Iran sanctions relief could reopen trade and global payments

Sanctions relief could free Iran’s oil sales first, but banks, SWIFT access and legal barriers would still keep global payments partly frozen.

Iran’s return to world markets would not begin with a dramatic reopening. It would start with a series of narrow, technical moves that relax oil sales, unlock revenue, and test whether banks can again move money through the international system. The fastest gains would likely come in energy, but the hardest work would be in payments, where legal restrictions, compliance fear and political distrust can keep commerce stalled even after a deal is announced.

What would have to change first

The clearest starting point is the set of U.S. sanctions that were fully re-imposed on November 5, 2018, after the United States withdrew from the 2015 Joint Comprehensive Plan of Action. Those measures hit Iran’s energy, shipping and shipbuilding, and financial sectors, which means any meaningful relief has to touch all three if trade is to restart at scale. A partial deal that only eases one layer may create headlines, but it would not by itself restore the machinery of international commerce.

Recent reporting says a draft U.S.-Iran understanding would include an oil sanctions waiver, nuclear limits and asset release, with the preliminary agreement temporarily waiving restrictions on Iran’s oil sales and the money earned from those exports. That is the most important first step because oil remains the quickest source of hard currency for Tehran and the most visible signal to global traders that the policy has changed. If tankers can sell again and proceeds can be retained or repatriated, Iran gets breathing room before broader financial normalization arrives.

Why banking is the real test

Oil can move before full trust returns. Banking cannot. Iranian banks were previously reconnected to the Society for Worldwide Interbank Financial Telecommunication under JCPOA relief, and that access is central to Iran’s ability to transact internationally. Without SWIFT connectivity, even a sanctioned or partially sanctioned economy struggles to invoice buyers, settle trade, move export proceeds, or pay for imports through regular channels.

That makes the legal mechanics as important as the political headline. Treasury and the Office of Foreign Assets Control would need to narrow or suspend restrictions in ways that allow banks, insurers, shipping firms and energy buyers to do business without facing secondary penalties. Even then, many international banks would remain cautious, because large institutions tend to wait for clear, durable guidance before touching Iranian accounts, especially after the experience of the last sanctions snapback.

The result is that reconnection would likely happen in layers. Oil payments might be authorized before wider correspondent banking resumes. Some trade finance could follow, but full access to global payments would still depend on whether the relief is durable, whether compliance teams trust it, and whether the political deal survives pressure in Washington and Tehran.

