IRS rules force hefty withdrawals from a $750,000 retirement nest egg

A $750,000 account can generate a roughly $28,300 RMD at age 73, and the tax bill can jump fast if that forced income lands in a higher bracket.

How the IRS turns a $750,000 nest egg into a mandatory withdrawal

The IRS does not let tax-deferred retirement money sit untouched forever. For traditional IRAs, SEP IRAs, SIMPLE IRAs, 401(k)s and most other defined-contribution plans, the required minimum distribution is the prior year-end account balance divided by an IRS life-expectancy factor from the Uniform Lifetime Table. Roth IRAs and designated Roth accounts are different: the owner is not required to take lifetime withdrawals, although beneficiaries can face RMD rules later.

That formula matters because the withdrawal amount is not based on what you need to spend. It is based on the balance that sat in the account on December 31 of the prior year, and the clock starts when you reach age 73. For IRAs, the first RMD is generally due by April 1 of the year after you turn 73, and every later RMD is due by December 31. For many workplace plans, the rules are similar, although you can often delay until retirement unless you are a 5% owner.

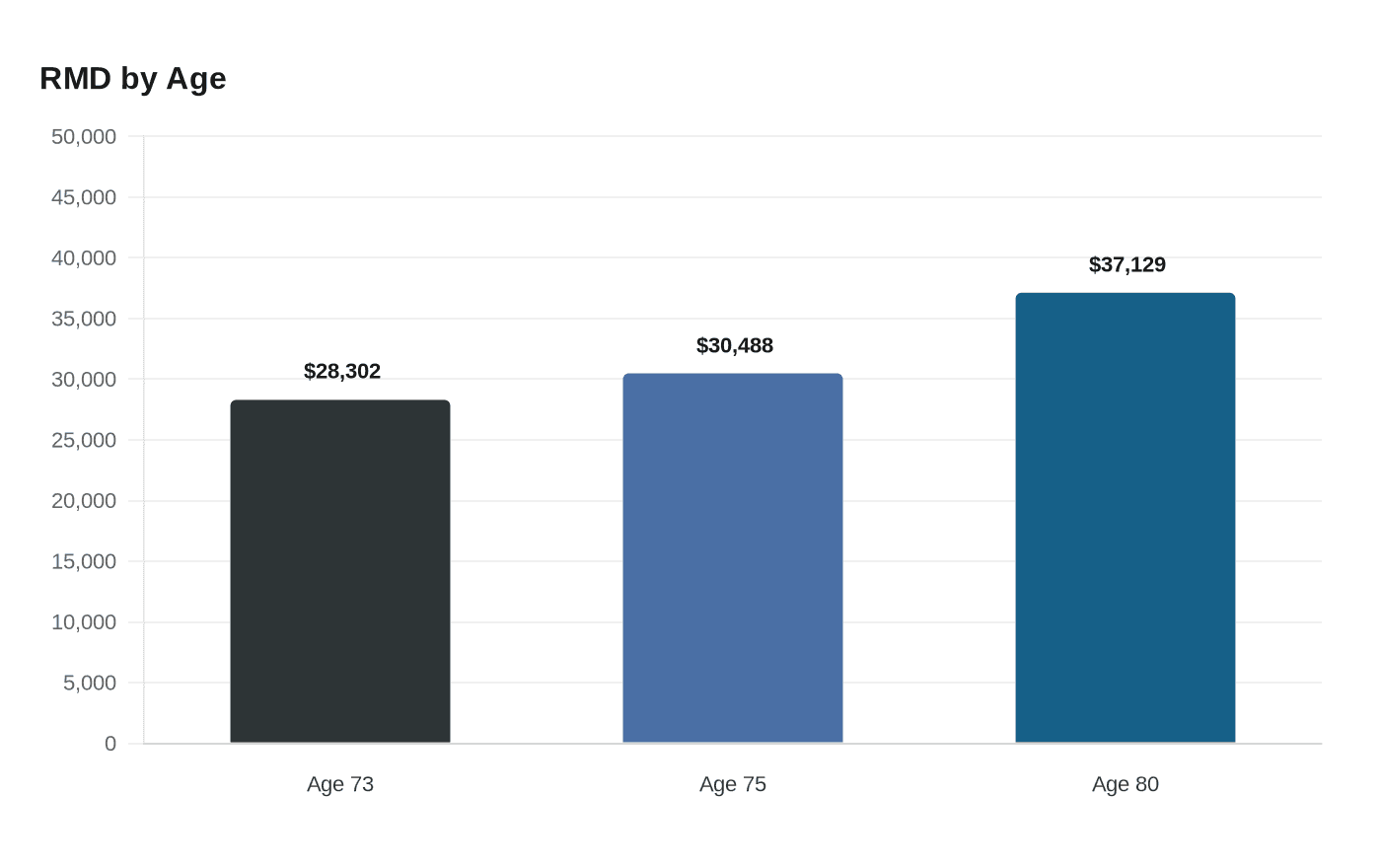

What a $750,000 account produces at different ages

On a $750,000 traditional IRA or similar pretax account, the required withdrawal grows as you get older because the divisor shrinks. At age 73, dividing $750,000 by 26.5 produces an RMD of about $28,302. At age 75, dividing by 24.6 produces about $30,488. By age 80, dividing by 20.2 pushes the RMD to about $37,129.

That rising number is the core planning problem for retirees. Even if you do not need the cash to pay bills, the IRS still treats the withdrawal as income in most cases. That means the RMD can be large enough to move a retiree into a higher bracket, especially when Social Security, pension income, dividends or capital gains are already part of the tax return.

What the tax bill can look like

The tax hit depends on your marginal federal bracket, not on the size of the account alone. If a 73-year-old pulls a roughly $28,302 RMD from a $750,000 account and lands in a 22% bracket, the federal income tax tied to that distribution is about $6,226. At 24%, it is about $6,792. If the same retiree were in a 12% bracket, the tax would still be about $3,396.

