Families Wait Months to Reclaim Money From Struggling UK Care Homes

Roughly 176,000 self-funding care home residents are exposed to a sector where one in four providers risks collapse, leaving families waiting months or years to recover fees.

Grieving families are waiting months, and sometimes years, to recover money paid to UK care home operators, in a consumer-protection failure that legal advocates say is systemic and worsening as the sector's financial foundations crack beneath it.

Around 440,000 people live in care homes across Britain, and approximately 40% of them, roughly 176,000 residents, fund their own care. With fees that can exceed £1,000 per resident per week, the stakes for families who find themselves chasing refunds are enormous. Yet the regulatory framework that should protect them has repeatedly proved insufficient against operators who resist repayment, enter administration, or simply outlast the resolve of bereaved relatives.

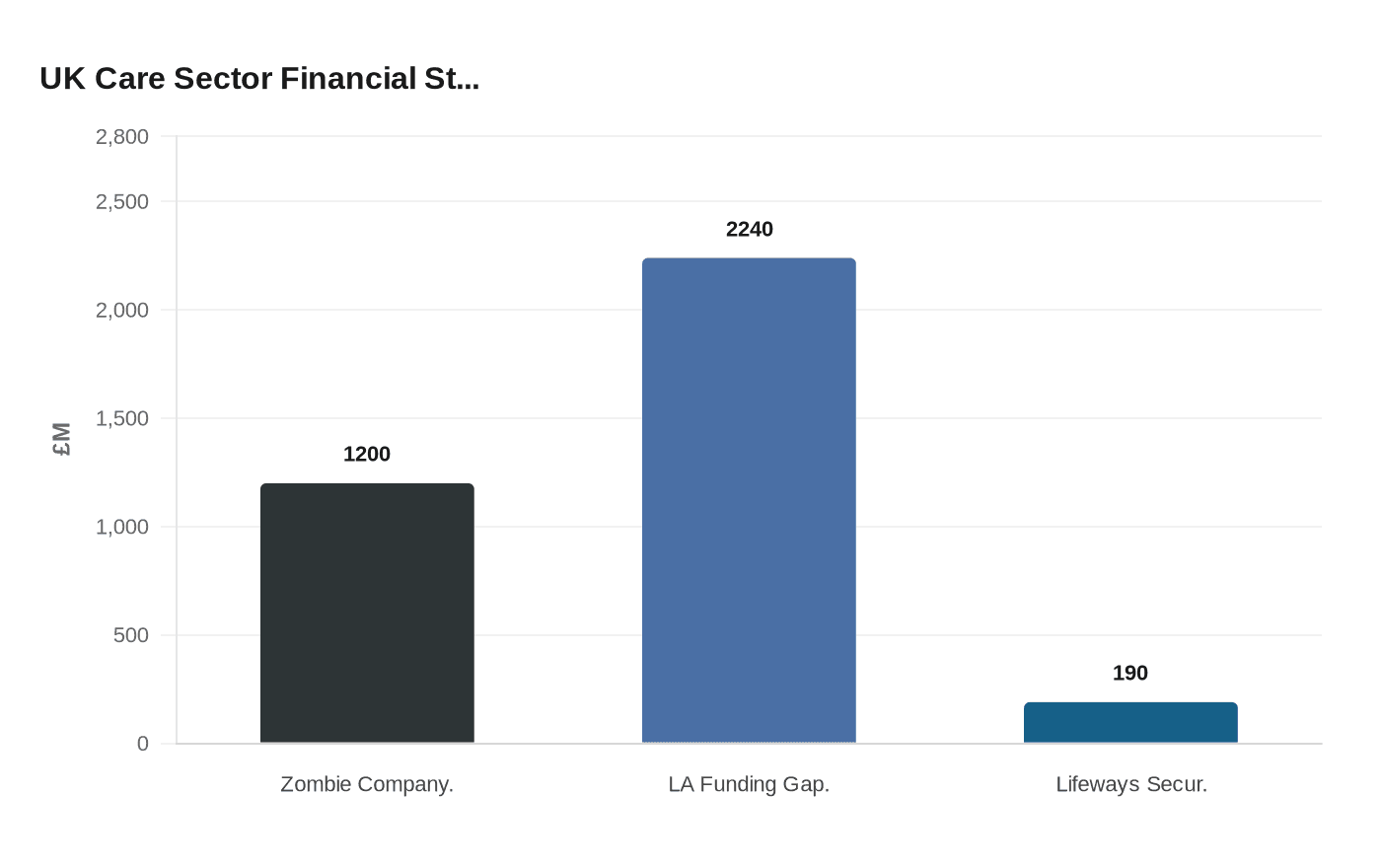

The financial fragility underpinning the problem is severe. An Opus Business Advisory Group analysis found that 3,154 residential care companies, representing 20% of the sector, qualify as zombie companies: technically insolvent, still operating, but carrying a combined deficit of £1.2 billion. One in four care homes in the UK is considered at risk of going bust. In a single recent quarter, 69 home care companies went out of business entirely. Care England has also reported a £2.24 billion gap between average local authority funding rates for 2024/25 and the Fair Cost of Care, a structural underfunding that puts still more providers on the edge.

The pattern of major failures stretches back more than a decade. Southern Cross, then the UK's largest care home chain, collapsed in 2011. Four Seasons went into administration in 2019. In 2023, Lifeways became the first UK healthcare-regulated business to use a formal restructuring plan, having accumulated approximately £190 million in secured debt while supporting 4,200 residents across its homes. Each collapse leaves families as unsecured creditors, pushed to the back of an administration queue that can take years to resolve.

