How much $12,000 earns in a high-yield savings account versus traditional savings

Move $12,000 from 0.6% savings to a 4.15% high-yield account and you could earn about $435 more a year, with FDIC coverage intact.

A $12,000 balance leaves a surprisingly large amount of cash on the table in a traditional savings account. At Bankrate’s average 0.6% APY, that money earns only about $6 in a month, while a top 4.15% APY high-yield account from Forbright Bank generates about $41.50 over the same period. The annual gap is even starker: about $72.20 versus $507.58, or roughly $435.38 more by moving the money into the higher-yield account.

What $12,000 earns at current rates

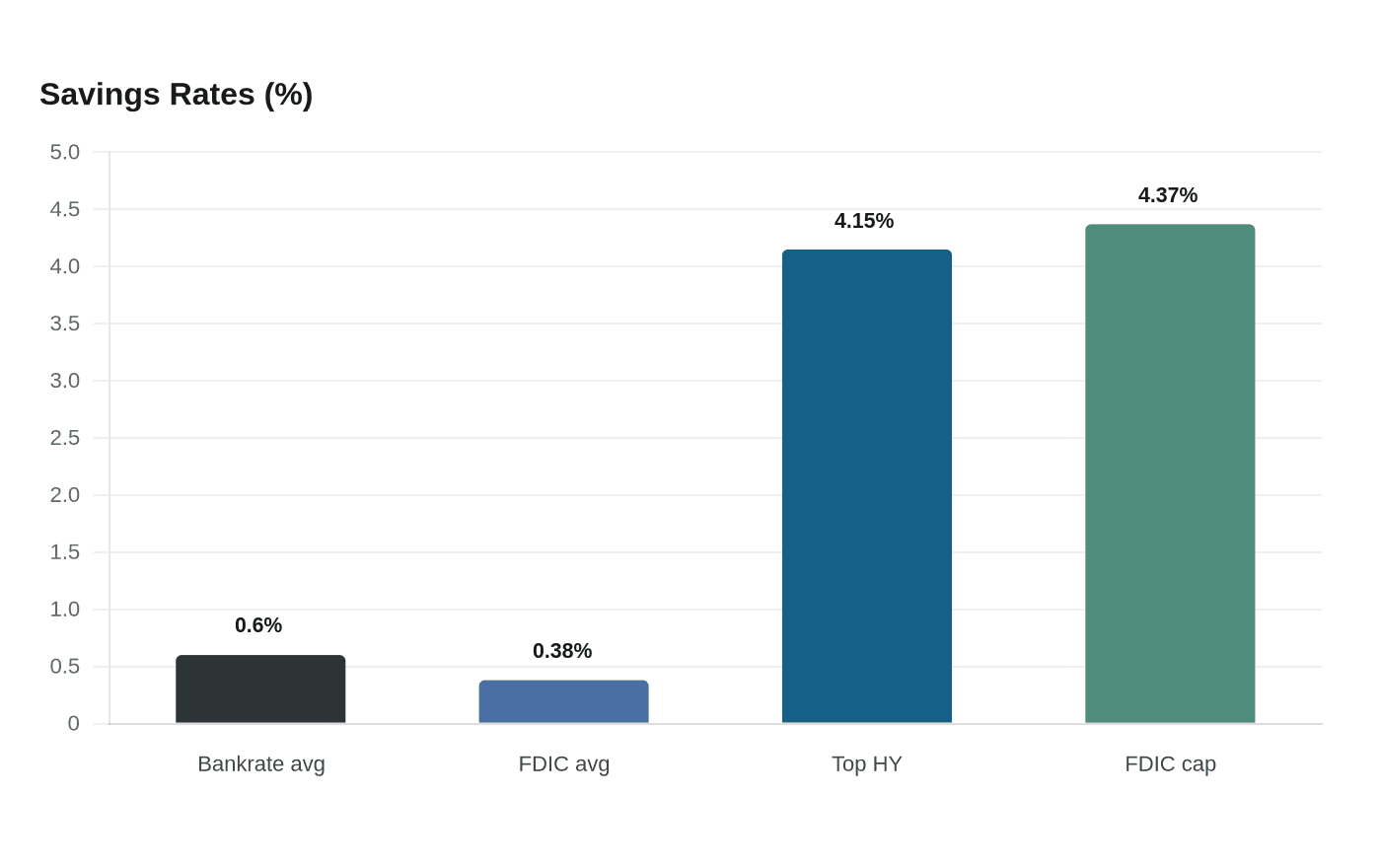

Bankrate’s survey of institutions puts the national average savings yield at 0.6% APY as of July 9, 2026, while the FDIC’s June 15, 2026 rate sheet shows a national savings rate of 0.38% and a rate-cap adjusted national rate cap of 4.37% for savings accounts. The top posted high-yield rate from Bankrate sits at 4.15% APY, which is still below that FDIC cap-adjusted benchmark but far above what most traditional savings accounts pay.

Why high-yield savings still works for emergency money

High-yield savings accounts are usually recommended for emergency funds because they preserve easy access while paying a better return than a standard savings account. Many of the best high-yield accounts do not charge fees and have low minimum deposit requirements, which keeps them practical for money you may need on short notice. That combination is especially relevant when households are trying to stretch every dollar: Bankrate’s 2026 Emergency Savings Report found that 29% of Americans have more credit card debt than emergency savings.

Emergency cash does two jobs at once. It has to stay liquid enough to cover a car repair, medical bill, or job disruption, but it also should not sit idle earning almost nothing when higher-yield options are available. For a $12,000 cushion, moving from a traditional account to a high-yield one produces more interest without forcing you into market risk.

The fine print that can shrink the payoff

The Consumer Financial Protection Bureau requires advertisements for tiered-rate accounts to state the APY for each tier and the corresponding minimum balance requirements. Fees can reduce earnings. Some banks advertise a top APY only for a certain balance band, while lower tiers may pay less.

Withdrawal rules also deserve attention. Banks and credit unions can charge fees for making too many withdrawals or transfers in a month, withdrawing too much money, or dropping below a minimum balance. A high-yield savings account is meant to be accessible, but the account agreement can shape how convenient that money really is.

How safe the money is

For most savers, the safety question is straightforward: FDIC insurance covers deposits up to at least $250,000 per depositor, per ownership category, at each FDIC-insured bank. No depositor has lost a penny of FDIC-insured funds since the agency was founded in 1933. That means the main risk in choosing a high-yield savings account is usually not principal loss, but rate changes, fees, and account rules.

If your balance is under that insurance limit, the decision is less about safety than efficiency. A $12,000 emergency fund is well within FDIC coverage, so the choice comes down to how much interest you want that cash to earn while it waits.

Whether the headline yield is likely to last

Savings rates are variable, which means banks can raise or lower them over time. APYs may have changed since they were last updated and can vary by region for some products, and Bankrate’s 2026 forecast says top savings and money market yields are expected to keep drifting lower. That makes the current 4.15% headline attractive, but not permanent.

Treat that rate as a moving target rather than a guarantee. CFPB disclosure rules require banks to spell out APYs, balance thresholds, and fee structures across products and tiers, so the headline rate should be checked against the account terms that actually govern your money. For a saver parking $12,000, the reward for shopping carefully is immediate: hundreds of dollars a year in extra interest, with federal insurance still in place.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?