Middle East War Disruptions Trigger Global Aluminum Supply Shock

War damage in the Middle East has jolted aluminium to a four-year high, with traders warning of a 2 million-ton deficit and shortages in cans, cars and construction.

Aluminium prices have surged into territory that is now forcing manufacturers, traders and analysts to ask the same question: is this a temporary price spike, or the start of a genuine supply emergency? The answer is leaning toward emergency. Nick Snowdon, Mercuria’s head of metals and mining research, described the shock as a black swan event and said the market could face a deficit of at least 2 million tons between now and the end of 2026.

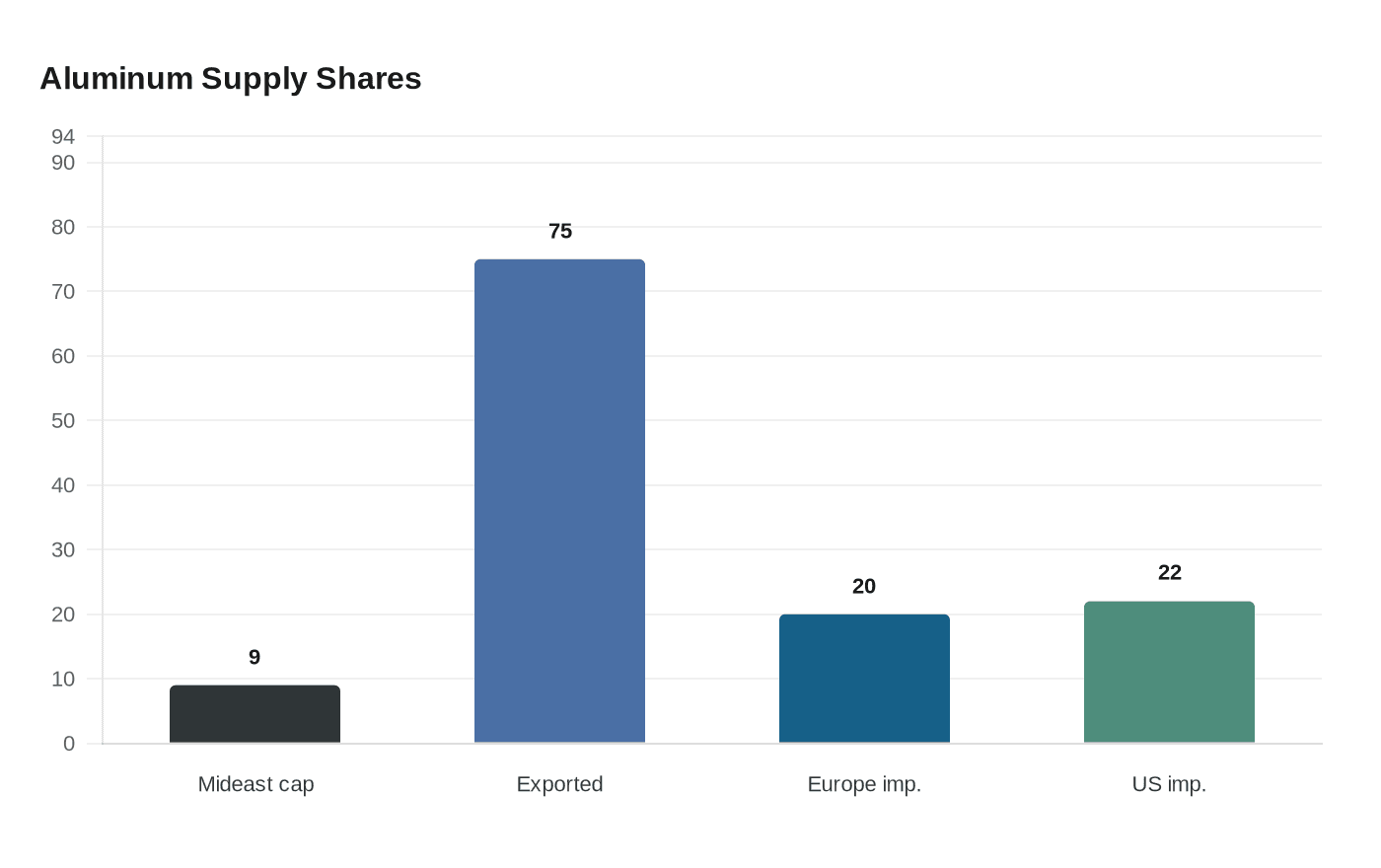

The disruption centers on the Middle East, where about 7 million metric tons of annual smelting capacity represents roughly 9% of global supply. About 75% of that production is exported, which is why damage and transport disruption in the region can reverberate from canning lines and auto plants to building-material suppliers and cable makers thousands of miles away. Europe imported about 1.2 million tons of aluminium from the Middle East and Egypt last year, or roughly 20% of its primary and alloyed imports. The United States bought nearly 3.4 million tons, close to 22% of its total.

The strain is no longer theoretical. Aluminium Bahrain shut three smelting lines in early March, affecting 19% of capacity, and Emirates Global Aluminium said its Al Taweelah plant sustained significant damage in the Iranian strikes. EGA produces around 2.7 million metric tons of primary aluminium each year in the UAE, making the hit especially significant for global buyers trying to replace supply quickly. With the Strait of Hormuz closed and shipments already restricted to export markets in the U.S. and Europe, industrial customers have been left with fewer immediate alternatives.

Market pricing shows how quickly the squeeze has traveled. On April 16, London Metal Exchange aluminium hit a four-year high of $3,672 a ton, after touching $3,492 on March 30. European physical premiums climbed to $469 a ton last week, up $120 since the war began on February 28. Those moves matter because they feed directly into costs for beverages, vehicles, homes and factory equipment, and because aluminium production itself is energy-intensive, making European smelters more vulnerable when gas prices stay high.

S&P Global Energy estimated that the world produced 73.8 million metric tons of primary aluminium in 2025, including 29.6 million tons of non-Chinese supply, and said just over 23% of that non-Chinese output came from the Middle East. With visible aluminium inventory at about 1.5 million tons and total global stock a little above 3 million tons, the market has little cushion if the conflict keeps disrupting power, shipping or plant operations. Some analysts see possible relief from restarts in Iceland and Slovakia and from new projects in Indonesia, but those are longer-term offsets, not immediate fixes. For now, the shock looks less like a trading story than a stress test for global manufacturing.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?