DBS beats profit estimates, sees stronger wealth inflows lifting 2026 outlook

DBS posted SGD 2.93 billion in quarterly profit and a record SGD 5.95 billion in income as deposits climbed to SGD 630 billion. The lender said stronger wealth inflows should support its 2026 outlook.

DBS Group Holdings lifted its outlook for 2026 after a first-quarter profit beat, with Singapore’s biggest bank saying stronger wealth inflows and steady deposit growth should help cushion a more uncertain global backdrop. Net profit rose 1% from a year earlier to SGD 2.93 billion, while total income reached a record SGD 5.95 billion, underscoring how wealth management and funding momentum are still feeding earnings at Southeast Asia’s largest lender by assets.

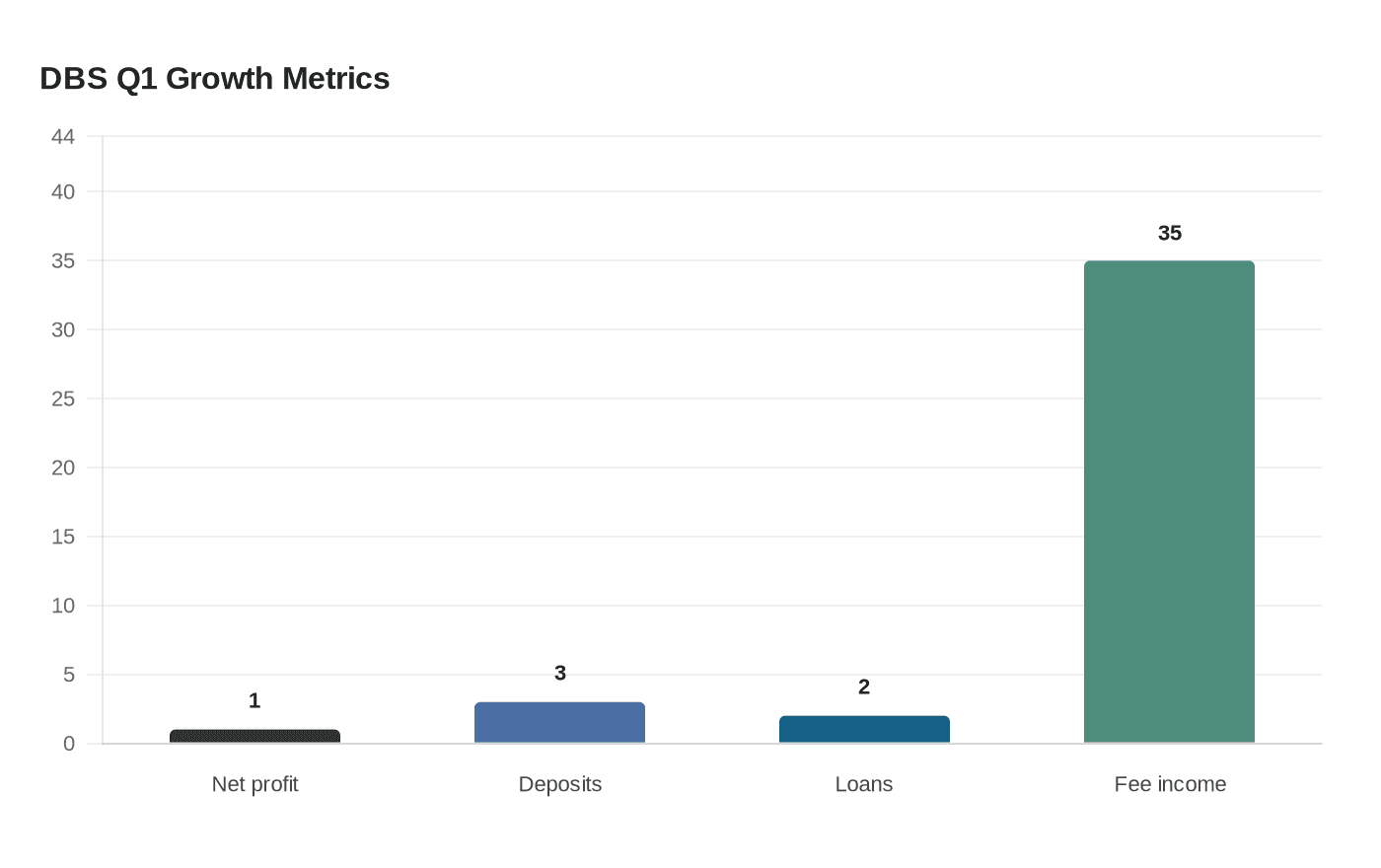

The numbers point to a franchise still drawing money into Singapore even as investors weigh tariffs, geopolitical shocks and softer trade flows across Asia. Deposits rose 3% from the previous quarter to SGD 630 billion, loans increased 2% to SGD 453 billion in constant-currency terms, and the current-account and savings account ratio edged up to 55%. That mix suggests DBS is not relying only on aggressive loan growth; it is also benefiting from a larger, cheaper funding base at a time when regional banks are watching margins closely.

Wealth management was the standout. Commercial-book fee income jumped 35% to SGD 1.48 billion, wealth-management fees hit a record SGD 907 million and treasury customer sales also reached a new high. DBS said those gains helped offset pressure elsewhere, while return on equity held at a strong 17.0%. The board declared a total first-quarter dividend of 81 cents a share, including a 66-cent ordinary dividend and a 15-cent capital return dividend.

Chief executive Tan Su Shan said DBS had very limited direct exposure to the Middle East, but warned that a prolonged conflict could still create second-order risks through higher oil prices and weaker market sentiment. The bank said asset quality remained resilient, with the non-performing loan ratio steady at 1.0% and specific allowances at 14 basis points of loans. DBS also said it expects deposit growth and commercial-book non-interest income to rise in the high single-digit range, while keeping the cost-income ratio in the low-40% area.

For Asian banking, the key question is whether DBS’s inflows reflect durable confidence or a temporary shift into a perceived safe haven. Singapore has long benefited when regional investors and corporates park cash in a stable financial hub, but those flows can reverse quickly if market sentiment improves elsewhere or if volatility eases. DBS’s latest results suggest the bank is still winning that competition for capital, and that Singapore remains one of the region’s main landing places for money seeking scale, liquidity and stability.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?