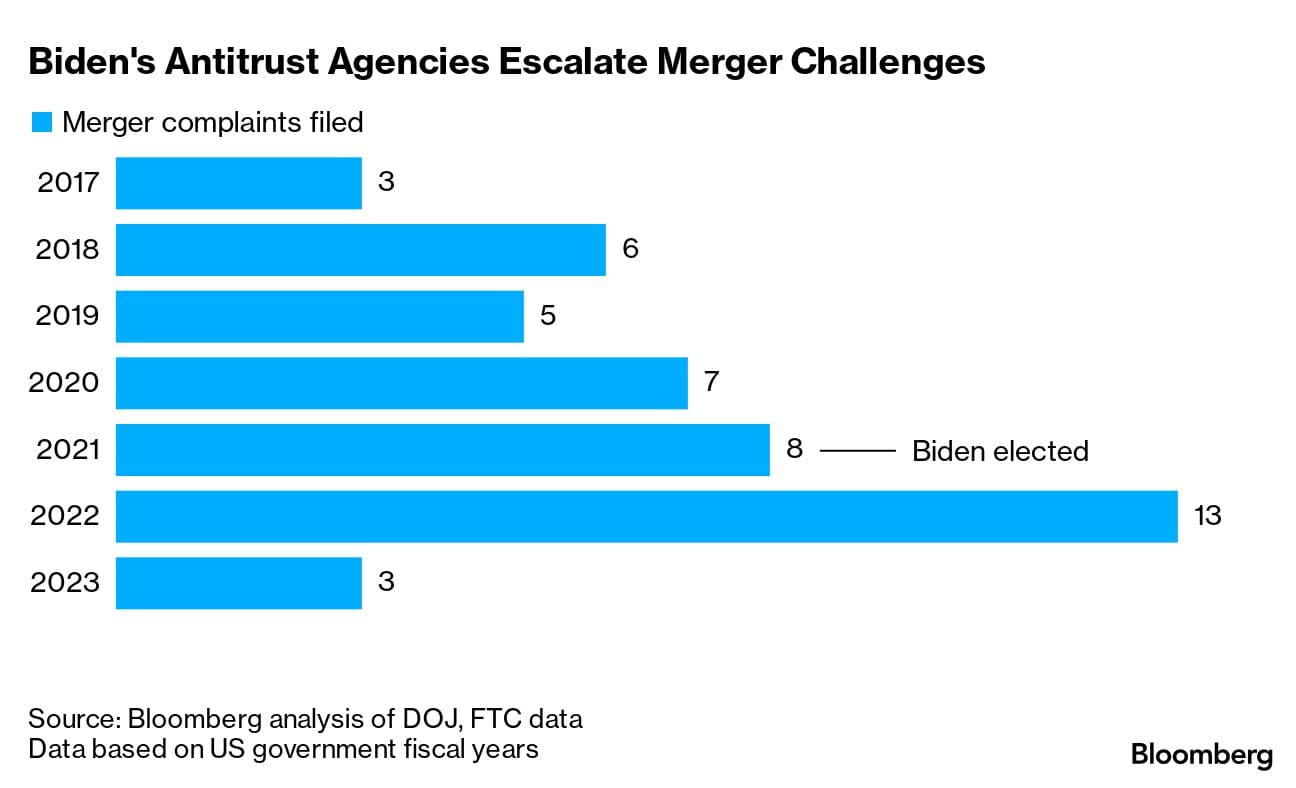

U.S. M&A deal volume in 2025 reached approximately $2.3 trillion, up 49% from 2024, a surge driven in large part by a shift in how federal antitrust agencies treated proposed combinations. Through Q3 2025, M&A volume for large-cap players increased a sizeable 36.8% year-over-year, following a 9.7% increase from 2023 to 2024, which was itself the first positive activity since 2021. Bankers say companies are braving higher oil prices and whipsawing stock prices to seize on the willingness of federal antitrust enforcers to approve mergers.

The behavioral shift at the Department of Justice and the Federal Trade Commission under the Trump administration has been the decisive variable. The agencies' stated openness to structural remedies is real, and transacting parties are now evaluating potential divestitures early in their deal planning process and considering whether remedies may offer a viable path to obtaining antitrust clearance. That stands in marked contrast to the Biden era, when agencies regularly used procedural delays to exhaust merger parties rather than negotiate workable fixes.

The results have been concrete. Notable deals that cleared DOJ antitrust scrutiny included UnitedHealth Group's acquisition of home care provider Amedisys for $3.3 billion and Nippon Steel North America's acquisition of United States Steel Corporation for $14.9 billion. The FTC required Boeing to divest several Spirit AeroSystems assets to proceed with its merger, and separately required the divestiture of oil change shops in the Valvoline-Greenbriar deal, both in the final months of 2025, signaling that conditions rather than outright blocks are now the agency's preferred instrument.

Technology and energy are carrying the heaviest deal traffic. Technology, media and telecom accounted for approximately 30% of global deal volume, and artificial intelligence has become the single largest animating rationale for consolidation. AI dominated Q1 2026 M&A activity, with 22 deals over $10 billion and a $110 billion funding round for OpenAI, with equity stake sales in the AI sector accounting for 29% of all merger and acquisition activity.