When insolvency is not the issue, operator resistance often is. The Competition and Markets Authority had to launch formal court proceedings against Care UK after the company initially refused to refund residents who had been charged a compulsory upfront fee on top of their NHS Continuing Healthcare funding. The CMA ultimately secured more than £1 million in refunds for those residents. Michael Grenfell, the CMA's Executive Director of Enforcement, stated: "Older people receiving Continuing Healthcare funding are some of the most vulnerable in our society and should not be expected to pay extra fees towards their essential care." Care UK subsequently committed to stop charging the additional fee and to repay eligible residents, with the CMA's redress powers applying from 1 October 2015 onwards.

The legal basis for challenging unfair charges exists but is under-used. The Consumer Rights Act 2015 and the Unfair Terms in Consumer Contracts Regulations both apply to care home contracts, covering how deposits must be held and refunded, how disputes must be handled, and when upfront payments can legitimately be required. Critically, the right to pursue a refund does not expire on death: solicitors at firms including Steene Law, Just Caring Legal, and Farley Dwek have all confirmed that estates can pursue claims after a resident has died, a fact most families never learn.

A further complication arises when NHS Continuing Healthcare funding is awarded retrospectively. Families who paid care fees out of pocket while an eligibility assessment was pending must then seek reimbursement separately from their relevant Integrated Care Board, a process that runs on a different track from any dispute with the care home operator and adds a further layer of bureaucracy to an already exhausting process.

Families who believe they are owed money should act before memories fade and documentation is lost. The starting point is gathering the original contract signed on admission, every invoice and receipt for fees paid, and any written correspondence with the operator. Where NHS Continuing Healthcare was involved, the relevant ICB should be contacted directly to request a retrospective review. Complaints about unfair contract terms or refund delays can be referred to the CMA or, for regulated care quality concerns, to the Care Quality Commission. If an operator is in administration, a formal creditor claim must be submitted to the appointed insolvency practitioner within the stated deadline, as late claims are routinely excluded.

The Insolvency Service recorded company insolvencies in England and Wales running 11% higher in January 2025 than in January 2024, a trajectory that suggests the queue of families chasing money from failed or failing providers is likely to lengthen before it shortens.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?