Defense startups boom as Anduril, Mach soar, but most face Valley of Death

Anduril and Mach are soaring, but the real test is whether defense startups can move from prototype to production before Washington’s slow cycle catches them.

The money is real, but so is the trap

Defense-tech investors are pricing in a bigger Pentagon footprint, yet the sector’s central question is not who can raise the largest round. It is who can survive the lag between a promising prototype and an actual production program, when hype cools and the federal contracting machine keeps moving at its own pace.

That tension is now visible in the two biggest names in the market. Anduril and Mach Industries have both posted dramatic valuation gains, while the Trump administration’s fiscal 2027 defense request points to a far larger spending pool. The gap between those two facts is where the sector’s winners and losers will be decided.

Anduril’s scale is turning into a durability test

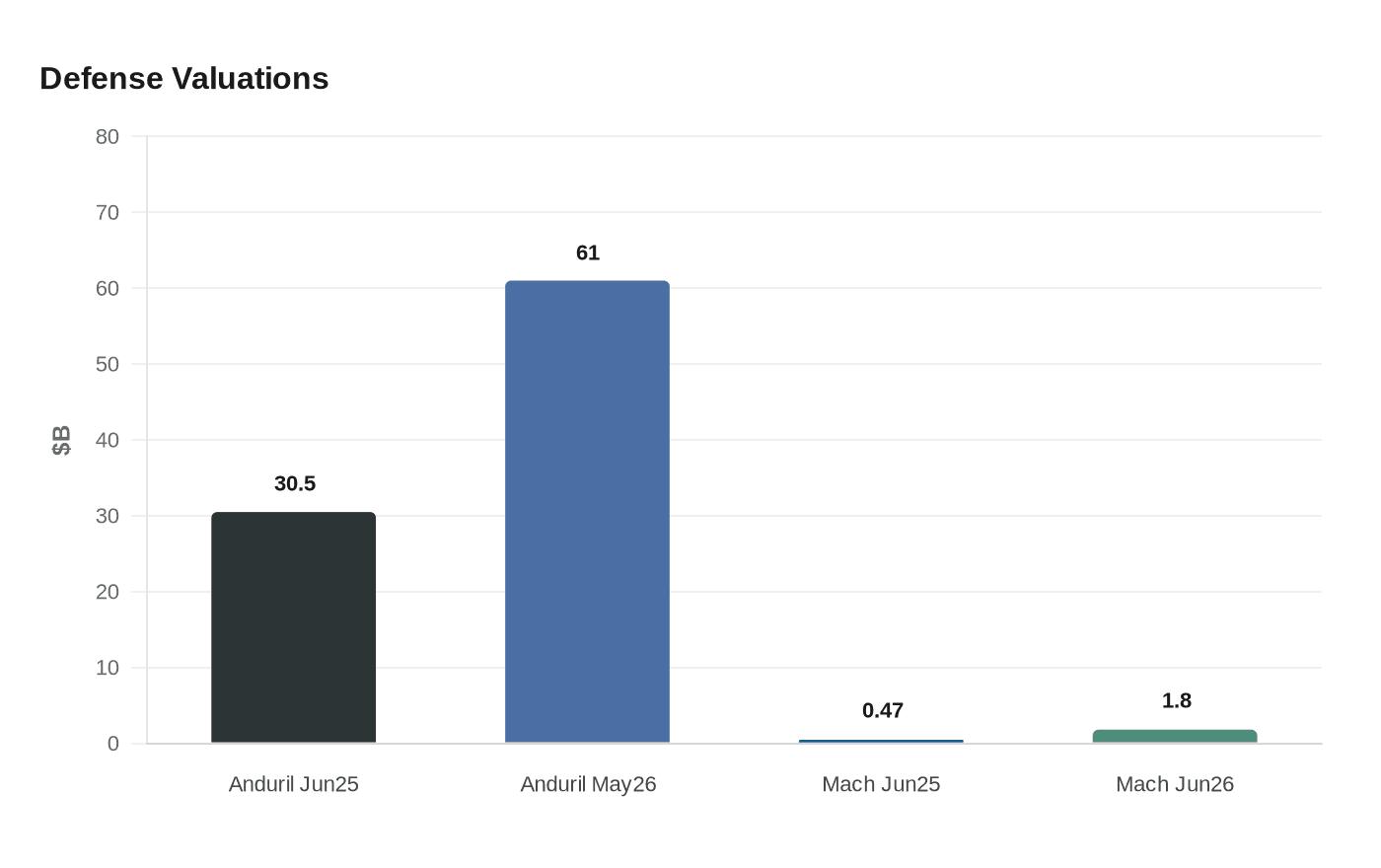

Anduril’s latest raise was a clear signal that investors see something more durable than a standard venture boom. On May 13, 2026, the company announced a $5 billion Series H round that lifted its valuation to $61 billion, up from $30.5 billion in a June 2025 funding round. The company also said its revenue more than doubled to $2.2 billion in 2025 and its workforce nearly doubled over the past year.

Those numbers matter because they move Anduril beyond the category of a speculative defense startup. Revenue at that scale suggests the company is already doing business across a meaningful set of programs, not simply pitching concepts. In a sector where government sales can take years to mature, that combination of growth, capital, and staffing gives Anduril a stronger claim to staying power than many of its peers.

Brian Schimpf’s company is now being treated less like a moonshot and more like a platform that must prove it can keep delivering through procurement delays, budget shifts, and production demands. That is a different challenge from fundraising, and it is the one that will determine whether a $61 billion valuation holds.

Mach Industries shows how fast the market is rewarding momentum

Mach Industries is traveling a steeper and riskier path. On June 1, 2026, the company announced a $300 million Series C round that lifted its valuation to $1.8 billion, roughly four times its June 2025 valuation of $470 million. For a three-year-old defense startup founded by Ethan Thornton, that jump reflects how aggressively investors are chasing the category.

TechCrunch reported that Mach already has five autonomous vehicles in development and has completed a major acquisition, both of which suggest an ambition to build beyond a single product line. That is important in defense, where one-off technical demos are rarely enough. A startup needs systems, manufacturing discipline, and a believable route into procurement if it wants to avoid being remembered as a case study in valuation inflation.

Mach’s rise also shows how quickly the market is moving to fund younger companies before they are fully proven. That can create real strategic advantage, but it can also increase the odds that capital outruns execution. In defense, the difference between those outcomes can be measured not in months, but in budget cycles.

The Pentagon is spending more, but contracting is still the bottleneck

The policy backdrop is undeniably favorable. The Trump administration’s fiscal 2027 defense budget request, released on April 21, 2026, totaled $1.5 trillion in national-defense budgetary resources, a 42% increase from current funding levels. The White House fact sheet said the request included $1.1 trillion in base discretionary budget authority for the Department of War, while defense officials said the proposal also included more than $70 billion for drones and counter-drone systems.

For investors, those figures look like demand confirmation. They suggest that drone warfare, counter-drone technology, and rapid battlefield adaptation are no longer niche bets, but central priorities in Washington. Yet budget requests are not the same thing as procurement awards, and even awards are not the same thing as durable production revenue.

That is why the market’s excitement should be read with caution. A large top-line request can create optimism across the defense ecosystem, but the Pentagon still buys slowly, evaluates cautiously, and often prefers suppliers that can demonstrate reliability over those that can merely demo speed.

The Valley of Death is where many startups will be judged

Ross Fubini, the venture investor who wrote Anduril’s first check, is warning that many of the startups now flooding into defense will not make it through the transition from prototype to production. His point goes to the heart of the industry’s oldest problem: the Valley of Death, the long stretch where a company has finished development but has not yet converted that success into operational use at scale.

The Defense Department created APFIT in fiscal 2022 to help bridge that gap. The program is designed to move innovative projects out of development and into use, with awards ranging from $10 million to $50 million to speed initial production. That kind of support can be decisive for a startup that has built a compelling system but lacks the capital and contracting history to ramp manufacturing on its own.

APFIT also reveals something else: the Pentagon knows the transition is hard. The existence of a formal bridge program confirms that prototype success is not enough. A company still has to prove it can manufacture, deliver, and sustain a system inside the slow-moving realities of federal procurement.

What separates the firms that can last

The current defense-tech surge is creating a wide gap between companies with real pathways and companies that are still mostly riding enthusiasm. The firms most likely to endure share a few traits:

- They already have meaningful revenue, not just product demos.

- They can point to production capacity, or at least a credible path to it.

- They are close enough to Pentagon needs that the budget cycle works in their favor.

- They can survive long procurement timelines without relying on another quick valuation jump.

By that standard, Anduril looks better positioned than most because it already has a multibillion-dollar revenue base and a large workforce. Mach is earlier, faster, and more exposed to execution risk, even as its valuation surge shows how much capital is chasing the category.

The broader market is still entering the hard part. A defense startup can win investor attention in weeks, but Pentagon staying power is earned over years. That is why the current boom should not be mistaken for a permanent reset. In defense, the companies that matter are not the ones that can raise fastest. They are the ones that can make it through the Valley of Death and remain standing when the hype cycle fades.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip