June mortgage borrowers should avoid these common interest rate mistakes

A half-point wait can cost you hundreds a month, and June borrowers who bet on a quick refinance may pay for it all summer.

Why June is a high-stakes month for rate decisions

Mortgage pricing is still pinned in the mid-6% range, and that is exactly where small timing errors start to cost real money. Freddie Mac put the 30-year fixed rate at 6.53% for the week ending May 28, while a June 3 daily read showed an average 30-year purchase rate of 6.586%. Freddie Mac also said pending home sales have risen for three straight months, a sign that demand is waiting on the sidelines and can rush back in if rates ease.

The backdrop is still volatile enough that a few tenths of a point can matter. Analysts cited by U.S. News expect the 30-year fixed to bounce between the low and mid-6% range through 2026 and 2027, with Fannie Mae and the Mortgage Bankers Association both putting 2026 around 6.2%. That means the market is not pricing in a dramatic plunge, and it also explains why June is a month to protect your budget rather than speculate on a clean drop.

Do not wait for a magical Fed cut

One of the most expensive mistakes is assuming a Federal Reserve meeting will hand you a lower mortgage rate on schedule. Mortgage pricing is still being pushed around by inflation worries, tax policy uncertainty, and geopolitical shocks, so the path can move higher even when borrowers are hoping for relief. If a lock now sits at 6.53% and the market drifts to 7.03% instead, the monthly principal-and-interest payment on a $400,000 loan rises from about $2,536 to about $2,669, or roughly $133 more each month. Hold that higher rate for the full 30 years, and the extra outlay is about $47,918.

That is why locking becomes valuable when your closing is close and your payment already fits your budget. The bigger risk in June is not missing a fantasy rate that may never show up; it is letting a small upward move turn into a payment shock just as the summer buying season builds.

Do not float without a plan

Floating can make sense only if you have time and you can tolerate the downside. In a simple example, paying $4,000 to buy the rate down from 6.53% to 6.28% saves about $65.49 a month on a $400,000 loan, so you need a little more than 61 months to earn that money back. If you might sell, refinance, or move in a few years, that math can turn a rate buy-down into dead money.

The same logic works in reverse. If you float and the rate rises just a quarter of a point, the savings you were chasing can disappear fast, and if the move is half a point the monthly damage is much larger. June borrowers should think of floating as a deliberate bet with cash reserves behind it, not as a passive way to hope for a better mood in the bond market.

Do not overbuy on refinance hope

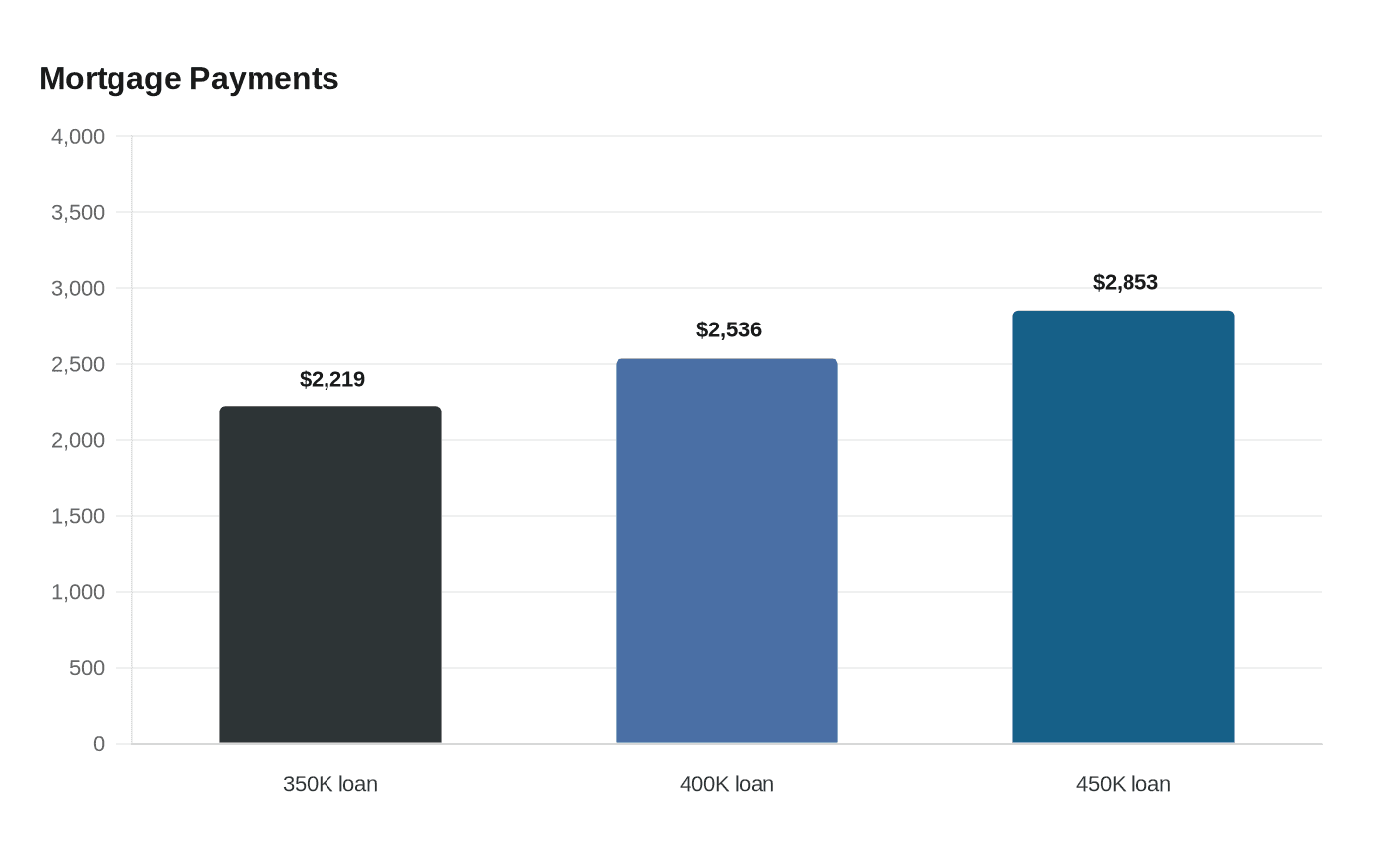

The most dangerous affordability mistake is stretching for a bigger house because you assume a refinance will save you later. Forecasts from Fannie Mae and the Mortgage Bankers Association suggest rates will stay around 6.1% to 6.3% in 2026, which means a rescue refinance is possible but far from guaranteed. On today’s numbers, a $450,000 loan at 6.53% carries a monthly payment of about $2,853, versus about $2,219 on a $350,000 loan. That extra $100,000 of borrowing adds about $634 every month, or roughly $228,255 in total payments over 30 years.

Even if rates later fall to 6.03%, the larger loan still costs about $2,707 a month. That is why “we’ll refinance later” is not a real affordability strategy. It can leave you with a payment that stays hundreds of dollars higher even after a rate drop, while also exposing you to the closing costs of the refinance itself.

The June playbook

The safest approach this month is simple: lock when your payment works and your closing is near, float only when you can survive a worse rate, and treat any points or buy-downs as an investment that has to earn its keep. If you can afford a shorter term, the 15-year fixed rate averaged 5.87% for the week ending May 28, but that option came with a much higher monthly payment of about $3,347 on a $400,000 loan, compared with about $2,536 on a 30-year loan at 6.53%.

June is a month for discipline, not wishful thinking. With rates still in the mid-6s, demand waiting in the wings, and forecasts pointing to only modest relief, the borrowers who win are the ones who protect cash flow and avoid turning a timing gamble into a long-term bill.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip