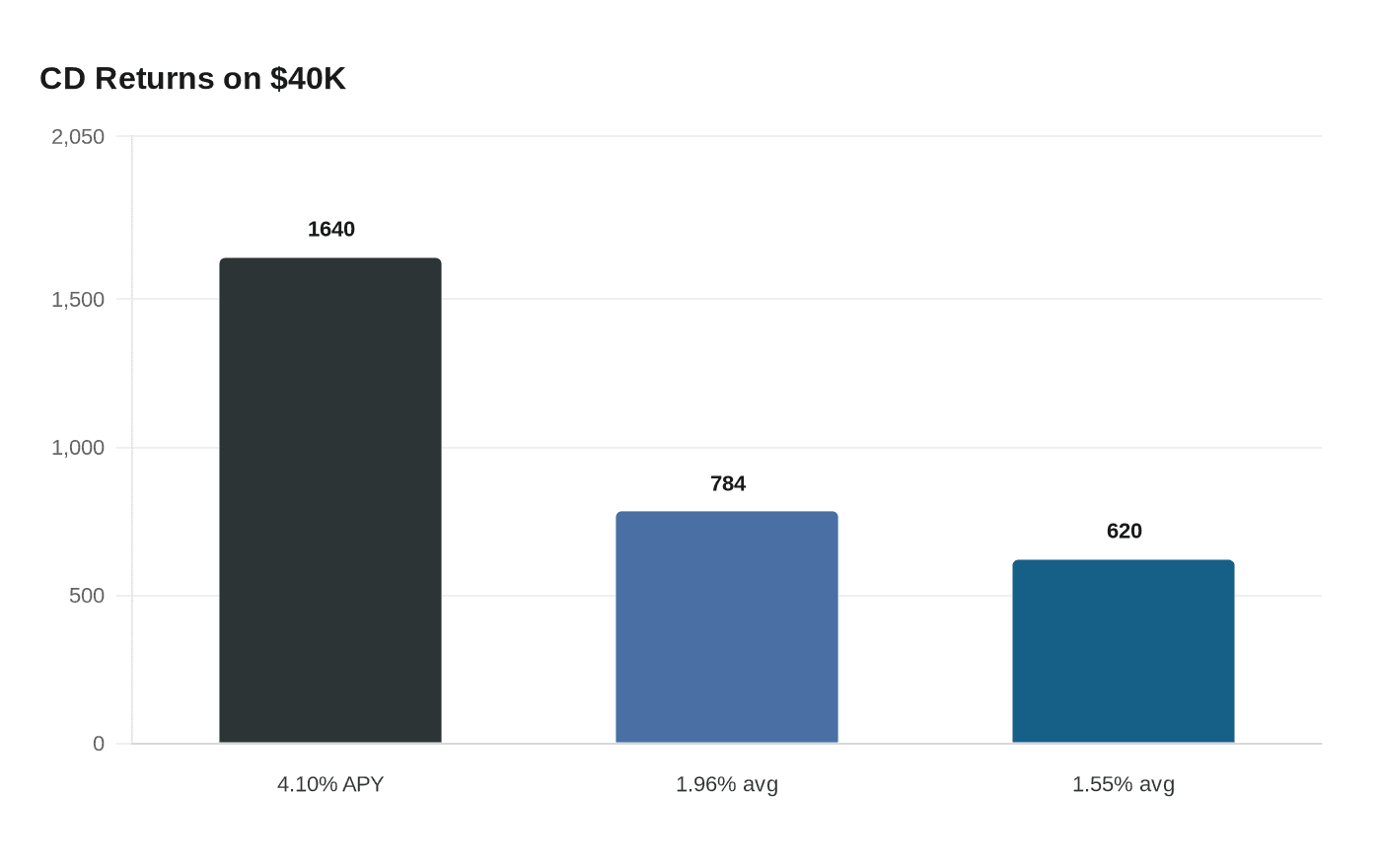

How to build emergency savings while paying down debt

Build a starter cushion before you chase every last debt dollar. One surprise bill can force you back into costly borrowing, undoing months of progress.

How to decide your emergency-fund target

Paying down debt and building cash at the same time is a balancing act, not a moral test. If you send every spare dollar toward a credit-card balance and then get hit with a car repair, medical bill, or job loss, you may be right back where you started, only with new interest charges layered on top. The smarter move is to set an emergency-fund target that matches your job stability, your debt rate, and how easily you can access credit.

The most widely cited benchmark is three to six months of living expenses. But that rule is not meant to be rigid, and federal guidance is broader than a single number: the Consumer Financial Protection Bureau describes emergency savings as cash reserved for unplanned expenses or financial emergencies, including car repairs, home repairs, medical bills, or a loss of income. That definition matters because the real job of emergency savings is not to maximize returns. It is to keep one surprise from becoming a long, expensive debt spiral.

Why the tradeoff matters

The case for keeping some cash on hand is stronger than it looks. In the Federal Reserve’s 2025 Survey of Household Economics and Decisionmaking, fielded in October 2025, 55% of adults said they had enough emergency savings to cover three months of expenses. The Fed also said the share of adults who would pay an unexpected $400 expense with cash or the equivalent was unchanged from 2022 and 2023, which suggests that many households still operate with very limited buffers even when broader savings measures appear stable.

That fragility shows up in other surveys too. Bankrate reported on March 26, 2025, that 37% of Americans tapped emergency savings in the prior year. CNBC reported in 2025 that 1 in 3 Americans do not have an emergency fund, and the median emergency-savings balance was just $500. Those numbers help explain why the old advice to save up three to six months of expenses before attacking debt can backfire for people carrying credit-card balances: the interest on that debt can compound faster than cash savings earns returns.

Choose your target based on your risk profile

The right emergency-fund target depends on how much income shock you can absorb before you are forced to borrow again. If your job is stable, your expenses are predictable, and your debt is low-cost, you may not need to halt debt repayment while building a full six-month reserve. In that case, a smaller starter fund can buy you breathing room while you keep making extra debt payments.

If your income is variable, your industry is vulnerable to layoffs, or a missed paycheck would strain your budget, your target should move closer to the three-to-six-month benchmark. The same is true if your essential expenses are high relative to income or if your access to cheap credit is limited. In those cases, a bigger cash buffer is not a distraction from debt payoff. It is a defense against falling back into more expensive borrowing.

A practical decision rule

Use these questions to set your target:

- How stable is your job? If your income is steady and replacement work would be easy to find, you can usually start with a smaller cash cushion.

- How expensive is your debt? If you are carrying high-interest credit-card balances, every month you leave that debt untouched costs you. That makes a starter emergency fund useful, but it also argues for aggressive repayment once you have some cash on hand.

- How available is credit? If you can only cover an emergency by swiping a card with a high rate, you need more cash in reserve. If you have reliable access to low-cost credit, your cash target can be lower, though not zero.

- How big would a typical surprise bill be? The Fed’s $400 example is a useful reminder that even a modest shock can force a borrowing decision. If a few hundred dollars would break your budget, your emergency fund is too thin.

Start small, then keep building

The Consumer Financial Protection Bureau’s Start Small, Save Up initiative was launched to encourage consumers to create, maintain, and grow emergency savings accounts as part of overall financial well-being. That approach is especially useful when you are still paying down debt, because it turns emergency savings into a habit rather than a finish line you never reach.

The point is not to wait until debt disappears before you save. It is to create a cash cushion early enough to prevent another round of emergency borrowing. A small reserve can keep a flat tire, a medical copay, or a broken appliance from becoming a new balance on a high-interest card. Once that first layer is in place, you can keep increasing the cushion while still making steady debt payments.

How to split each extra dollar

There is no universal split, but the logic is straightforward: put enough toward savings to stop the next emergency from becoming new debt, then direct the rest toward the most expensive balances. If your debt carries a high rate, especially on credit cards, prioritizing debt without any cash reserve is risky. If your debt is lower-cost and your household is vulnerable to income swings, the emergency fund should carry more weight.

For many people, the best sequence is:

1. Build a starter emergency fund.

2. Keep making minimum debt payments.

3. Send additional cash to the highest-interest debt.

4. Increase savings again as balances fall and income rises.

That approach keeps you from choosing between two bad outcomes: a debt payoff plan that collapses after one emergency, or a savings plan that ignores punishing interest charges for too long.

What the latest data says about household resilience

The 2025 Fed survey, conducted among nearly 13,000 adults, suggests that emergency-savings behavior has not shifted dramatically from the prior two years. The share of people who could handle a $400 expense with cash or the equivalent was unchanged, which is a reminder that many households still live close to the edge even when headline savings measures look stable. The broader lesson is that emergency savings is not just a personal budgeting issue. It is a measure of how much financial shock a household can absorb without taking on new debt.

That is why a sensible plan should be built around risk, not perfection. If your income is fragile, aim higher on savings. If your debt is costly, move faster on repayment once you have a usable cushion. If your credit access is poor, keep more cash. If your job is secure and your debt is manageable, you can probably pursue a smaller reserve while accelerating payoff.

The right answer is not to choose between savings and debt reduction. It is to prevent one emergency from undoing both. A targeted cash buffer, built early and raised over time, gives you the best chance to break the cycle of borrowing, repay debt on your own terms, and keep the next surprise from becoming a financial setback.

Know something we missed? Have a correction or additional information?

Submit a Tip