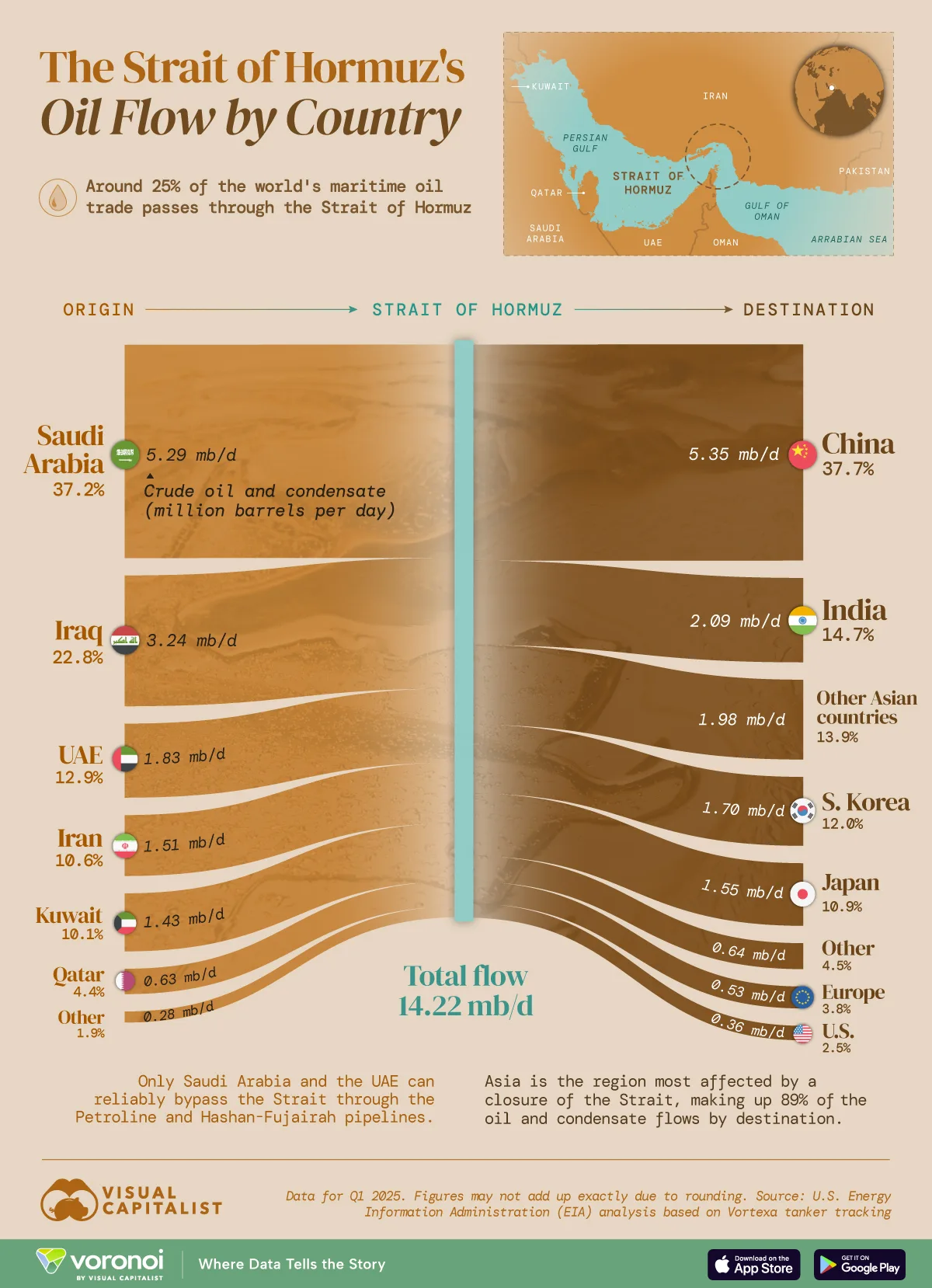

Energy deals carry a different kind of pressure. A combination of macroeconomic uncertainty, geopolitical shifts and volatile oil prices had an impact on M&A activity in the oil and gas industry through 2025, with new or increased tariffs on U.S. imports of steel and aluminum raising operational and capital costs for many companies operating in the sector. Heightened Middle East tensions slowed tanker traffic through the Strait of Hormuz and pushed energy price volatility higher, complicating deal valuations even as executives pressed ahead. In chemicals, OMV and ADNOC combined their assets to create BGI, one of the largest players in the industry, while companies such as LyondellBasell and Dow freed up cash to offset lower margins by pruning their portfolios through divestitures.

The willingness to transact in volatile conditions reflects a calculation that the current antitrust posture is time-limited. By the end of 2025, dealmakers were declaring that they could either cut a deal with the agency or pursue a White House strategy to obtain antitrust approval, feeding what observers described as transformational M&A fever. Legal analysts at Freshfields warned, however, that this perception could change dramatically as blue-state antitrust regulators expand their own review processes and as midterm election politics begin to reshape the enforcement landscape.

Regulatory considerations remain central to deal planning, with antitrust scrutiny, foreign investment regimes and export controls expected to remain key factors influencing both transaction structure and execution timelines. Companies are also focused on supply chain realignment and resilience as tariff uncertainty adds a new layer of complexity to cross-border combinations. For now, the race to close is on, driven by a judgment that the gap between deal ambition and regulatory reality has rarely been this narrow.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip