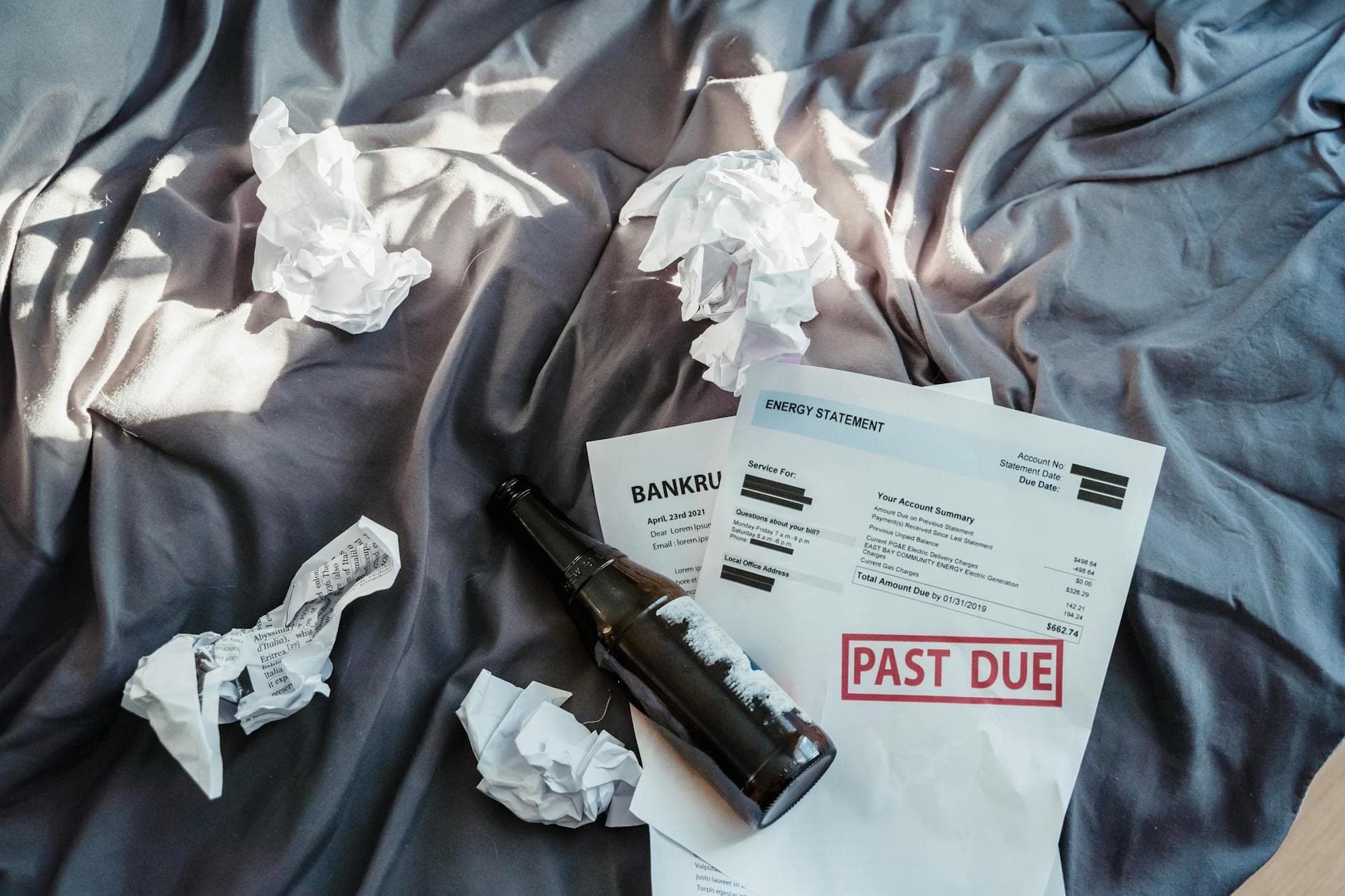

Debt relief can cut balances, but risks fees, taxes, lawsuits

Debt relief can shrink balances, but missed payments can trigger fees, credit damage, lawsuits and a tax bill before the savings arrive.

