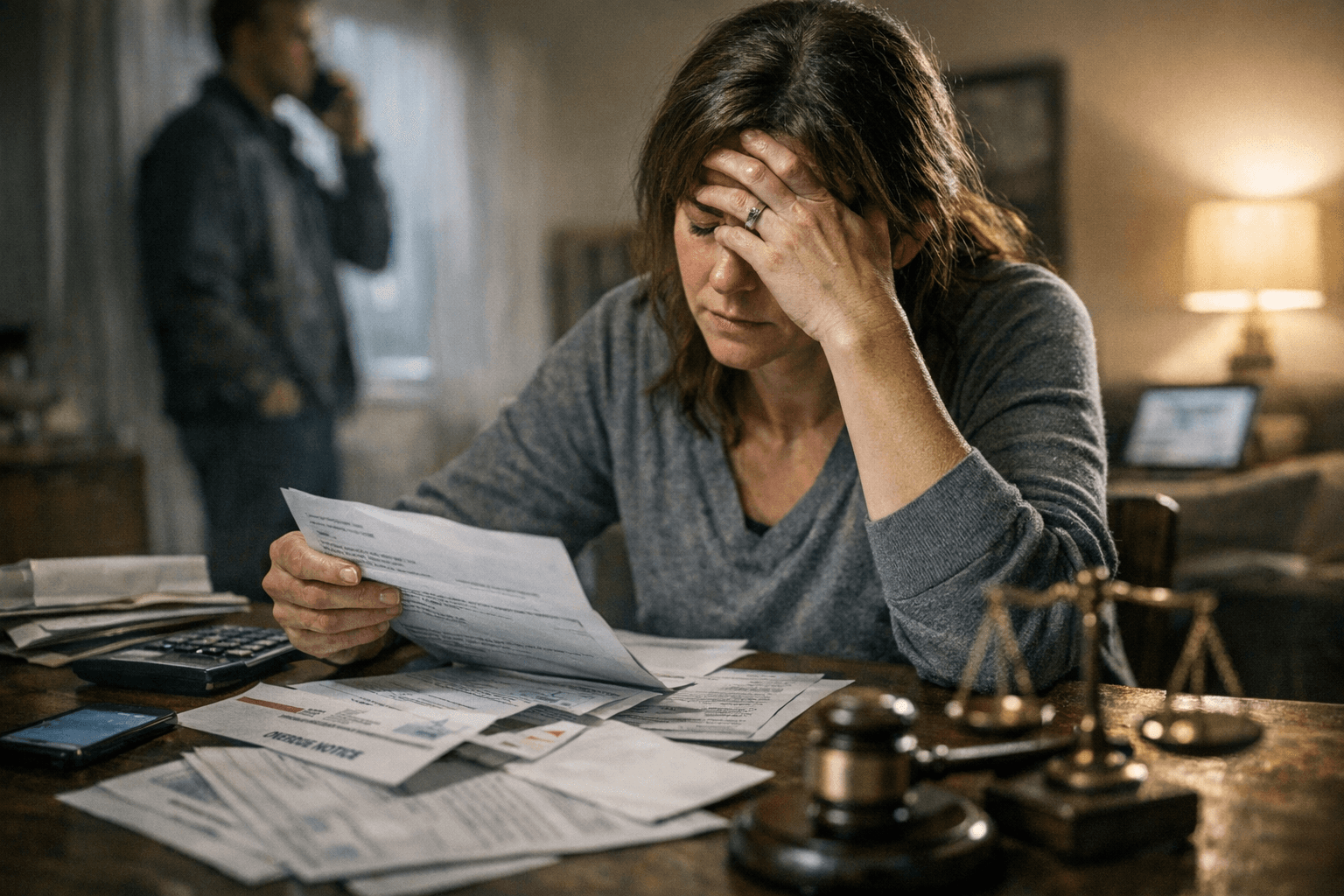

Missing debt settlement payment can trigger fees, lawsuits, and credit damage

One missed debt settlement payment can snowball into more fees, collection calls, lawsuits, and deeper credit damage, even before a deal is completed.

How debt settlement can put you behind

Debt settlement is often sold as a way to shrink what you owe, but the setup itself carries risk. These programs often ask or encourage you to stop sending payments directly to your creditors, and that can quickly lead to late fees, penalties, and extra interest that keep the balance growing while the program is underway.

