Missed Credit Card Payments? Act Quickly, Experts Say to Avoid Collections

The fastest way to limit damage is to call your creditor first, not a debt-settlement marketer. The wrong move can trigger fees, collection pressure, and scams that make the hole deeper.

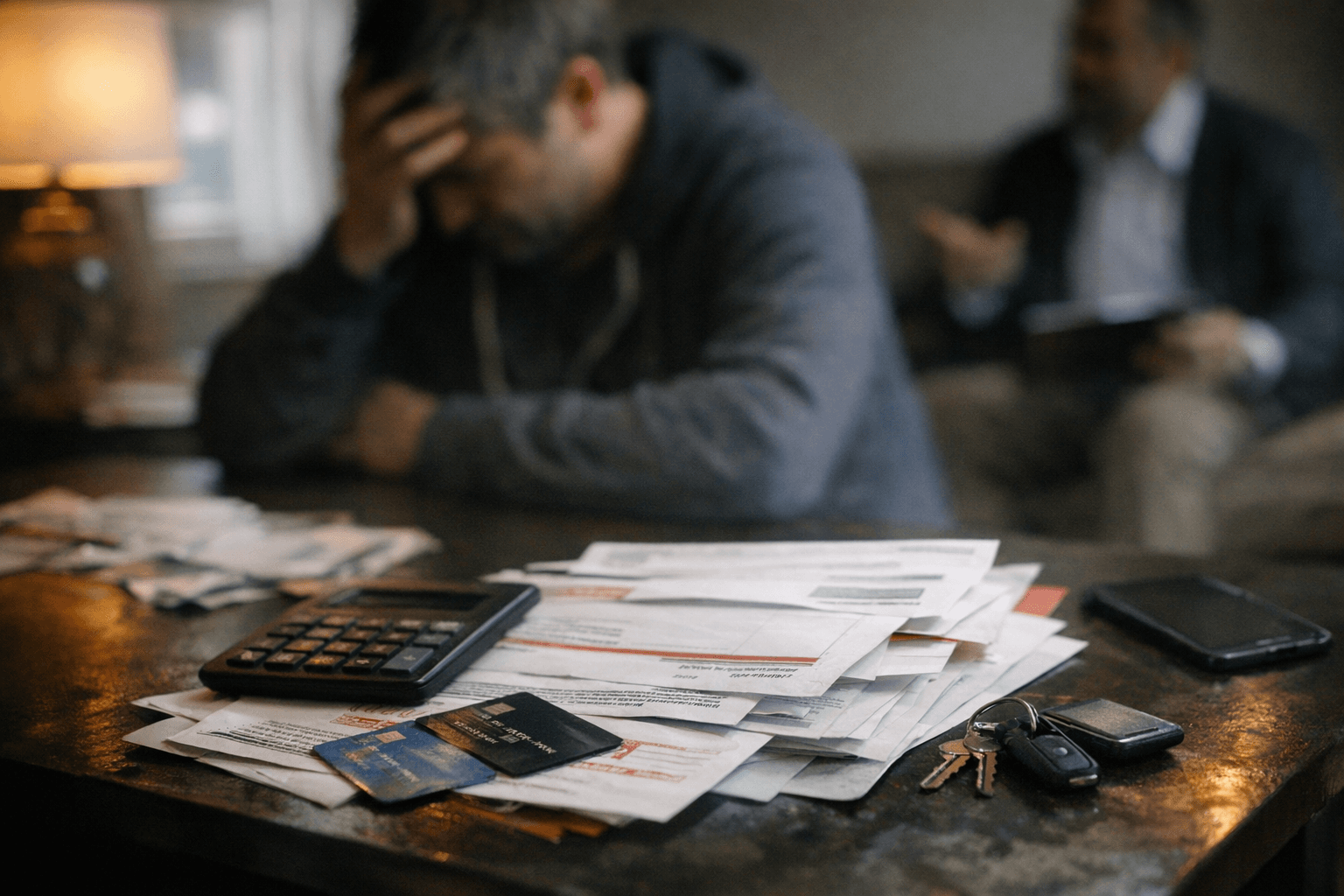

Act first, before a missed payment becomes a collections problem

Missing a debt-relief or credit card payment is not the end of the road, but it is a point where delay gets expensive fast. The Consumer Financial Protection Bureau says many people fall behind because they cannot cover monthly debt payments on top of daily living expenses, and the practical response is immediate contact, not silence. The least damaging move is to reach out to your credit card company right away, explain why you cannot pay the minimum, say how much you can afford, and give a realistic date when normal payments might restart.

That matters because the CFPB says missed payments can lead to late fees, penalty interest, more aggressive collection efforts, and even lawsuits. The Federal Trade Commission gives the same core advice: if you are having trouble making ends meet, contact creditors immediately and try to work out a modified payment plan before an account is handed off to collectors. In this space, speed is a form of damage control.

The first 7 days: stabilize the account and avoid the worst credit damage

If you have already missed a payment, the first week is about stopping the problem from spreading. Start with the creditor, not a settlement company, and ask whether there is a short-term accommodation, a modified payment plan, or another way to keep the account from escalating. The FTC specifically says to tell creditors why it is difficult for you and to try to work out a modified payment plan.

Use those calls to build a budget at the same time. The FTC says a budget can show where your money goes and how you might spend it differently, while the CFPB says nonprofit credit counseling organizations can help you develop one. If you can assemble a small, realistic payment, even a partial one, it is usually less harmful than disappearing from the creditor’s view and waiting for the account to worsen.

What to do right away

• Call the credit card company immediately. • Say why you cannot pay the minimum. • State the amount you can pay now. • Give a date when you expect to resume normal payments. • Ask whether the account can be placed on a modified plan before it gets harder to fix.

The first 30 days: compare nonprofit counseling with high-risk debt settlement

By the 30-day mark, you need a plan that addresses both the debt and the monthly budget. The CFPB says credit counseling organizations are usually nonprofits that can help you build a budget, develop debt management plans, and offer money management workshops. The National Foundation for Credit Counseling says a debt management plan is not a loan, which is important because it means you are entering a structured repayment arrangement, not taking on another credit product.

This is the point where many people become vulnerable to debt settlement sales pitches. The CFPB says debt settlement companies often tell consumers to stop paying credit card bills, which can add fees, penalty interest, and collection pressure. That advice can also make creditors less willing to cooperate, and some may refuse to work with the company at all. If a company’s strategy depends on you paying them while ignoring your creditors, the odds are high that it will worsen your position before it improves anything.

The safest comparison set is straightforward: creditor renegotiation, a nonprofit debt management plan, debt consolidation if it fits your circumstances, or bankruptcy if your debts are unmanageable. The CFPB’s point is not that one solution fits everyone; it is that stopping payment and hoping for the best is usually the most expensive path.

How to spot a debt-relief company that is making things worse

Warning signs include: • Telling you to stop paying creditors without a clear, credible plan. • Charging fees while promising fast relief that sounds too easy. • Promising results before it has reviewed your full budget and debts. • Pressuring you to sign before you have spoken with a nonprofit counselor or your creditors. • Suggesting that missed payments are harmless when the CFPB says they can trigger fees, collection efforts, and lawsuits.

The first 60 days: decide whether the problem needs restructuring, not just negotiation

If you are still behind after two months, the question is no longer whether you can “catch up” in a simple way. It is whether your debt load requires a more durable restructure. Nonprofit counseling can still be useful here because a debt management plan may lower and organize payments in a way that fits your budget. Debt consolidation may also make sense in some cases, but only if the new terms improve your monthly cash flow rather than just rearrange the debt.

At this stage, the hardest but sometimes necessary option is bankruptcy. The research notes do not make it the default answer, and neither should you. But if the monthly burden is so heavy that you cannot pay for debt and basic living costs at the same time, the CFPB’s description of why people fall behind suggests that a deeper reset may be more realistic than a series of temporary fixes. The key is to choose the least damaging tool that actually matches the size of the problem.

Why debt settlement is the option that needs the most scrutiny

Debt settlement is often marketed as a shortcut, but the CFPB and FTC both warn that the industry has a long history of abuse. The FTC says debt relief and credit repair scams are common enough that it has brought scores of law-enforcement actions and worked with states on hundreds of additional lawsuits. It also amended its Telemarketing Sales Rule in 2010 to protect consumers seeking debt relief services, which shows how long regulators have been watching this market.

That history is not abstract. In July 2024, the FTC said it stopped operators of a student-loan debt relief scheme that targeted financially strapped consumers, including Spanish-speaking consumers in Puerto Rico, and promised false low fixed payments and loan forgiveness. The lesson is blunt: when money is tight, polished sales language can disguise a plan that drains cash while doing little to reduce debt.

The practical rule: pay the creditor, not the hype

If you cannot afford the payment, the least harmful path is still the most direct one. Contact the creditor immediately, build a budget, and use a nonprofit counselor before you agree to stop paying or sign up for a fee-based program that depends on delay. The CFPB and FTC both point to the same anchor: early contact, honest numbers, and a modified payment plan can preserve more options than panic or silence.

A missed payment does not have to turn into collections. But after 7, 30, and 60 days, the cost of waiting rises fast, and the wrong debt-relief company can turn a temporary setback into a longer, more expensive crisis.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?