HELOC rates may ease as Fed holds borrowing costs steady

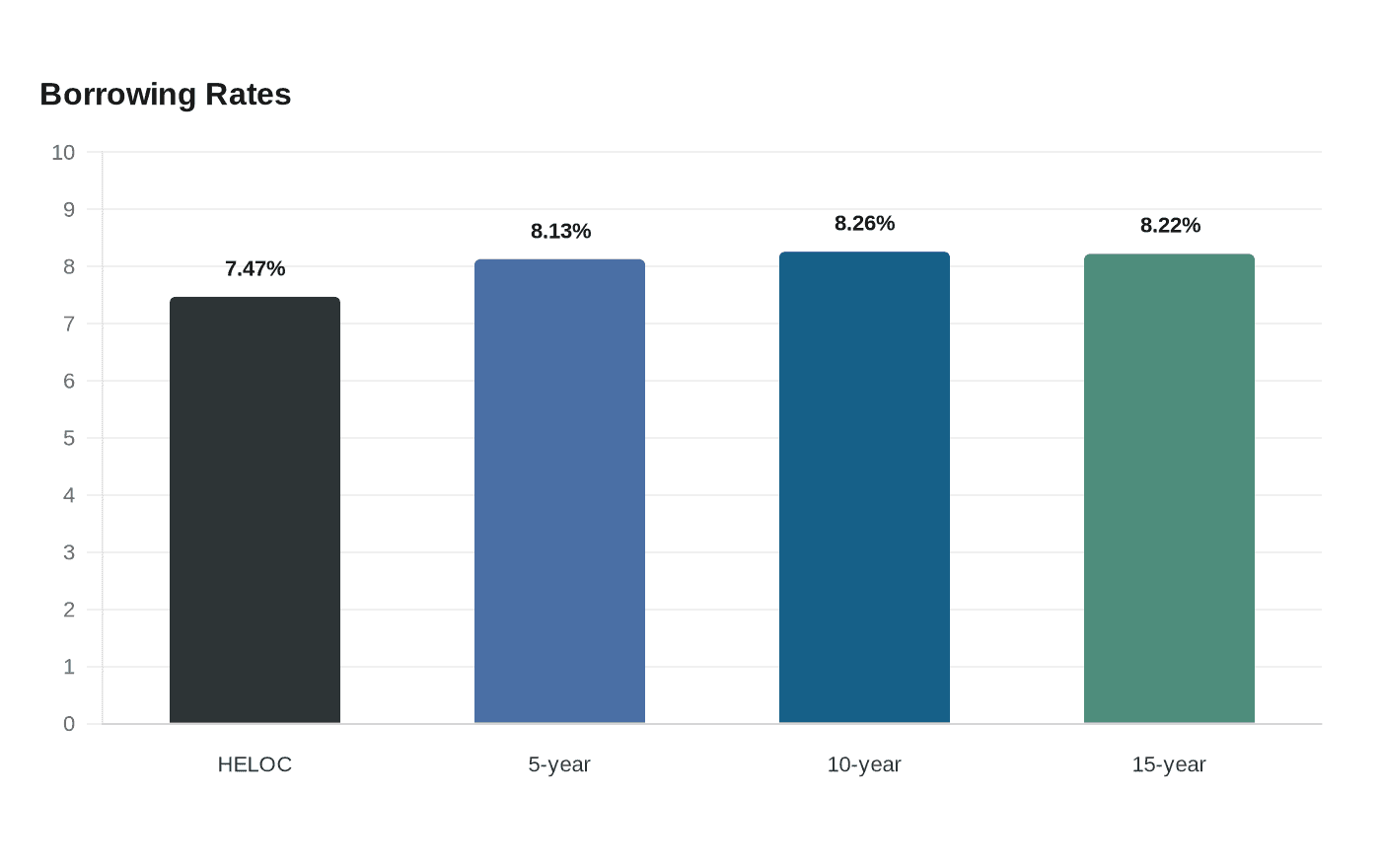

A $30,000 HELOC averages 7.47%, versus 8.22% for a 15-year home equity loan, sharpening the borrow-now-or-wait decision for summer borrowers.

Homeowners deciding whether to tap equity now or wait for lower borrowing costs are staring at a narrow spread. Bankrate put the national average HELOC rate at 7.47% on June 17, while average home equity loan rates for the same $30,000 balance ran 8.13% on five-year loans, 8.26% on 10-year loans and 8.22% on 15-year loans. On a $30,000 balance, that works out to about $187 a month in interest-only HELOC charges, versus roughly $611 for a five-year loan, $368 for a 10-year loan and $291 for a 15-year loan, before fees or principal changes on the line of credit.

The broader rate backdrop still points back to the Federal Reserve. The Fed left its target range at 4.25% to 4.50% in its June 18, 2025 statement, and the Fed’s H.15 data show a 6.75% prime rate, the benchmark that drives most HELOC pricing. That connection matters because HELOCs can reset as prime moves, while home equity loans lock in a fixed rate and fixed payment from the start.

Borrowing demand has not faded even as rates remain elevated by pre-2022 standards. The St. Louis Fed said the share of HELOC borrowers among people with housing debt rose 18% from the first quarter of 2022 through the first quarter of 2026, and inflation-adjusted per-borrower HELOC amounts rose 14% over that span. The New York Fed said HELOC balances climbed by $12 billion in the first quarter of 2026 to $446 billion, the 16th straight quarterly increase, showing that households continue to lean on home equity as a funding source.

That helps explain why many owners with low-rate first mortgages still prefer borrowing against equity instead of refinancing. Freddie Mac’s latest survey put the 30-year fixed mortgage at 6.47% and the 15-year at 5.81% on June 18, 2026, leaving little incentive for a refinance if the goal is cash rather than a new mortgage. For borrowers who want flexibility and may not need every dollar at once, a HELOC can still offer cheaper access up front; for borrowers who want certainty, the fixed payment on a home equity loan is the cleaner fit.

The risk later this summer is that borrowers wait for relief that never arrives. If the Fed keeps borrowing costs steady, HELOCs are likely to stay tied to prime, and if home-price gains slow further, available equity can tighten even though FHFA says its House Price Index tracks single-family values across all 50 states and more than 400 American cities. In that case, the bargain shifts quickly from rate savings to lost borrowing capacity.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip