Judge finds IRS shared addresses with ICE in roughly 42,695 improper disclosures

A federal judge ruled the IRS violated Section 6103 by disclosing last-known taxpayer addresses to ICE about 42,695 times, raising privacy and safety concerns for immigrant communities.

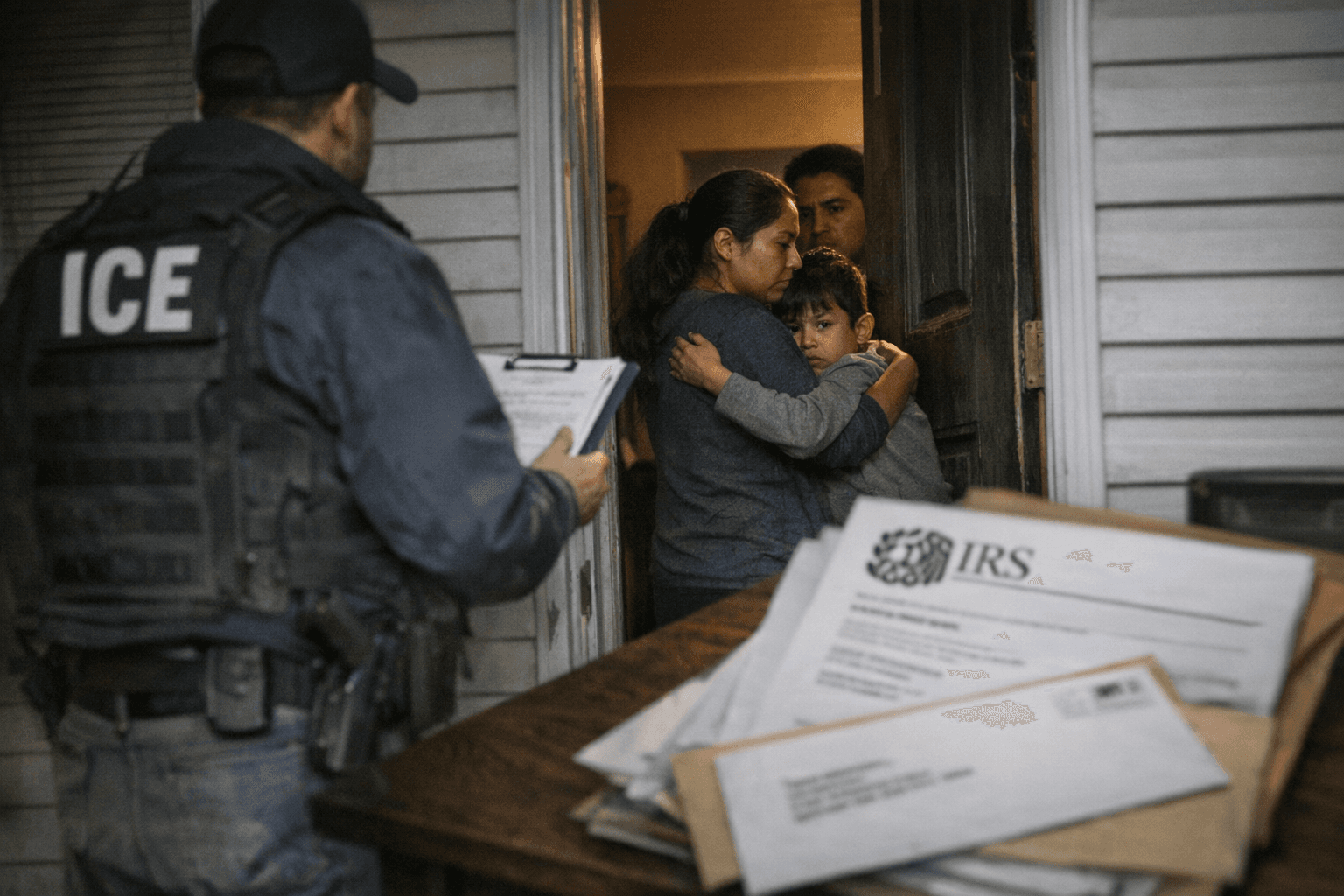

A federal judge found the Internal Revenue Service improperly disclosed last-known taxpayer addresses to Immigration and Customs Enforcement about 42,695 times, ruling on Feb. 26, 2026 that those disclosures violated the strict confidentiality protections of Section 6103 of the Internal Revenue Code. The decision marks a rare judicial rebuke of interagency data sharing and puts the spotlight on how tax information has been used in immigration enforcement.

Section 6103 limits how the IRS may share taxpayer information and generally bars disclosure except in narrowly specified circumstances. The court concluded that the agency’s transfers of address data to ICE exceeded those limits, creating a statutory violation with immediate privacy implications for thousands of people. The ruling does not rest on speculation; it is grounded in a quantified finding of roughly 42,695 instances in which last-known addresses were provided to immigration authorities.

Legal consequences could be significant. Section 6103 provides avenues for civil redress and includes criminal penalties for willful unauthorized disclosures. The judgment is likely to trigger follow-on litigation seeking damages, administrative investigations within Treasury and the IRS, and oversight inquiries in Congress. It also raises questions about whether internal safeguards and audit trails were adequate when taxpayer records were accessed and transmitted to another federal agency.

Beyond legal technicalities, the court’s finding reverberates through immigrant communities and the wider civic compact. Taxpayers who are noncitizens often rely on confidence in confidential handling of returns when they comply with tax obligations. Advocacy groups and community leaders say such revelations can chill participation in the tax system and deter interaction with government programs that require personal data. The disclosures also carry immediate safety concerns: addresses can reveal household locations, put relatives at risk of enforcement encounters, and complicate asylum or relief claims where confidentiality is essential.

The ruling intersects with broader debates over cross-agency data sharing in an era of increasing reliance on digital records. Governments around the world balance law enforcement objectives against privacy and human rights obligations, and this decision underscores how U.S. domestic law constrains those choices. Internationally, the case may attract attention from governments whose nationals file U.S. returns, as well as from human rights observers concerned about the extraterritorial impacts of enforcement tactics.

Practical fallout will hinge on remedies ordered by the court and the response from the IRS and the Department of Homeland Security. Potential reforms could include tighter access controls, mandatory logging of requests for taxpayer data, and new statutory or regulatory limits on transferring address information for immigration purposes. Congressional committees that oversee tax administration and homeland security are also likely to press for briefings and to consider legislative fixes.

For taxpayers, the decision is a reminder that legal protections for confidential information can be enforceable and that disclosures once thought routine may attract scrutiny. For policymakers, the ruling frames a test of how agencies can pursue enforcement priorities without undermining legal safeguards, public trust, and the safety of vulnerable populations.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?