Local Governments Finance Housing They Aim to Keep Affordable Forever

Local governments are starting to finance housing like long-term owners, not one-time subsidizers. The hard test is whether these funds can preserve affordability for decades and scale beyond a few strong counties and cities.

A new role for city hall

Local governments are increasingly trying to do more than help housing get built. They are putting public money directly into projects, taking ownership stakes, and setting up revolving funds designed to keep units affordable long after the first subsidy is spent. That is a quiet but consequential shift in housing policy: instead of treating affordability as a temporary intervention, officials are acting more like long-term investors and stewards.

The appeal is straightforward. If a county or city can help finance a building, keep a share of the units permanently affordable, and recycle repayments into the next project, the public dollar can work far longer than a one-time grant. The unresolved question is whether these models can preserve affordability over decades, not just during the first financing cycle, and whether they can scale beyond a handful of well-resourced jurisdictions.

Montgomery County’s revolving fund model

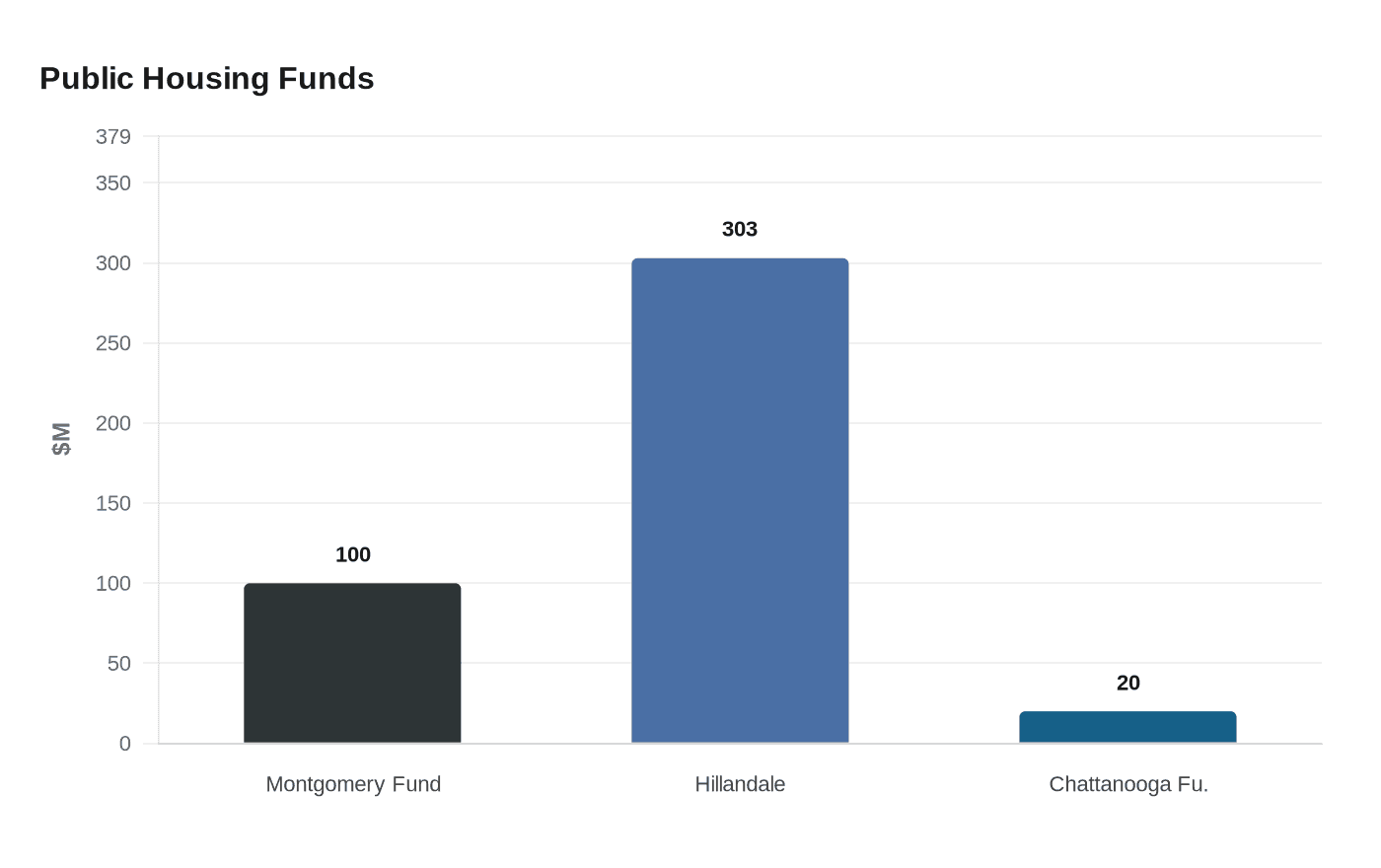

Montgomery County, Maryland, has become one of the clearest examples of this strategy. In 2021 and 2022, county officials created a $100 million Housing Production Fund, structured as a revolving fund rather than a one-time subsidy pool. The county says the fund can support construction of 6,000 new residential units over 20 years, including 1,800 units, or 30%, that would remain permanently affordable.