Which sectors would move first

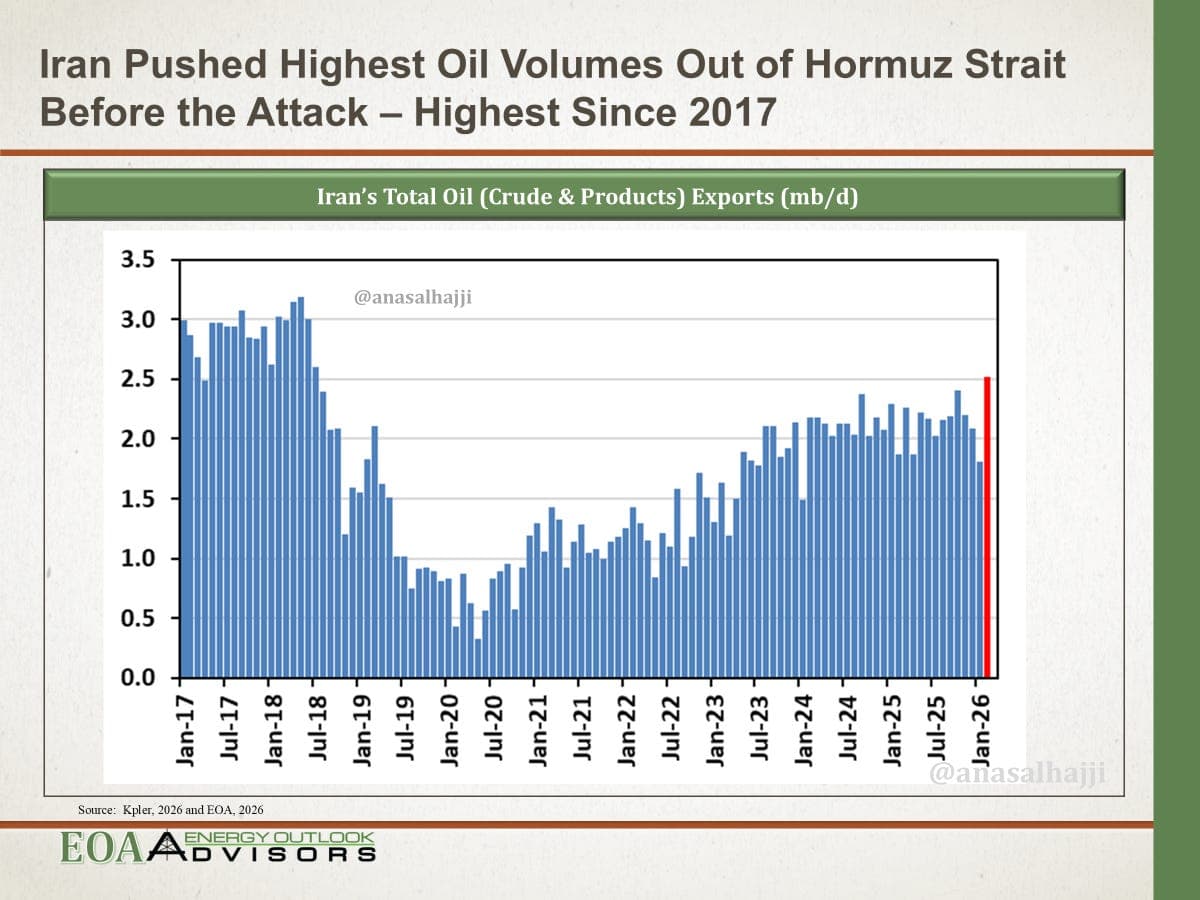

Energy is the obvious first mover because it is the sector most directly named in the 2018 sanctions and the one most immediately tied to revenue. If restrictions on oil sales are waived, Iranian exports can begin to flow again, at least in limited form, and that could quickly affect market expectations. Even the prospect of more barrels can matter for prices, because traders respond not only to actual supply but to the probability that supply will increase.

Shipping would follow close behind, but it faces its own barriers. A tanker that carries sanctioned crude still needs insurance, port access, financing and a bank willing to clear payment. Shipbuilding and logistics also remain constrained, so the reopening of one channel does not automatically restore the rest of the supply chain. That is why any sanctions relief package must be read as a sequence, not a switch.

Financial access is the third and most difficult layer. The sanctions restored in 2018 targeted Iran’s financial sector directly, and the damage from that isolation lingers even after legal restrictions begin to ease. Banks can technically be cleared to reconnect, but the market response will depend on whether foreign institutions believe they can process payments without later punishment.

What the economic data says

The economic cost of isolation is already visible in the numbers. The International Monetary Fund said Iran’s real GDP growth rebounded to 4.3 percent in 2017/18 after the nuclear deal, showing how quickly sanctions relief can lift activity when trade and finance reopen. The Center for a New American Security then said GDP contracted 5.4 percent in 2018 and 7.6 percent in 2019 after sanctions were restored, underscoring how sharply renewed pressure can reverse that gain.

That pattern matters because it explains why Tehran treats sanctions relief as more than a diplomatic gesture. It is the difference between selling crude into a constrained market and rebuilding a more normal export economy. It is also the difference between a banking system that can handle international settlement and one forced to operate through workarounds, delays and intermediaries.

For global markets, the stakes are just as concrete. A credible oil waiver can add supply expectations to an already sensitive energy market, while a weak or reversible deal can create volatility as traders price in the risk of another snapback. Either way, the market is not waiting for rhetoric. It is watching whether barrels, wires and bank messages actually start moving.

Why politics still limits normalization

Even a deal would not erase the political barriers around Iran. Britain, France, Germany, Italy and Japan welcomed the agreement, and some European governments signaled they were prepared to lift sanctions if Iran curbs its nuclear program. That kind of support matters because European policy can help create the commercial space needed for trade, insurance and banking to resume more broadly.

But political welcome is not the same as full reintegration. U.S. leverage still sits at the center of the system because American sanctions shape the risk calculus for banks and multinational firms far beyond U.S. borders. A temporary waiver can open channels, yet the deeper question is whether firms believe the relief will last long enough to justify re-entering a market that has been shut, reopened and shut again before.

That is why the practical test of any Iran deal is not the announcement itself. It is whether Treasury guidance, OFAC licensing, bank compliance, and foreign counterparties line up fast enough to turn legal relief into real commerce. Until then, Iran may gain room to sell oil sooner than it regains full access to the global payments system, and that gap will define both the economics and the politics of reconnection.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip