Global art market contracts again as high-end sales plunge

High-end auction sales fell 45% in 2024 as global art-market value slipped to $57.5 billion, deepening doubts about the gallery-fair model.

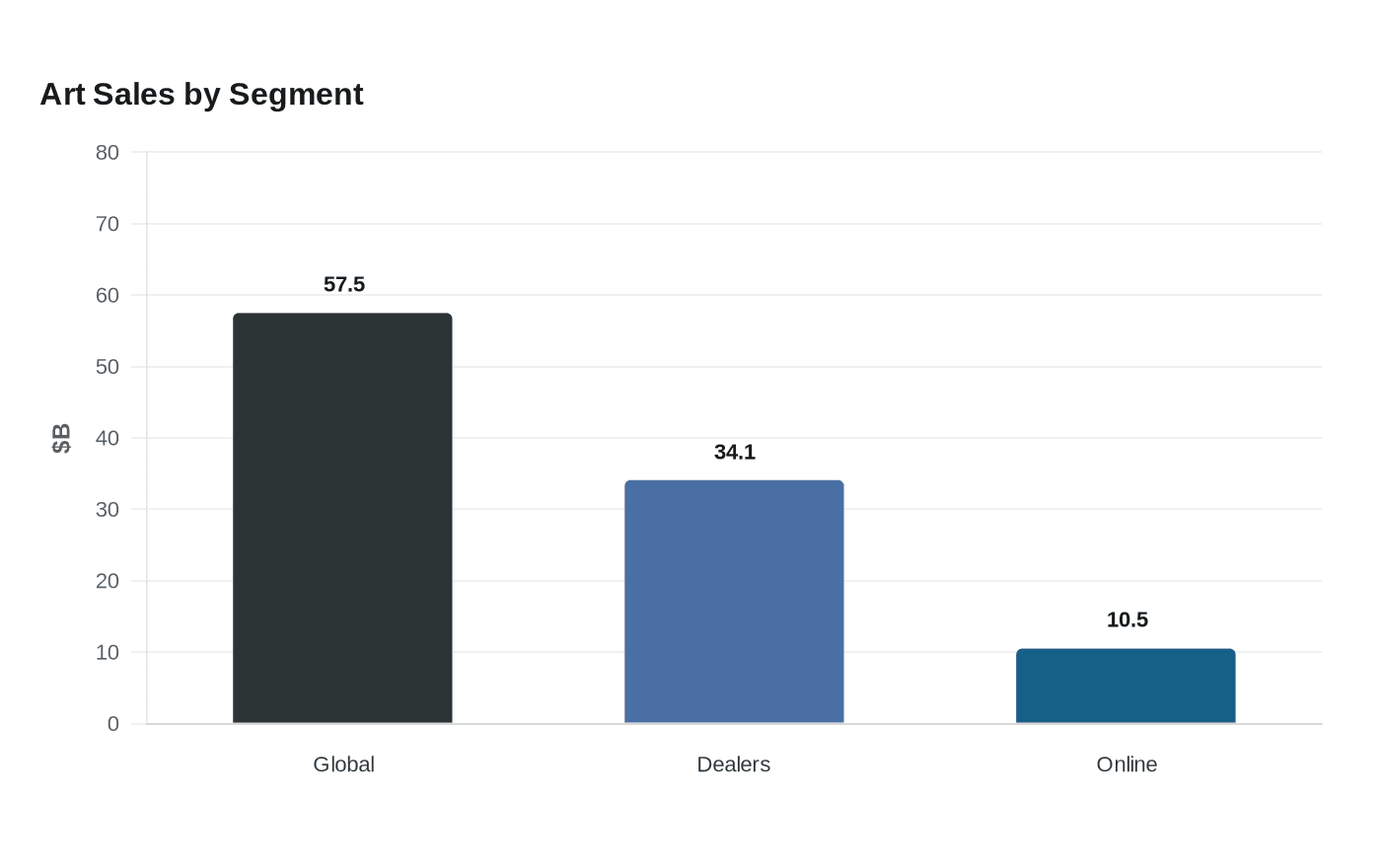

The art market’s center of gravity moved lower in 2024 even as more works changed hands, a sign that volume is not replacing lost value at the top. Global sales fell 12% to an estimated $57.5 billion, and works auctioned for more than $10 million dropped 45% by value after a 40% decline the year before.

That slide hit the dealer sector and public auctions in different ways. Dealer sales fell 6% to $34.1 billion, while public auction sales plunged 25%. Yet transactions rose 3%, and the number of items sold at the lowest end of the market increased 3% to 40.5 million, underscoring a market where activity is holding up even as prices soften. Online sales also fell 11% to $10.5 billion, though that remained well above pre-pandemic levels.

For galleries, the strain is not just the headline contraction. The report said market activity stayed concentrated at lower price levels, while some of the highest-end dealers posted among the steepest value declines. Industry commentary around the report pointed to higher operating costs as an added burden, with the constant cycle of fairs and openings making the business harder to sustain. Tim Blum turned that pressure into a public reckoning in 2025 when he said he would “sunset” Blum’s traditional gallery model after more than three decades.

Blum and Jeff Poe founded Blum & Poe in Santa Monica in 1994, later opening in Tokyo in 2014 and rebranding as BLUM in 2023. Blum’s retreat became a symbol of a wider recalibration across the trade, where closures, downsizing and strategic pauses have followed the post-pandemic boom of 2021 and 2022. The 2025 report framed 2024 as a year of recalibration rather than a one-off dip, with the United States remaining the strongest market even as China and Hong Kong saw major auction declines and the United Kingdom held third place.

The deeper question is whether the old gallery-fair model can survive a market that now depends less on a narrow band of trophy lots and more on a dispersed base of lower-value sales. Women artists continued to gain representation, but parity had not been reached, a reminder that structural change is happening even as the market contracts. For galleries, artists and mid-market dealers, the next phase may be defined less by rebound than by which business models can still bear the costs of staying visible.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip