Goolsbee Says Fed Needs More Evidence Before Cutting Rates

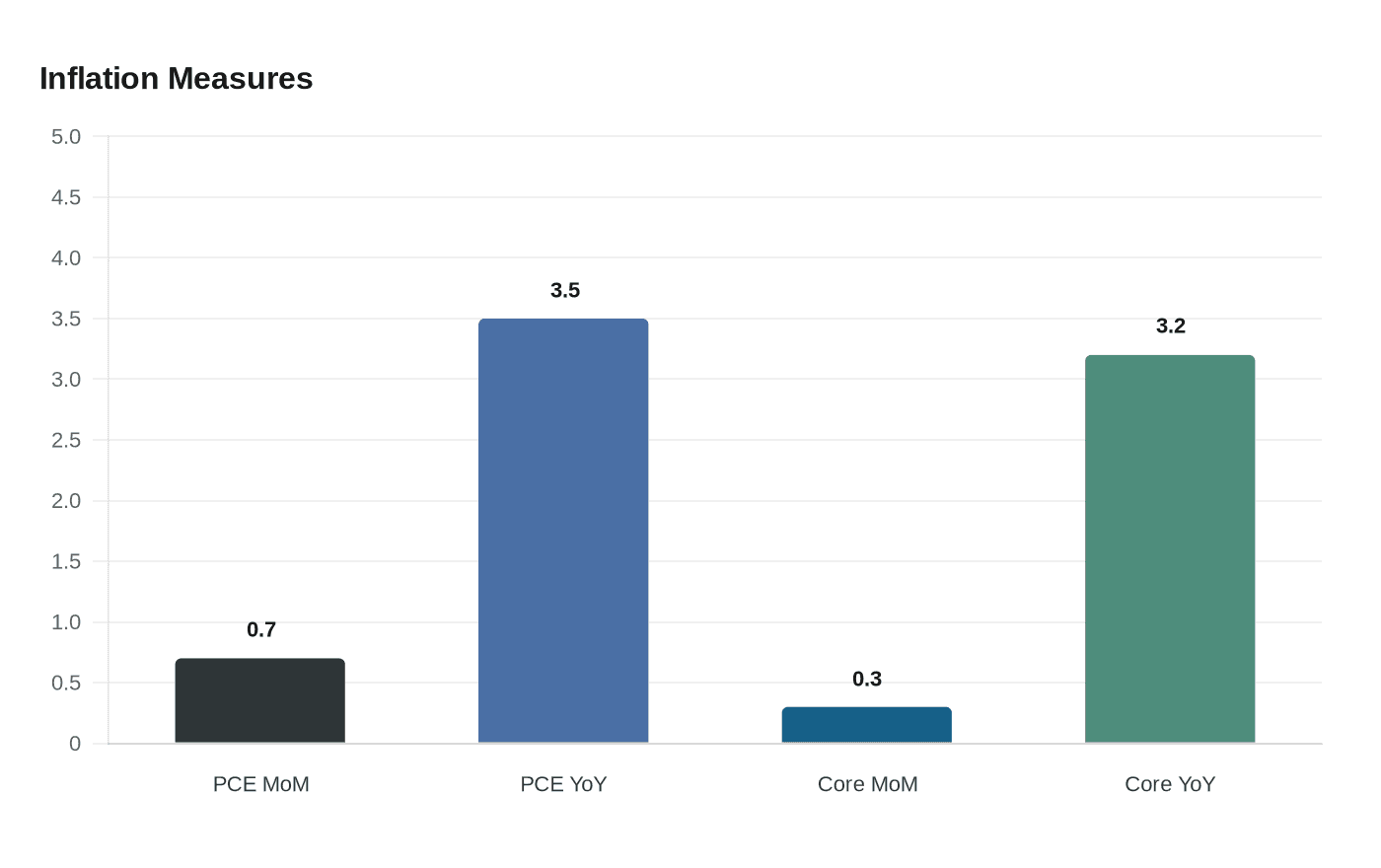

Hotter prices are keeping cuts off the table, with March PCE at 3.5% and a divided Fed signaling no rush to ease.

Hotter prices are keeping mortgage, credit card and small-business borrowing costs elevated, and Chicago Federal Reserve President Austan Goolsbee said that is exactly why the central bank needs more evidence before cutting rates. March’s personal consumption expenditures price index, the Fed’s preferred inflation gauge, rose 0.7% from February and 3.5% from a year earlier, the sharpest annual increase since May 2023.

Goolsbee called the latest inflation readings “bad news” and said the Fed needs assurance that price pressures are moving back toward its 2% target before easing policy. He said the composition of inflation “doesn’t look good,” because some of the pressure is showing up in service sectors that are less directly affected by tariffs or oil shocks. That matters because persistent service inflation usually signals broader price stickiness, not just a temporary jump in imported goods or energy.

The new data also complicated an already divided policy debate in Washington. The Federal Reserve held the federal funds rate in a range of 3.5% to 3.75% at its April 29 meeting, and the 8-4 vote was the most split since 1992. Three policymakers dissented from language suggesting the next move would probably be a rate cut, while one wanted an immediate cut. Goolsbee said that kind of split shows how difficult forward guidance becomes when the outlook is changing quickly.

The Fed’s April 29 statement said inflation remained elevated in part because of recent increases in global energy prices, while economic activity was expanding at a solid pace. It also said job gains had remained low on average and unemployment had changed little in recent months, underscoring the balancing act facing Jerome Powell and his colleagues as they weigh labor-market resilience against stubborn inflation. Goolsbee said some of the price pressure was tied to higher oil prices connected with the U.S.-backed war with Iran, adding another layer of uncertainty to the policy path.

Markets have already moved toward a more cautious view. Traders were pricing in no rate cuts in 2026 around the time of the April 29 decision, suggesting investors expect borrowing costs to stay high for longer if inflation does not cool quickly. The latest March figures reinforce that expectation, especially with core PCE also up 0.3% on the month and 3.2% from a year earlier.

For households and businesses, the policy message is straightforward: rates are unlikely to fall until inflation shows more convincing progress. More data on energy prices, service-sector inflation and the next round of consumer spending will help determine whether this pause becomes a prolonged hold or the start of a cautious easing cycle.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)