Intel Forecast Tops Estimates as AI Demand Lifts Outlook

Intel lifted second-quarter revenue guidance far above Wall Street’s view, and the stock jumped 19% as investors weighed whether AI demand marks a real turnaround.

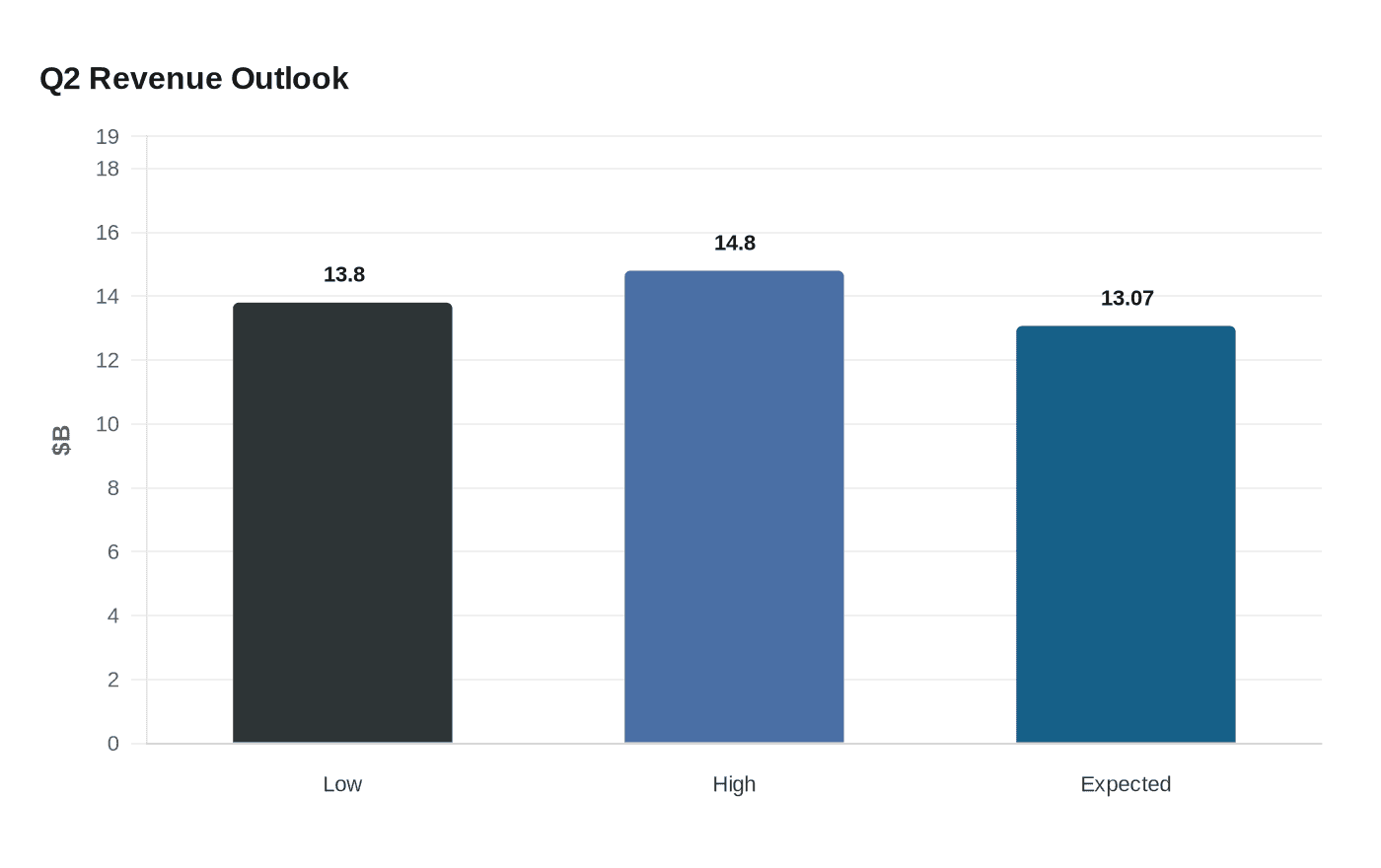

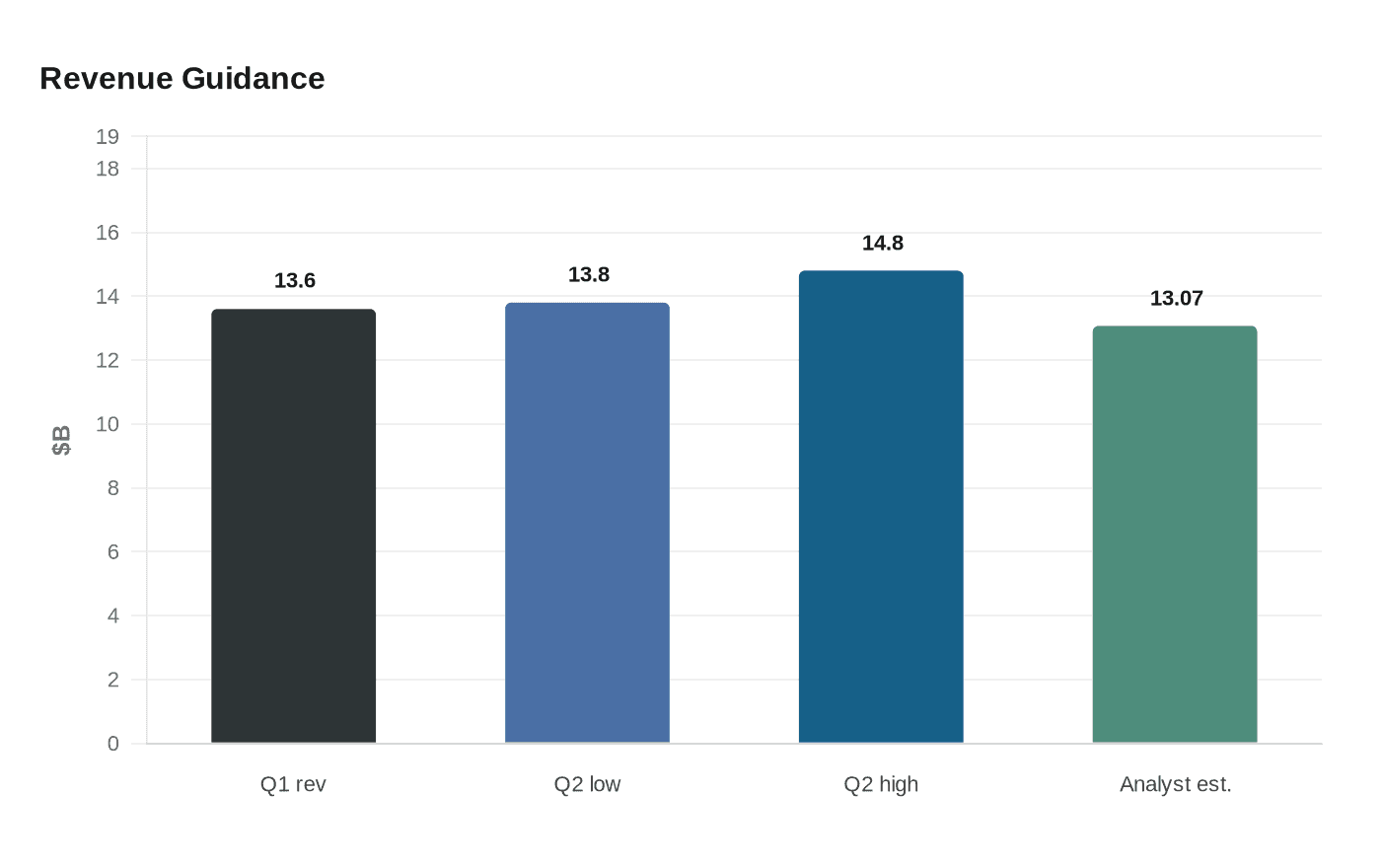

Intel’s latest forecast gave investors a sharper test of its comeback story than any quarterly beat could. The chip maker said second-quarter revenue should reach $13.8 billion to $14.8 billion, well above the $13.07 billion analysts expected, while adjusted earnings per share are projected at 20 cents versus the 9-cent estimate. The response was immediate: Intel shares rose 19% in extended trading, adding about $64 billion in market value and extending an 81% gain so far this year.

The guidance came alongside a first-quarter update that showed Intel’s business still moving in the right direction. Revenue reached $13.6 billion, up 7% from a year earlier, with non-GAAP earnings of 29 cents a share and cash from operations of $1.1 billion. Intel said the quarter was its sixth straight period of revenue above its own expectations, a run that matters because the company has spent years trying to convince the market that its execution can match its ambition.

What made the outlook stand out was the company’s explanation for where demand is coming from. Chief executive Lip-Bu Tan said the next phase of AI is shifting from foundational models to inference and agentic AI, a change that is increasing demand for Intel CPUs, wafer products and advanced packaging. Chief financial officer David Zinsner described the current environment as “unprecedented demand for silicon” and said Intel is focused on maximizing output across its factory network to improve supply through the year. That points to a more durable source of demand than a one-quarter surge in sentiment, but it also leaves Intel with the old problem of conversion: whether the company can turn demand into sustained revenue at scale.

The stakes are high because Intel is still trying to prove that it can regain credibility after years of falling behind rivals in product execution and market share. Tan’s revival plan has included asset sales and layoffs, along with efforts to secure investments and deals involving the U.S. government, SoftBank and Nvidia. Intel also said it raised chip prices to offset higher production costs, a sign that the margin story is still under pressure even as volume improves.

A potential foundry win added another layer to the turnaround narrative. Elon Musk said Tesla plans to use Intel’s next-generation 14A manufacturing process for chips at its Terafab project in Austin, Texas, a deal that could become Intel’s first major external customer for 14A if it develops as described. Intel also disclosed that Altera was deconsolidated effective September 12, 2025, after the sale of 51% of its common stock. For now, the numbers suggest Intel is benefiting from the same data-center and AI spending that has lifted the sector; the harder question is whether this is the start of a real competitive turn, or only a powerful burst of investor optimism.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?