CD interest rates stay high, but are they enough for $1,000 deposits?

A $1,000 CD still only adds a few dollars a month after tax and inflation, so the real test is whether locking up emergency cash is worth so little extra yield.

The $1,000 math

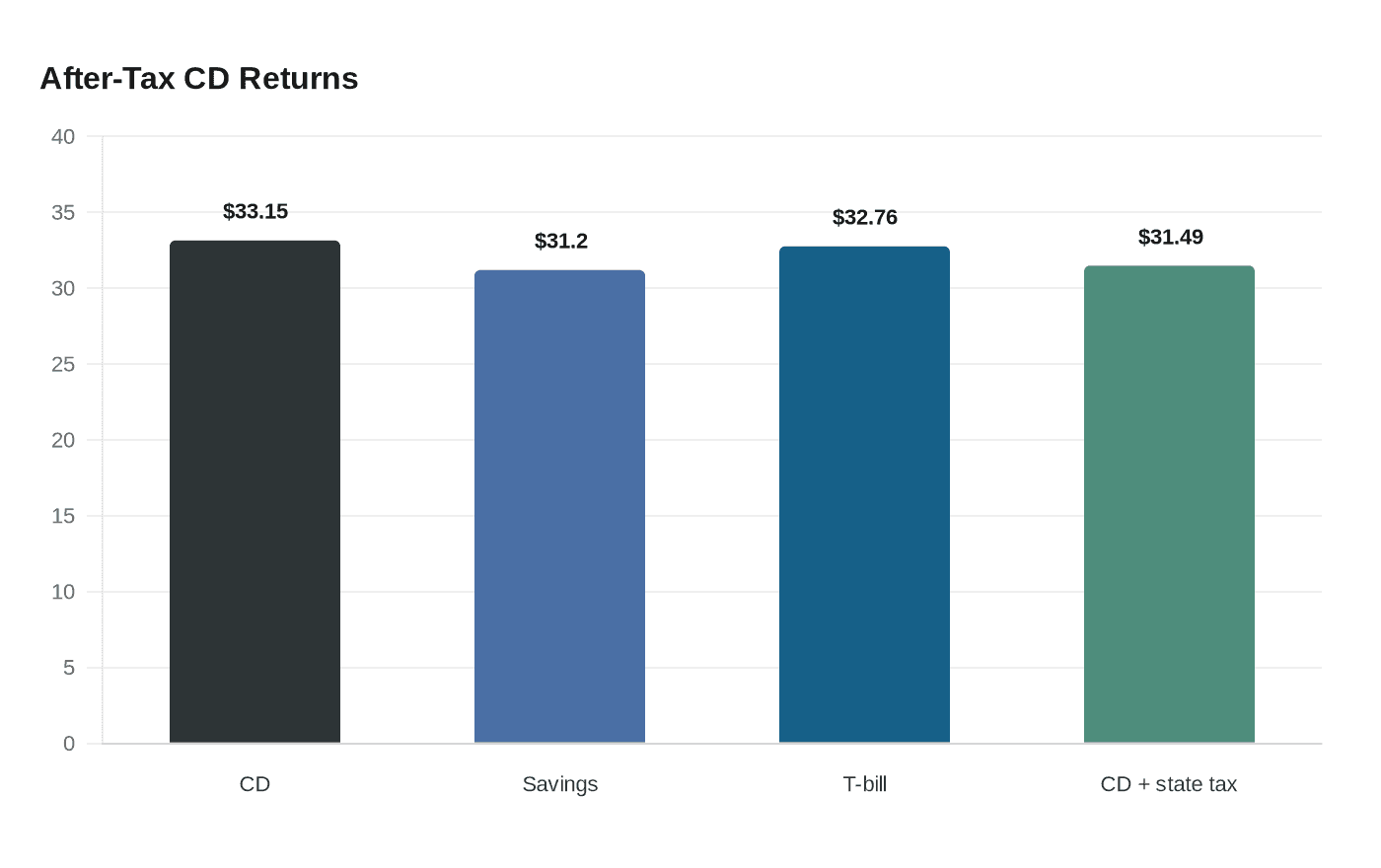

A $1,000 CD can still look attractive on paper, but the dollars are small once you strip out tax and inflation. At a 4.25% APY, that deposit earns $42.50 in a year before tax, $33.15 after a 22% federal tax rate, and about $7.95 in real after-tax purchasing power if inflation runs at 2.5%.

That is the key consumer math: a good rate does not turn a small balance into meaningful income. It turns it into a modest offset against inflation, which is useful, but not enough to make liquidity irrelevant for money that might be needed fast. The monthly after-tax gain works out to about $2.76, so even a year of patience only buys a few extra dollars.

How CDs stack up against savings and Treasury bills

A high-yield savings account at 4.00% APY produces $40 before tax and $31.20 after the same federal tax assumption. A Treasury bill at a 4.20% annualized yield produces $42 before tax and $32.76 after federal tax. On a $1,000 balance, the CD’s edge over the savings account is just $2.50 before tax, or $1.95 after tax, while its edge over the T-bill is only 50 cents before tax and 39 cents after tax.

That spread is tiny enough that taxes can flip the comparison. If you also pay a 5% state tax, the taxable CD’s after-tax interest drops to about $31.49, while the Treasury bill still keeps $32.76 because Treasury interest is exempt from state and local income tax. For savers in taxable states, that exemption can matter more than the headline APY gap.

Why the lockup matters more when the balance is small

The hard part of a CD decision is that the reward for locking up $1,000 is so limited. A standard three-month early-withdrawal penalty on that balance would cost about $10.63 before tax, or $8.29 after tax, which is enough to wipe out months of interest. That is why a small emergency fund is punished more by penalties than a larger savings pool would be.

The comparison also shows how little room there is between products. The CD’s monthly after-tax interest is about $2.76, versus $2.60 for the savings account and $2.73 for the Treasury bill. Those are real differences, but they are small differences, and small differences matter less than having cash available the day an expense arrives.

When a CD makes sense, and when it does not

A CD works best when the money is already spoken for and the timing is known. If you are saving for a tuition bill, a property tax payment, or another expense with a clear date, the lockup can be a feature rather than a flaw, especially if the CD rate is higher than your savings account and you are confident you will not need the money early.

For a true emergency fund, the logic changes. Cash that needs to cover a job loss, a car repair, or an unexpected medical bill earns its keep by being ready, not by squeezing out an extra dollar or two a month. In that case, a high-yield savings account usually wins on convenience, while Treasury bills offer a middle ground for people who can tolerate short maturities and want a better after-tax result than a taxable deposit account.

The bottom line

For a $1,000 emergency reserve, the real question is not whether CD rates are high. It is whether locking up cash for a handful of extra dollars a year is worth losing immediate access to it. At today’s rate math, the answer is usually no unless the money can stay untouched until maturity or the state-tax advantage of Treasury bills changes the calculus in your favor.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip