Daily Money Managers Help Seniors, Busy Professionals Navigate Personal Finances

A little-known profession handles the bills, insurance claims, and financial paperwork that overwhelm seniors and time-strapped professionals, and demand is quietly growing.

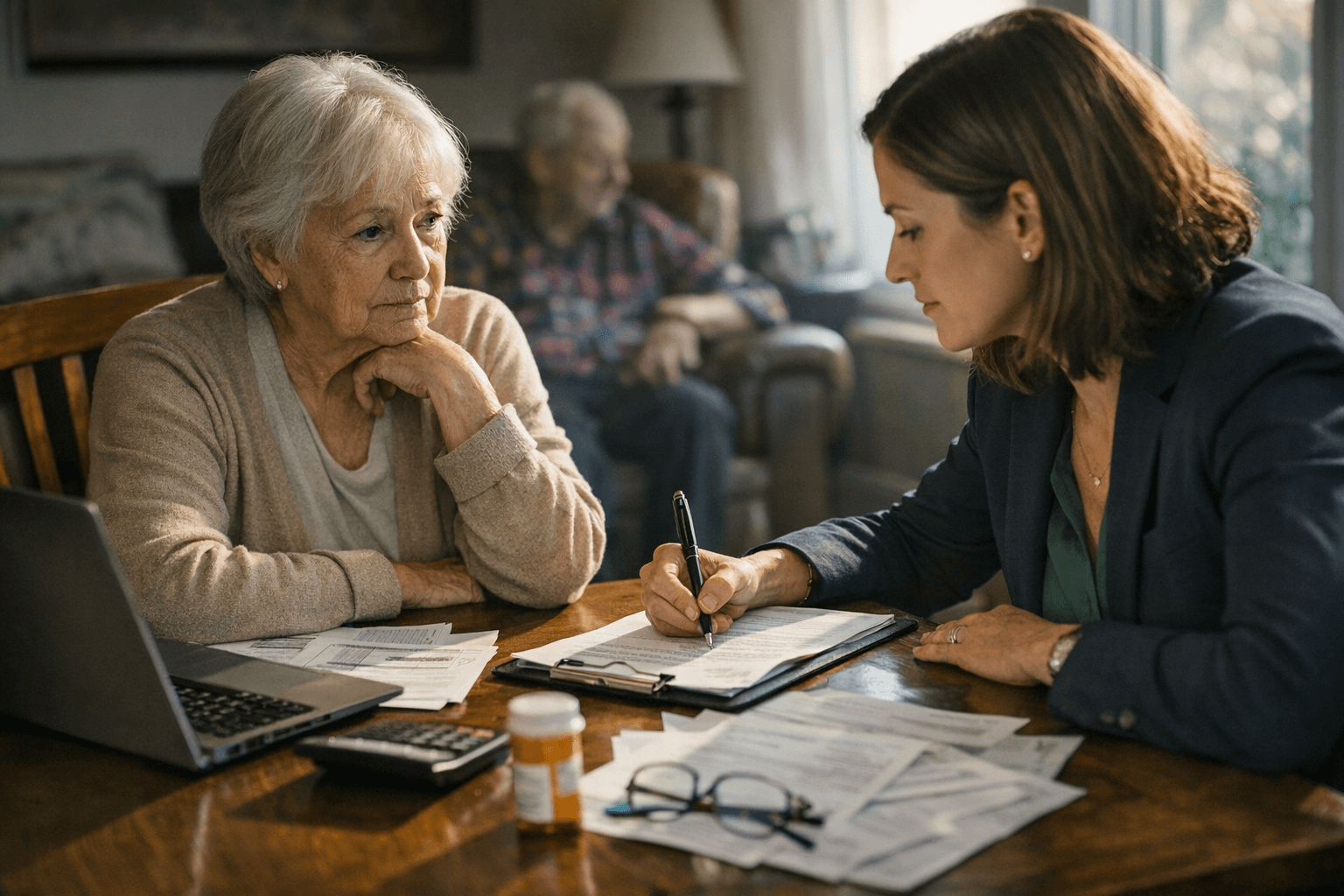

Clifton Herndon was 90 years old, living in Palo Alto, Calif., and facing a financial life that had suddenly become unmanageable. After her husband died of Alzheimer's disease, she hired a daily money manager named Salisbury in 2010. She called it a game changer.

Herndon's experience cuts to the heart of what this profession actually delivers: not investment advice or legal guidance, but the unglamorous, essential work of keeping a personal financial life running. Daily money managers deliver essential personal financial services to seniors and older adults, people with disabilities, busy professionals, high net worth individuals, small businesses, and others. Yet despite filling a genuine need, the profession remains largely unknown to most Americans who could benefit from it.

What a Daily Money Manager Actually Does

At its most fundamental level, daily money managers represent individuals and businesses in the field of daily money management, delivering essential personal financial services across a wide range of client types. Think of the financial tasks that pile up when life gets complicated: insurance reimbursements that never arrived, tax documents scattered across folders, bills that slipped through the cracks during a health crisis or a cross-country move.

Daily money managers specialize in helping people manage their day-to-day personal finances, including paying bills, tracking insurance claims, organizing files, safeguarding important financial documents, and budgeting. The AARP offers a vivid illustration of the work: imagine having someone who makes sure your bills are paid on time, organizes your tax documents and hands them off to your accountant, and follows up with your insurance company because you were supposed to be reimbursed for physical therapy.

DMM services provide value in monitoring medical bills and ensuring that Medicare and other health insurance have paid their share before the client pays any balance due. Additionally, DMM assistance in assembling papers needed for income tax preparation and in documenting medical and charitable contributions often means the client will pay lower taxes each year.

Paul Orsinger, a DMM with over 23 years of experience, frames the work in terms of what clients are really missing: "It's about bringing clarity. Where the money's coming from, where it's going. Some people live in a vagueness around their money, and that's one of the major benefits we bring to them."

It is worth understanding what DMMs are not. They are not financial or legal professionals, so they cannot act in an advisory capacity or prepare tax returns; but a good DMM can provide referrals to professionals like accountants, investment advisors, and lawyers. Since daily money managers often work with elderly persons living in their homes, they can also provide recommendations to other senior-serving professionals. If they see that a client is in any way "at risk" due to impaired vision, physical limitations, or confusion, they can make referrals to community resources, including care managers, attorneys, and accountants.

Who Hires a Daily Money Manager

Daily money managers generally help older adults and the wealthy, but busy professionals are increasingly turning to their services when they fall behind. As AARP has noted, you do not have to be wealthy to hire a trusted professional to take care of these kitchen-table money issues.

The client picture is broader than most people assume. Clients include senior citizens, people with disabilities, busy professionals, high net worth individuals, divorcees, widows and widowers, and frequent travelers. One common scenario involves a surviving spouse who suddenly must manage finances that a partner handled for decades. As AARP describes it, when the spouse who managed the money dies and the survivor is struggling to remain independent, family members may not be positioned to help because they are strapped for time or simply live too far away.

A typical client may be someone who was hospitalized and then entered rehabilitation. When they return home after several weeks, they face a new reality and often require a range of in-home services including daily money management, because paperwork has accumulated and bills need to be paid. A daily money manager can come in for several sessions to get bills paid and file important documents, and can arrange to set up bills on autopay so that if clients reenter the hospital or travel, they do not have to worry about payments being missed.

Studies show that bill-paying services can help seniors remain in their homes longer and avoid costly nursing home care. DMMs ensure that bills get paid on time, checks are deposited, and taxes get paid, which helps avoid eviction, foreclosure, utility shutoffs, and other debt trouble.

The Professional Association and Its Standards

The American Association of Daily Money Managers (AADMM) is a national membership organization representing individuals and businesses in the growing profession of daily money management. The vast majority of AADMM members are employed as DMMs providing personal financial services across the full client spectrum. The organization was incorporated as a non-profit on May 4, 1998.

Membership stands at approximately 700 professionals across the U.S. and Canada. AADMM's mission is to support daily money management services in an ethical manner, to provide information and education to members and the public, and to develop a network of dedicated professionals. All members must abide by a code of ethics, and AADMM requires all members to pass a background check before joining or renewing membership, a requirement the board considers a critical element in developing the profession's credibility.

Members also have access to specialized liability insurance, book discounts for professional resources, industry news updates, and various networking opportunities. Individuals looking for a daily money manager can find one by visiting the AADMM website and entering their zip code in the "Find a DMM" section.

Certification: What the PDMM Credential Means

Not every AADMM member holds a certification, and the distinction matters when choosing a professional. Certified DMMs have earned the designation PDMM (Professional Daily Money Manager) by completing coursework on subjects such as Social Security, Medicare, Medicaid, insurance, banking practices, security issues, and analyzing investment statements. They must also undergo a background check and have at least 1,500 hours of experience working as a DMM.

AADMM began its certification program in 2007, and the voluntary program emphasizes both experience in the field and continuing education. Those who meet the requirements and pass the exam earn the PDMM designation. The rigor of that credential, particularly the 1,500-hour experience floor and the topical breadth of the coursework, helps explain why certified DMMs are considered a higher bar of professional accountability.

Education, Webinars, and Professional Development

For DMMs themselves and for those considering the profession, AADMM hosts a variety of events including monthly live webinars, members-only book club meetings, new member webinars, and the AADMM Annual Conference. The catalogue of past recorded webinars covers topics such as Standards of Practice, Types of Expenses, Payroll, Finance, Bookkeeping and Bill Pay, Ethics, and more. Practitioners can even earn continuing education unit (CEU) credits through the recorded webinar library.

For those considering daily money management as a career, AADMM offers a Business Basics two-part webinar series designed for people new to the profession or exploring it as an option. The series sets forth the components needed to perform the duties of a DMM on a day-to-day basis, making it a practical starting point for anyone drawn to this kind of work. For many AADMM members, daily money management is a second career, and what members share is a strong commitment to helping others, which is essential as they become indispensable to clients who rely on them to keep their day-to-day finances running smoothly.

The Positive Aging SourceBook, which has been fostering solutions and connections in the senior services space for more than 35 years, recently hosted a discussion on the profession. In that conversation, moderated by Steve Gurney of the Senior Service Alliance, three experienced DMMs, including Sharon Zissman, Paul Orsinger, and Edward W. Jackson of Phoenix Consulting, LLC, shed light on a profession that fills a critical gap in the lives of millions of Americans yet remains largely invisible to the public.

How to Find and Vet a Daily Money Manager

A good starting point is the AADMM's "Find a DMM" directory, which allows consumers to search by zip code for vetted professionals in their area. When evaluating candidates, the PDMM designation signals that a practitioner has completed substantial coursework, logged at least 1,500 hours in the field, and passed a background check.

In addition to bill payment, daily money managers provide budgeting assistance, tax document organization, bank reconciliations, and creditor negotiations. With client permission, they also establish working relationships with the other professionals in their client's lives, which assures a more synergistic approach to managing the client's overall affairs.

For families navigating an aging parent's finances from a distance, or for professionals whose financial to-do list keeps growing longer, a daily money manager represents something straightforward: someone whose entire job is to ensure that the details of your financial life do not fall apart.

Know something we missed? Have a correction or additional information?

Submit a Tip