Low-Cost Extrusion Drives Polymer 3D Printing Market to $6.1B by 2034

low-cost extrusion systems push polymer 3D printing toward a $6.1B market by 2034, expanding commercial and defense uses and changing material and vendor dynamics.

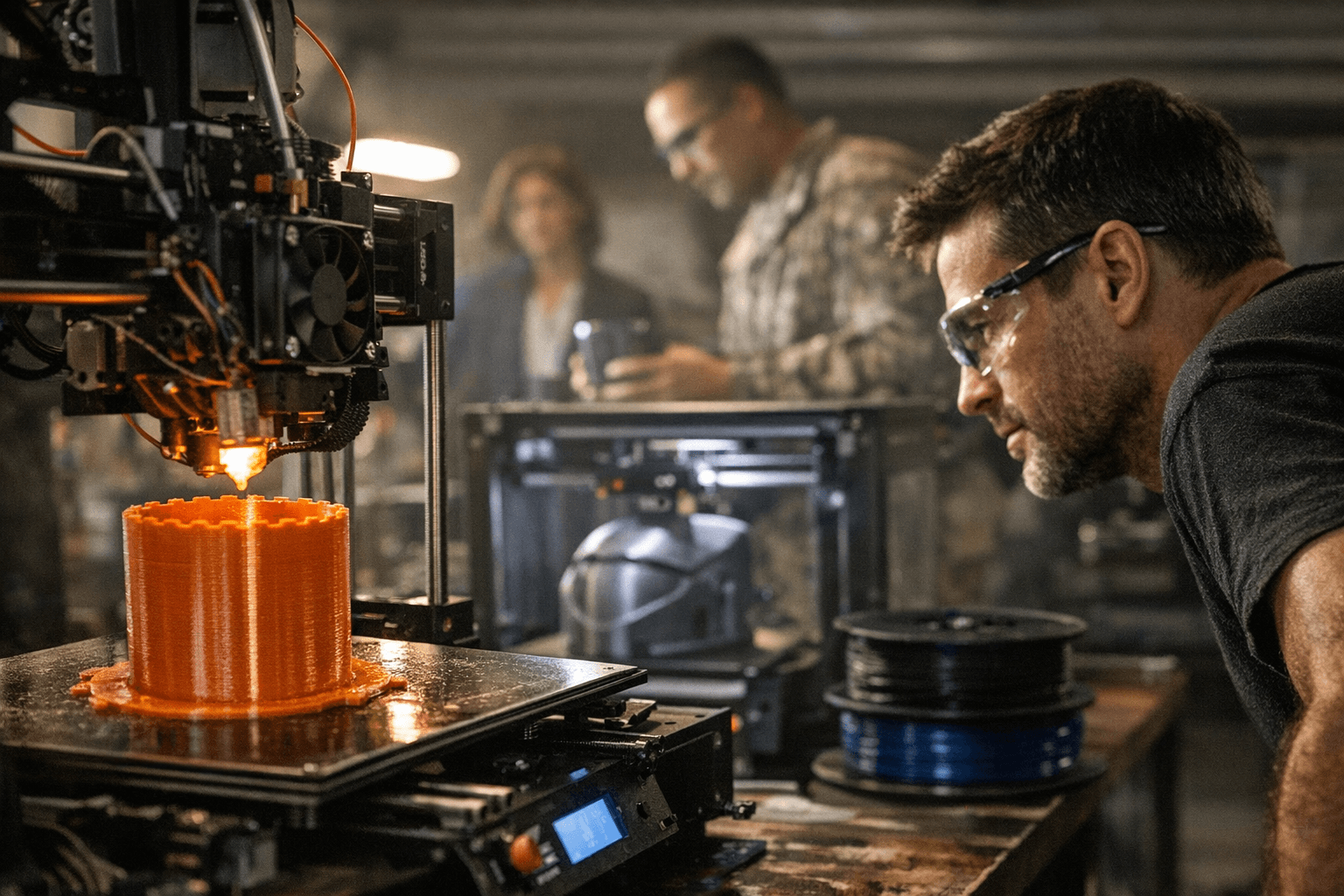

A new market forecast released January 19 projects the polymer extrusion segment of 3D printing will grow from about $2.2 billion in 2025 to $6.1 billion by 2034, driven largely by the explosive expansion of low-cost extrusion systems. What began as hobbyist desktop tooling is moving into small-scale manufacturing, industrial prototyping, and even defense applications, altering purchasing choices for makers, small shops, and service bureaus.

The analysis breaks the market into material, application, geography, and vendor segments, and highlights a striking rise in materials innovation. Materials grew at an estimated compound annual growth rate of roughly 23 percent between 2020 and 2025, and that momentum is expected to continue as filament and pellet chemistries diversify. That matters at the bench: new composite filaments, high-temperature polymers, and affordable engineering-grade materials mean hobbyists and micro-factories can produce stronger, lighter, and more functional parts without stepping up to very expensive platforms.

Extrusion technologies are finding traction beyond model parts. The forecast shows growing use in drones, solid rocket motors, and other defense and industrial components where speed, weight reduction, and part consolidation matter. These applications demand process control, traceable materials, and qualification workflows—areas where established professional suppliers still hold advantages. At the same time, low-cost upstarts are compressing price points and enabling rapid adoption by print farms, prototyping shops, and classroom programs.

For the community, the takeaway is practical and immediate. Expect more accessible professional tooling and a wider palette of validated materials, which can lower entry costs for commercial projects and scale-out production. Verify material data sheets and run in-house validation when parts move from hobby-grade prints to functional components. Keep slicer profiles, nozzle choices, and cooling strategies in mind as new materials alter processing windows. Watch for vendor strategies that mix aggressive hardware pricing with proprietary consumables—cost savings up front may come with material lock-in later.

Competitive dynamics will shape supply chains and service models. Established vendors will leverage certifications and support for regulated sectors, while nimble newcomers will push innovation in price, software, and modular hardware. Regional adoption will vary, with industrial clusters likely to adopt extrusion for end-use parts faster than hobby-focused markets.

The forecast includes detailed vendor-level breakdowns and full datasets for teams modeling investments or scaling operations. For readers, that means more options and faster iteration cycles, but also a need for disciplined testing and supplier scrutiny as extrusion moves from tinkering to true manufacturing.

Sources:

Know something we missed? Have a correction or additional information?

Submit a Tip