The promise and the price

Debt relief can lower what you owe, but the path to that result is often full of costs that are easy to miss. Many debt settlement companies tell consumers to stop paying creditors while money is built up for a future settlement, and the Consumer Financial Protection Bureau warns that this can quickly turn into late fees, penalty interest, extra charges and more aggressive collection efforts.

That pause in payments can also damage credit scores and, in some cases, give creditors time to file a lawsuit before any deal is reached. In other words, the consumer may be paying for relief in the form of wrecked credit and legal exposure long before any balance is reduced.

Why not every debt can be settled

Debt settlement is usually designed for unsecured debt, especially credit cards and medical bills. It is not a broad fix for every obligation a household carries, and it generally does not apply to secured debt backed by collateral. That matters because consumers sometimes sign up expecting a full reset, only to learn that major debts may remain outside the program.

Even when a company has a plan, some creditors may simply refuse to negotiate. That means not all debts are likely to be settled, and the consumer can end up paying fees for a result that never fully materializes. The basic promise of simplification can break down fast when one or more lenders say no.

Forgiven debt can create a tax bill

A reduced balance does not always mean a clean finish. The Internal Revenue Service says forgiven or canceled debt is generally treated as income when it is forgiven for less than the full amount, unless an exception applies. That can leave consumers facing taxes on part of the forgiven balance after they thought the worst was over.

This is one of the most overlooked parts of debt relief. A settlement may cut the amount owed to a creditor, but the tax code can still treat the forgiven portion as money received. For households already under strain, a surprise tax bill can undermine the very savings the settlement was supposed to create.

How scams and weak offers trap consumers

The Federal Trade Commission says debt relief scams often target people with significant credit card debt and promise to reduce or eliminate what they owe. Some of these companies charge up-front or monthly fees and do little or nothing to help, leaving consumers worse off than before they signed up.

That risk is not hypothetical. The FTC’s Telemarketing Sales Rule was amended in 2010 to bar for-profit debt relief companies that sell by phone from collecting fees before they have actually settled or reduced a customer’s unsecured debt. The rule reflects a simple concern: consumers should not pay a company before any meaningful debt reduction has happened.

What safer counseling looks like

Nonprofit credit counseling is a different model. The CFPB says these organizations are usually certified and trained in consumer credit, money management and budgeting, and they can help build a personalized plan to solve money problems. In many cases, they use a debt management plan rather than trying to cut principal.

With that approach, consumers make one monthly payment to the counseling organization, which then pays creditors. A plan like this may lower monthly payments by stretching repayment over a longer period or negotiating lower interest rates, which can make it easier to stay current without the credit damage that often comes with settlement.

Warning signs that should make you pause

Before signing anything, look closely for the signs that a debt relief offer may be risky:

- The company tells you to stop paying every creditor without clearly explaining the consequences.

- It promises to erase or sharply reduce debt quickly, especially with little discussion of which debts qualify.

- It wants up-front or recurring fees before any settlement is completed.

- It downplays the chance of late fees, penalty interest, collection calls or lawsuits.

- It does not explain that forgiven debt may be taxable income.

- It talks more about collecting your payments than about a realistic plan for resolving your accounts.

A company that avoids those basics is asking for trust without proving results. Consumers facing serious debt need clarity, not a sales pitch built on hope and delay.

The bigger picture behind the numbers

Debt relief is not a niche product. The CFPB’s 2020 report on debt settlements and credit counseling found that nearly one in thirteen consumers with a credit record had at least one account reported as settled or managed by a credit counseling agency from 2007 through 2019. That same period included a surge in debt settlements during the Great Recession, when the total peaked at $11.4 billion.

Those numbers show how often distressed borrowers turn to debt relief when budgets crack. They also explain why the market attracts both legitimate help and aggressive operators. The Better Business Bureau says some consumers report positive experiences, but complaints remain common and often involve limited results and stacked fees.

The lesson is straightforward: debt relief can cut balances, but the hidden costs can be severe. Credit damage, tax liability, collection pressure and lawsuits can erase much of the benefit if the company is vague, slow or ineffective. The strongest safeguard is to treat any offer that sounds painless as a warning sign, not a promise.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?