The Consumer Financial Protection Bureau says debt settlement companies may also steer you into a dedicated bank account, usually managed by a third party, where you save money for future settlements. That account can come with its own fees, and the arrangement does not guarantee that a creditor will accept the offer you eventually make. In other words, you can pay into the program, still fall behind, and still end up owing the full balance if the creditor rejects the deal.

What one missed payment can trigger

Missing a payment inside a debt settlement plan is not just a paperwork problem. It can be the point where the account moves further into delinquency, additional fees pile up, and collection pressure intensifies. The Federal Trade Commission warns that debt settlement and similar agreements can negatively affect your credit report and credit score, and that late payments or settling for less than you owe can damage credit for as long as the service is affecting the debt.

The bigger risk is that the debt does not disappear just because you enrolled in a settlement program. Unpaid balances can continue to accrue fees and interest, creditors can still try to collect the full amount, and a creditor can still sue. The CFPB specifically warns that working with a debt settlement company may lead to a debt collection lawsuit.

Why the promises do not match the real-world fallout

Debt settlement companies often talk about reduced balances and a cleaner way out of debt, but the legal and financial exposure remains until a creditor actually agrees to accept less than you owe. That matters because a creditor is not obligated to accept a settlement offer at all. If the offer is rejected, the debt survives, the fees may keep running, and the consumer can be left with both a damaged credit file and a larger bill than expected.

That is why a missed payment inside the program can become more damaging than a missed payment on a regular bill. You may already have stopped paying creditors directly, which means you have fewer buffers if the settlement account falls short or the company’s timing is off. The consequence is a widening gap between what the program promised and what the debt collector or creditor is actually allowed to do.

What rights you still have if collectors get involved

Federal debt collection rules still apply even when you are in a settlement program. Under the FTC’s guidance, debt collectors must provide validation information about the debt, which gives you a basic way to confirm who says you owe the money and how much they claim is due. You can also ask collectors to stop contacting you in writing, though that does not erase the debt itself.

That distinction matters. Stopping contact can reduce the immediate pressure, but it does not prevent a lawsuit, does not cancel interest already added, and does not force a creditor to accept a settlement. If the debt is valid and still within the collection window, the account can continue to move through collection channels even after a consumer tries to slow the calls.

Why timing matters if you miss a payment

A missed payment can also affect the legal clock on a debt. The FTC says the statute of limitations for debt collection generally starts when a payment is missed, although the exact length depends on state law or the contract. That means the date of the missed payment can become important later if a collector tries to sue.

This is one reason consumers in debt settlement should keep careful records of every payment, missed payment, notice, and collector contact. A delay of days or weeks can change the balance, the collection strategy, and the legal posture of the account. If a lender or collector later claims the debt is still collectible, the missing-payment date may be one of the first facts disputed.

What can be fixed quickly, and what cannot

Some of the fallout from a missed settlement payment can be reduced if you act quickly. Catching up on the payment, getting back into the dedicated account, or completing a negotiated settlement may help stop the problem from growing further. But other consequences are harder to undo. Late fees, penalties, interest, and collection activity can continue while the account is unresolved, and credit damage may remain visible for the duration of the service.

The practical priority is to respond before the account hardens into a lawsuit or a deeper collection file. Once a creditor decides to pursue the full balance, the consumer may face not only the original debt but also added fees, legal costs, and the strain of defending the claim.

Why regulators keep policing the industry

Federal regulators have been especially wary of debt relief sales by phone. In 2010, the Federal Trade Commission amended the Telemarketing Sales Rule to require for-profit debt relief sellers that market by phone to disclose key terms, bar misrepresentations, and prohibit upfront fees before debts are actually settled or reduced. That rule exists because the harm from deceptive debt relief can be immediate: consumers pay for a service that has not yet delivered the promised result.

Recent enforcement shows the risk remains real. In December 2024, the FTC announced more than $540,000 in refunds for consumers harmed by abusive debt collectors who threatened lawsuits or arrest. In April 2026, the agency announced a temporary restraining order against NERD Solutions over alleged student-loan debt relief claims and illegal upfront fees. Those cases underscore a basic warning for anyone already stretched thin: if the program is poorly explained, deceptive, or tied to a company that does not follow the rules, a missed payment can become the trigger for a much bigger financial mess.

Bottom line

A missed debt settlement payment can do more than dent a plan, it can restart the old debt’s momentum. Fees can grow, credit can take another hit, collection rights can survive, and a lawsuit can still land on your doorstep if the account is not handled fast and carefully.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?