The bill rises with age because the required withdrawal rises too. At age 75, a $750,000 account generates an RMD of about $30,488, which would create roughly $6,707 of federal tax at a 22% bracket. At age 80, the roughly $37,129 withdrawal would create about $8,911 of federal tax at a 24% bracket. These are federal income taxes only, before any state tax.

Why retirees get squeezed even when they do not need the money

The RMD is not optional, and it is not sheltered just because the saver already has enough income. The IRS says withdrawals are included in taxable income except for any amount that was already taxed, known as basis, or for qualified tax-free Roth distributions. That is why mandatory withdrawals can create an uncomfortable tradeoff: you may be forced to realize income you would rather defer, and that extra income can cascade into higher taxes.

There is also a timing trap in the first RMD year. If you delay the first withdrawal until April 1 of the following year, you still owe the next year’s RMD by December 31 of that same year. That can create two taxable withdrawals in one calendar year, a mistake that can make an otherwise manageable tax bill much larger.

What happens if you miss the deadline

Missing an RMD can trigger an excise tax under Internal Revenue Code section 4974. The IRS says plan sponsors can use its correction programs to fix RMD failures, and the Voluntary Correction Program can be used to request a waiver of the excise tax in some cases. Self-correction does not waive the participant’s excise tax.

The penalty is steep enough to hurt twice. On the age-73 example, a missed $28,302 RMD would produce a 25% penalty of about $7,075, and a 10% corrected penalty of about $2,830. The cleanest defense is simple discipline: know the prior-year balance, apply the correct divisor, and take the withdrawal on time.

The practical planning takeaway

For retirees with a $750,000 pretax nest egg, the real issue is not whether the account is large enough. It is whether the mandatory withdrawal fits neatly inside the rest of the tax picture. A distribution of roughly $28,300 at age 73, rising to more than $37,000 by age 80, can be manageable in isolation and still push taxable income higher than expected once it is added to other retirement income.

That is why RMD planning is less about spending the money and more about controlling the tax timing. The IRS formula is mechanical, but the consequences are anything but. For many seniors, the challenge is not just meeting the deadline, it is managing the bracket pressure that comes with being forced to take the money out.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip