Short-term CDs still top 4%, $40,000 can earn solid returns

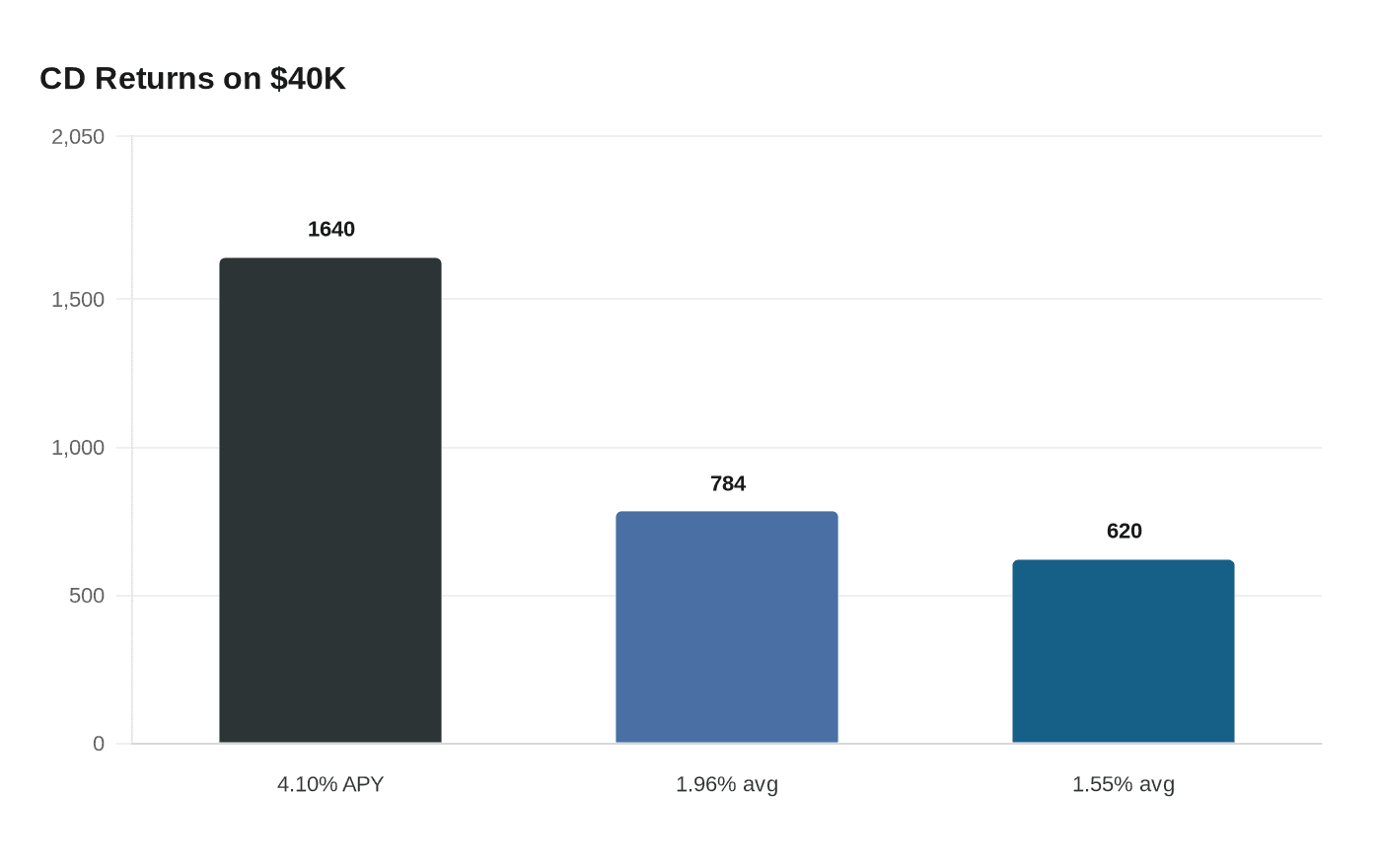

A $40,000 one-year CD at 4.10% APY earns $1,640 before taxes, but inflation cuts the real gain to about $120 and average CDs trail much further.

A $40,000 one-year CD at 4.10% APY would generate $1,640 before taxes, but the household test is less flattering once inflation is counted. With consumer prices up 3.8% over the 12 months ending in April 2026, that deposit leaves only about $120 in added purchasing power before tax, and ordinary-income taxes would shrink the gain further.

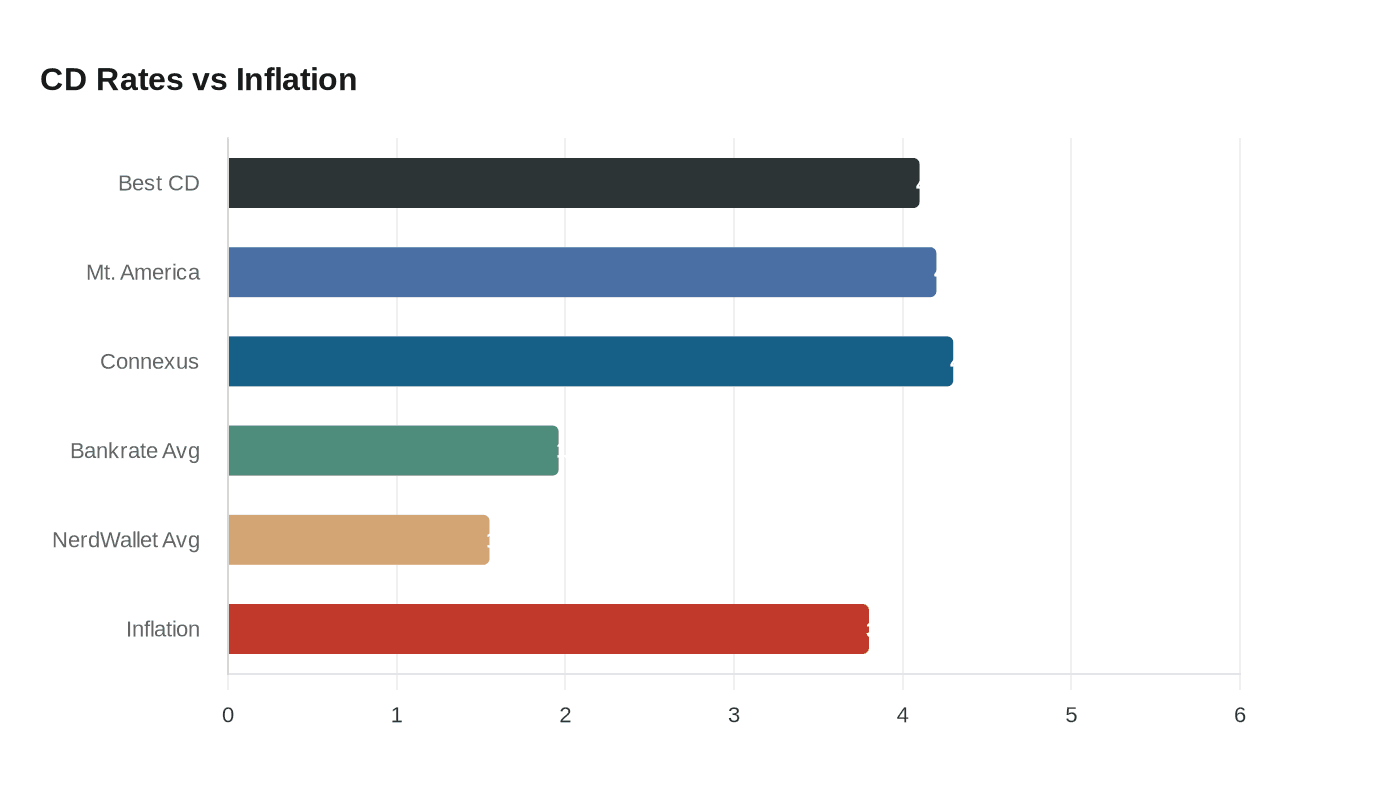

The gap between top-tier offers and the market average remains wide. Bankrate said the best one-year CD it tracked stood at 4.10% APY as of May 22, 2026, with a top short-term rate of 4.20% from Mountain America Credit Union. NerdWallet’s highest tracked CD rate was 4.30% APY from Connexus Credit Union. By contrast, Bankrate put the national average for one-year CDs at 1.96% APY, while NerdWallet said the average was 1.55% in May 2026. On a $40,000 balance, those average rates would produce just $784 and $620 a year before taxes, both well below the inflation rate.

The reason yields have stopped climbing much faster is the Federal Reserve Board’s policy stance. On April 29, 2026, the central bank kept the federal funds target range at 3.5% to 3.75%, leaving banks with limited pressure to bid short-term deposit rates sharply higher. Bankrate said short-term CDs are still the highest-yielding CD category, but even there, the best offers are clustered around 4% APY rather than breaking decisively above it.

NerdWallet’s rate trend points in the same direction. Its midpoint for one-year CD rates at 21 online banks and credit unions fell from 4.00% in January 2025 to 3.70% in April 2026, even though a handful of banks briefly lifted rates in late March and late April. That suggests the current market is still paying up for deposits, but not aggressively enough to outrun inflation by much.

The safety case remains strong. The FDIC insures CDs up to $250,000 per depositor, per insured bank, per ownership category, and all CDs held in the same ownership category at the same bank are combined for coverage. The FDIC also says APY is the best way to compare deposit products because it includes compounding. The main tradeoff is liquidity: Bankrate notes that CDs usually carry early-withdrawal penalties, so money needed before maturity may be better kept in a high-yield savings account, Treasury bill or money market fund.

Know something we missed? Have a correction or additional information?

Submit a Tip