How much an $80,000 CD could earn in one year

An $80,000 CD can earn thousands in a year, but the real question is whether the extra yield is worth locking up cash.

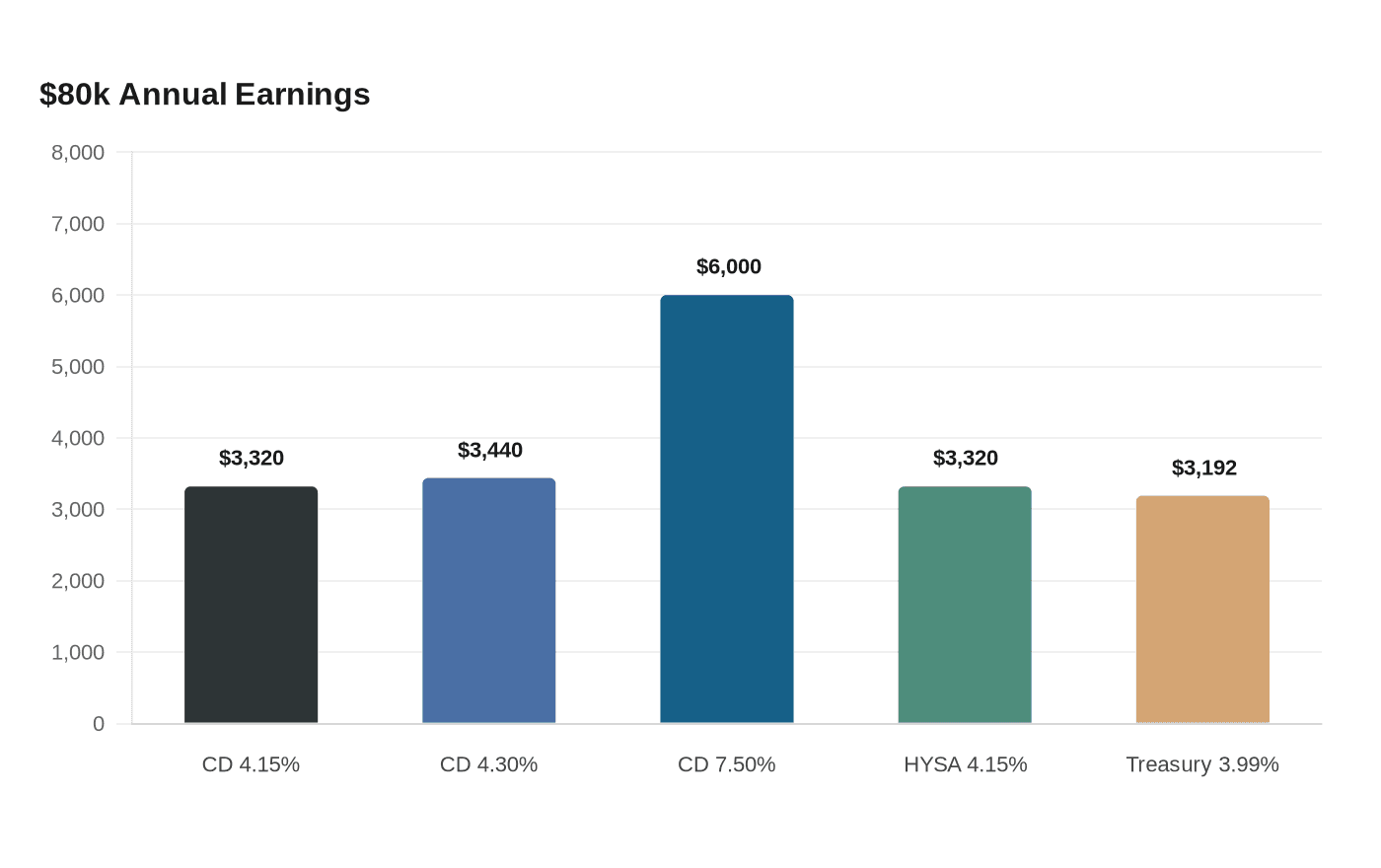

On an $80,000 deposit, today’s one-year CDs are generally paying about $3,320 to $3,440 a year, with a 7.50% outlier at SF Fire Credit Union paying about $6,000. The catch is that the gain over a top high-yield savings account is small, and the edge over inflation is smaller still.

The one-year math on $80,000

Here is the practical comparison for a saver with $80,000 ready to park for a year:

- At 4.15% APY, an $80,000 one-year CD earns about $3,320.

- At 4.30% APY, the same deposit earns about $3,440. That is NerdWallet’s current top CD rate, offered by Connexus Credit Union.

- At 7.50% APY, the deposit earns about $6,000. Bankrate is tracking that rate at SF Fire Credit Union, but it is an outlier, not the norm.

- At 4.15% APY in a top high-yield savings account, the same $80,000 also earns about $3,320, which makes the liquidity difference more important than the rate difference.

- At a 1-year Treasury yield of 3.99%, the deposit earns about $3,192. Treasury’s daily curve put the 1-year rate at 3.99% on June 24, 2026.

Against inflation, the picture is tighter. The Consumer Price Index rose 4.2% over the 12 months ending May 2026, so a 4.30% CD barely outpaces price growth before taxes, by about $80 on $80,000. A 4.15% savings rate trails that inflation pace by about $40 on the same principal, and a 3.99% Treasury falls short by about $168.

Where the market is actually pricing CDs

The top of the CD market is clustered around 4%, not 7%. The best one-year CDs in June 2026 are running up to 4.15% APY at Bankrate and 4.30% APY at NerdWallet, with the 4.30% offer from Connexus Credit Union. Offers are also spread across terms: Consumers Credit Union at 4.25% for seven months, OMB Bank at 4.25% for five months, NASA Federal Credit Union at 4.20% for 49 months, and TAB Bank at 4.20% for five years.

That spread matters because CD rates are not uniform across terms. A short-term rate can beat a longer-term one, and a headline best rate can sit on an unusual term length or a specific credit union membership requirement.

Why the lockup is the real tradeoff

A CD pays a fixed rate for a set term, which is exactly why savers use it when they want certainty. CD terms can run from three months to 10 years, and early withdrawal penalties typically equal 3 to 12 months of interest. That penalty structure can erase a big part of the gain if the money has to come out early, so the best CD is the one that matches cash you truly will not need before maturity.

FDIC insurance softens the credit risk but not the liquidity risk. The standard coverage limit is $250,000 per depositor, per FDIC-insured bank, per ownership category, so an $80,000 CD sits comfortably inside the insured range if it is held in one category at one bank.

Why the Fed and inflation still matter

The rate backdrop explains why CDs are still paying around 4%. The Federal Reserve held the federal funds target range at 4.25% to 4.50% on July 30, 2025, then lowered it to 4.00% to 4.25% on September 17, 2025. When policy rates ease, bank deposit rates usually follow.

Inflation is the other half of the math. With CPI up 4.2% over the past 12 months, a CD yielding 4.30% is only barely ahead in nominal terms, while a 4.15% savings account and a 3.99% Treasury sit just below that pace.

Taxes and the final decision

The IRS treats interest from CDs as taxable income, and taxes can be due each year the interest is earned, even before the CD matures. That means the advertised APY is not the amount you actually keep, especially if your earnings push you into a higher tax bracket or if you owe state income tax as well.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?