That design reflects a broader change in how the county thinks about housing finance. The Montgomery County Housing Opportunities Commission has described the effort as a move away from relying only on finite federal housing dollars. County housing officials also say the public sector has been using flexible financing for multifamily development since 1989, which gives the model a longer local history than the current fund itself suggests.

The scale matters because Montgomery County is not only making loans, it is helping underwrite projects that remain partly in public hands. In 2024, the county closed on more than $303 million in financing for Hillandale Gateway, a 463-unit mixed-income, mixed-use community in Silver Spring that is majority owned by the county. That transaction shows how the county is using public finance not just to stimulate construction, but to keep an ownership role in the asset itself.

Chattanooga’s bet on public investment

Chattanooga, Tennessee, has now joined that same policy current. On December 5, 2024, the city announced a $20 million Housing Production Fund and launched Invest Chattanooga, a public enterprise and Housing Authority subsidiary built to finance housing with both market-rate and dedicated affordable units.

The structure is notable because it treats housing more like infrastructure than a short-term grant program. Invest Chattanooga can provide low-cost construction loans covering up to 25% of project costs, a share large enough to improve project feasibility without paying for the entire building. That makes the city a financing partner, not simply a subsidy provider, and it gives officials more leverage over the eventual affordability mix.

The Chattanooga model also underscores the political appeal of mixed-income development. By funding projects that include both market-rate and affordable homes, the city can stretch public dollars further while still locking in a dedicated affordability component. The challenge, as in Montgomery County, is whether the public side can hold that line over time as properties age, financing changes, and ownership shifts.

Why the timing matters now

This policy shift is happening against a still-severe affordability crunch. The Urban Institute reported in August 2024 that more than 40 million Americans were struggling to afford housing costs. It also found that 60% of Republicans in a recent poll were more likely to vote for a candidate who supports permanently affordable housing, which suggests that the politics of long-term affordability may be broader than traditional housing coalitions.

Federal rescue money has also helped local governments test these models at scale. In October 2023, the U.S. Department of the Treasury said nearly $63 billion across ARPA housing programs had been dedicated to housing projects. Brookings Metro reported in June 2024 that large U.S. cities and counties had committed $6.7 billion of State and Local Fiscal Recovery Funds to housing projects, about 11% of the funds appropriated to date. Roughly two-thirds of those local investments were focused on homelessness services and affordable housing development.

That federal flow of money matters because it has given local governments room to experiment with direct investment, lending, and ownership. But rescue funds are temporary by design. The more important question is what remains after those dollars are gone.

Community land trusts offer a parallel answer

One of the clearest long-run affordability tools is the community land trust. The basic idea is simple: separate land ownership from housing ownership, then restrict resale value so that homes stay affordable for future buyers rather than being absorbed into speculative markets. That structure can keep public investment in place far longer than a one-time subsidy tied to a single sale.

Urban policy research points to cities such as Irvine, California, where public land and low-interest loans have helped launch community land trusts. That approach shows another version of the same governing logic seen in Montgomery County and Chattanooga: public institutions can shape the rules of ownership, not just finance construction.

Community land trusts also make the central policy tradeoff visible. They can preserve affordability permanently, but they require legal and administrative discipline, as well as land or financing that municipalities are willing to hold for the long haul. That makes them powerful, but not easily replicated everywhere.

The real test for local government housing finance

The emerging debate is no longer whether local governments should help fund housing. They already are, through revolving funds, public enterprises, land trusts, and direct ownership stakes. The harder question is whether they can protect affordability for decades, keep those units out of speculative cycles, and recycle public capital into the next project without losing control.

Montgomery County’s $100 million fund, Chattanooga’s $20 million initiative, and the federal rescue dollars that helped localities experiment all point in the same direction. Governments are starting to behave less like temporary subsidizers and more like long-term investors. The durability of that shift will determine whether these programs become a durable housing model or remain the province of a few unusually capable places.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?