P&G Faces Sixth Straight Gross-Margin Drop as War Costs Rise

War-driven oil and freight costs are set to squeeze P&G for a sixth straight quarter, raising the odds of higher prices on Tide, Pampers and other staples.

A fresh surge in war-driven energy and freight costs is pressing Procter & Gamble at the point where shoppers notice it most, the shelf price of Tide, Pampers and other household staples. When the Cincinnati company reported fiscal third-quarter results, investors were watching for a sixth straight gross-margin decline and for signs that management would defend profit by raising prices, trimming costs, or shrinking packages.

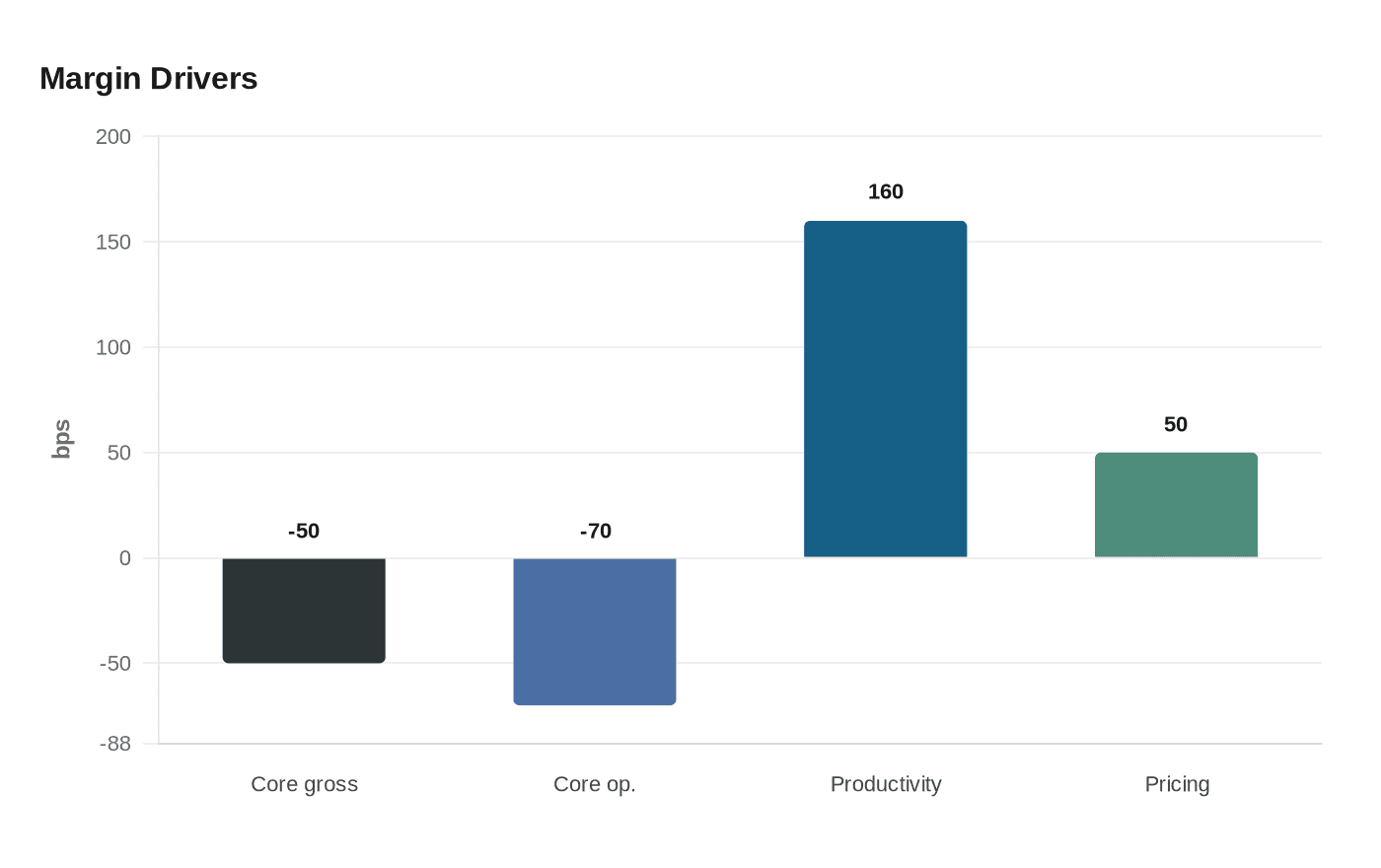

The stakes were clear in P&G’s January second-quarter update, when core gross margin fell 50 basis points from a year earlier and core operating margin slipped 70 basis points. The company still held to fiscal 2026 guidance, calling for core earnings per share to be in line with, or up as much as 4% from, fiscal 2025 core EPS of $6.83, while all-in sales growth was expected to land between 1% and 5%. P&G also posted net sales of $22.2 billion and core EPS of $1.88 for the quarter.

The cost pressure has widened beyond one company. The International Energy Agency said shipping through the Strait of Hormuz plunged amid the Middle East war, describing the disruption as the largest in history. It forecast global oil demand would contract by 80,000 barrels a day in 2026 and fall by 1.5 million barrels a day in the second quarter alone. That matters for P&G because higher oil prices feed directly into freight, plastics and petrochemical derivatives used in packaging, the same inputs that support the company’s everyday consumer brands.

The hit is landing unevenly across the portfolio. Beauty delivered 4% organic sales growth in the second quarter, but baby, feminine and family care fell 4% on an organic basis, showing how weaker demand in lower-growth categories can offset strength elsewhere. Investors were also focused on whether P&G’s sales and earnings were tracking toward the low end of its full-year ranges, especially if households keep trading down or delaying purchases as living costs stay elevated.

That tension echoes the last inflation wave, when consumer giants leaned on pricing and productivity savings to protect margins. P&G said last quarter that gross productivity savings added 160 basis points to margin and pricing added 50 basis points, yet the company still posted a decline. Now the question is whether a new round of input inflation will force another pricing cycle, deeper cost cuts, or more package reductions for consumers already stretched by higher bills.

The market has already begun to price in the strain. P&G shares have fallen nearly 15% since the war in Iran began about two months ago, even as the S&P 500 rose about 4% and recently hit a record high on ceasefire hopes. The S&P 500 consumer-staples index has fallen about 7.4%, underscoring how exposed a mature brand company can be when geopolitics collides with thin margin growth.

New chief executive Shailesh Jejurikar, who took over on January 1, 2026 from Jon Moeller, inherited the problem immediately. Analysts said the next test is not just this quarter, but fiscal 2027, when oil, shipping and currency could decide whether P&G can keep its margins from slipping further.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?