March Jobs Report Surpasses Forecasts With 178,000 Positions Added

March payrolls tripled economists' forecasts at 178,000, but soft wage growth and a slipping participation rate signal a fragile rebound rather than a broad-based surge.

The U.S. economy added 178,000 jobs in March, a figure that roughly tripled economists' expectations and reversed what had been the worst month for employment in years. But peeling back the headline number reveals a recovery concentrated in a narrow slice of the economy, with warning signs accumulating beneath the surface that are already shaping the Federal Reserve's calculus on interest rates.

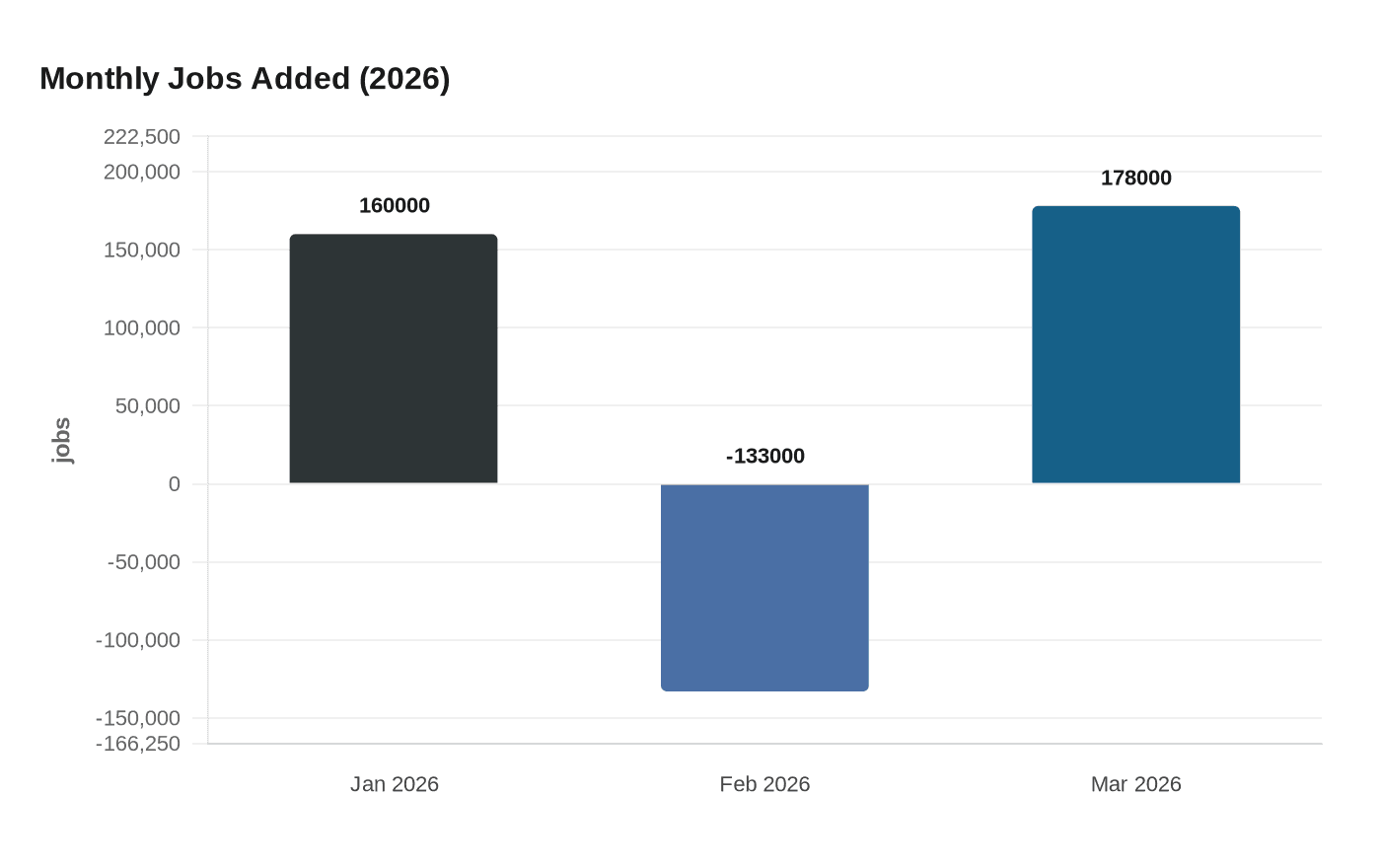

The Bureau of Labor Statistics reported Friday that the March gain far outpaced the Dow Jones consensus forecast of 59,000, erasing February's revised loss of 133,000 positions, which had been dragged down by a healthcare workers' strike. Healthcare led all sectors again in March with 76,000 new positions, a figure inflated in part by 35,000 physicians' office workers returning from that strike. Construction and transportation and warehousing also posted gains. Federal government employment continued to shrink, with roughly 8,000 positions eliminated, extending a contraction that has pushed the unemployment rate for government workers from 1.9 percent a year ago to 2.5 percent today.

Revisions to prior months offered little net comfort. January's count was revised upward by 34,000 to 160,000, while February's was revised down by 41,000, leaving the two-month net nearly unchanged. The BLS also noted that over the prior 12 months, payroll employment had "changed little on net."

Three key indicators beneath the headline tell a more cautious story. Average hourly earnings rose just 0.2 percent in March and 3.5 percent over the past year, the slowest annual wage growth since May 2021, missing economist forecasts of 0.3 percent monthly and 3.7 percent annually. The average workweek edged down by 0.1 hour to 34.2 hours. And the labor force participation rate slipped to 61.9 percent as more adults stepped back from the workforce than stepped in. Long-term unemployment, meanwhile, climbed 322,000 over the year to 1.8 million people, representing 25.4 percent of all unemployed Americans.

Laura Ullrich, director of economic research at the Indeed Hiring Lab, captured the structural tension: "The broader story of 2026 so far remains one of recalibration rather than acceleration." Ullrich cautioned that healthcare and social assistance continue to do the economy's "heavy lifting" while long-term unemployment rises as "sidelined workers struggle to transition into the few sectors that are growing."

For the Fed, the report settles the question of what happens next at the policy table, at least for now. Officials held the benchmark rate steady at their March meeting and had signaled one cut remained possible in 2026. The March payrolls number effectively extends that pause, giving the central bank room to watch how oil prices and a deteriorating geopolitical picture play out before acting. Multiple analysts now predict no cuts at all this year. That judgment carries direct consequences for borrowers: mortgage rates tied to Treasury yields, already elevated, are unlikely to ease soon, and revolving credit card debt continues to accrue at rates that reflect a Fed in no hurry.

One important caveat shadows the entire report: the BLS survey period closed on March 12, before the full economic weight of escalating tensions in the Middle East registered in hiring decisions. Gas prices have since surged past $4 a gallon, and the Atlanta Federal Reserve has cut its real-time GDP growth estimate to 1.9 percent, down from more than 3 percent just weeks ago. The March jobs report captures a snapshot of an economy that may already look different than it did when the data was collected.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?