Mortgage rates hover in the mid-6% range as buyers weigh options

Mid-6% mortgage rates still buy a home, but they also buy a much larger payment than most borrowers expect. The key question now is not whether rates are high, but whether your budget can survive them.

The mortgage market is stuck in a zone that feels manageable only until you run the payment math. A 6.3% to 6.7% 30-year loan may look close to last week’s quote, but on a real mortgage it can decide whether a purchase works, whether a refinance saves money, and whether waiting for a lower rate is worth the risk.

What a mid-6% rate means for your monthly bill

At Fortune’s 6.395% average for a 30-year fixed conforming mortgage, a $300,000 loan works out to about $1,876 a month in principal and interest. Bankrate’s 6.46% national average pushes that to roughly $1,889, while Bankrate’s 6.71% refinance average lands near $1,938. That gap may look small on paper, but it is close to $60 a month between the lower and higher ends of today’s mainstream quotes, or more than $700 a year.

The longer-term cost is even more revealing. Fortune estimated that a $300,000 mortgage at 6.395% would generate about $375,189.78 in total interest over the life of the loan. On a 15-year mortgage at 5.720%, the same loan would produce about $147,554.78 in total interest, but the monthly payment rises to roughly $2,488. That is the central tradeoff in this market: the 15-year loan is far cheaper over time, but only if your cash flow can handle the higher monthly hit.

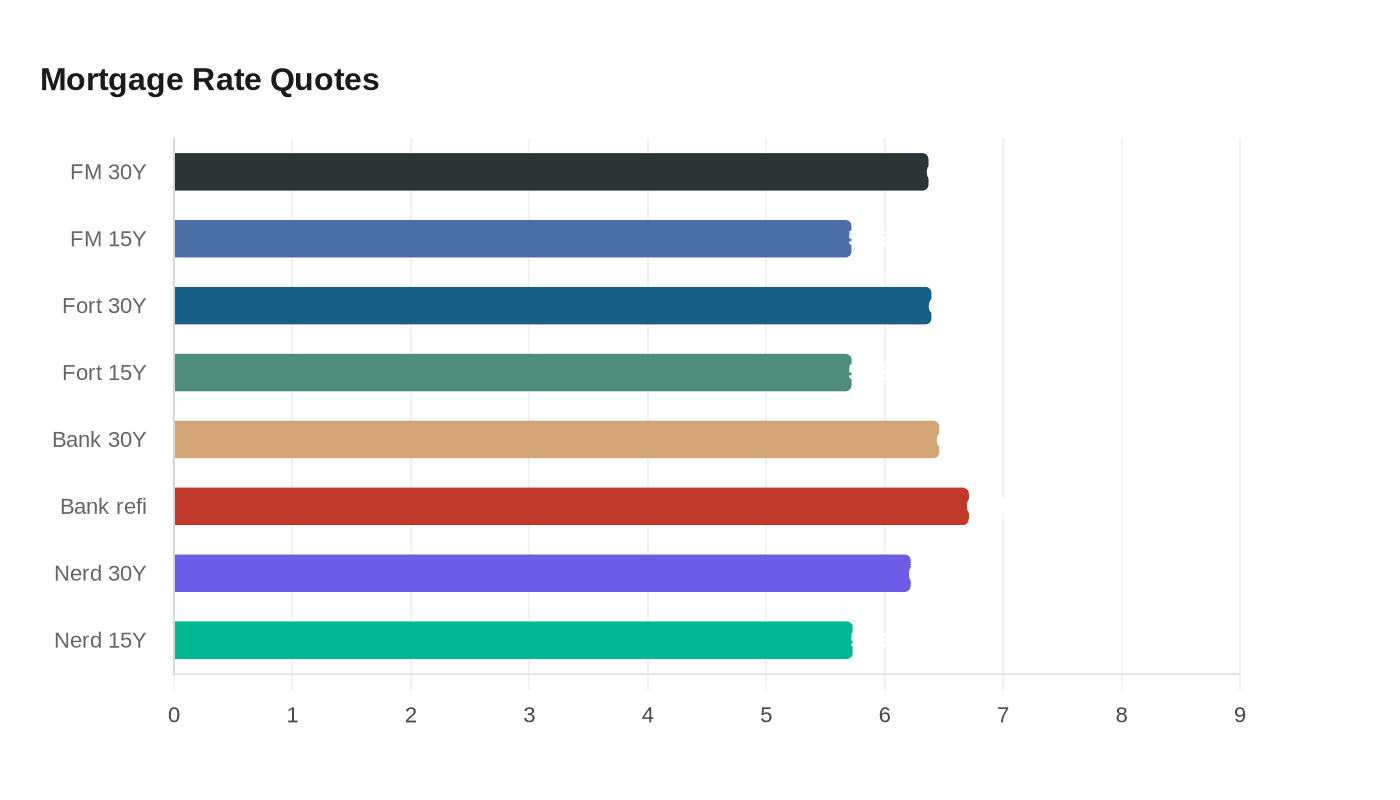

Why the headlines show slightly different rates

Mortgage rate trackers are not all measuring the same thing, which is why the numbers sit close together but do not match exactly. Freddie Mac’s Primary Mortgage Market Survey said the 30-year fixed mortgage averaged 6.37% and the 15-year fixed averaged 5.72% for the week ending May 7, 2026. Freddie Mac said those weekly figures are based on thousands of loan applications submitted through Loan Product Advisor from lenders across the country, and the results are released on Thursdays at 12 p.m. ET.

Fortune, using Optimal Blue loan-lock data, reported a 30-year fixed conforming rate of 6.395% and a 15-year fixed conforming rate of 5.720% for May 14, 2026. Bankrate’s national survey of large lenders put the average 30-year fixed mortgage at 6.46% and the average 30-year fixed refinance rate at 6.71% on the same day. NerdWallet’s figures were lower still on an APR basis, at 6.22% for a 30-year fixed and 5.73% for a 15-year fixed. That spread is a reminder that APR and note rate are not interchangeable, and that lender fees can change the real cost of borrowing.

The market is better than 2023, but still far from cheap

Borrowers are still paying well above the sub-3% rates of 2020 and 2021, yet the direction has improved from the worst of the recent cycle. Freddie Mac said the 30-year rate was 6.37% on May 7, 2026, down from 6.76% a year earlier. The 52-week range for Freddie Mac’s 30-year rate was 5.98% to 6.89%, which shows how narrow the market’s recent band has been even after months of volatility.

There are also some signs that housing conditions are slightly less punishing than they were a year or two ago. Freddie Mac pointed to stronger new-home sales, median new-home prices falling to their lowest level since July 2021, and higher inventory than in recent years. That does not make the market easy, but it does mean buyers have a little more negotiating power than they did when supply was tighter and pricing was running hotter.

Who should lock now

If you are a first-time buyer with a stable job, a solid emergency fund, and a payment that still works at today’s rates, locking now can make sense. The reason is simple: a house that fits the budget at 6.4% may be scarce, and waiting for a much lower rate could mean competing in a hotter market if rates do ease. Mid-6% rates are not a bargain, but they are also not a reason to freeze a purchase that already pencils out.

Fixed-rate borrowers who care more about certainty than timing should also lean toward locking. A 30-year mortgage near 6.4% gives you a known payment in a market where inflation, Federal Reserve policy, and geopolitical risk are still pushing expectations around. Bankrate’s May 14-20 expert poll found 64% expecting rates to rise, 18% expecting them to stay the same, and 18% expecting them to fall, which suggests the near-term bias is not especially friendly to borrowers hoping for a quick drop.

Who should wait

Refinancers should be more selective. Bankrate’s national average 30-year fixed refinance rate was 6.71%, which is high enough that many existing homeowners will not see enough savings to justify closing costs unless their current mortgage is well above today’s levels. If you already hold a low-6% loan or anything below that, waiting is usually the more rational choice unless you need to shorten your term, remove mortgage insurance, or tap equity for a specific purpose.

Homeowners deciding whether this is the new normal should also keep the policy backdrop in mind. Forbes Advisor said mortgage rates spent much of 2025 in the upper-6% range because of persistent inflation and a cautious Federal Reserve, then eased after the Fed began cutting rates in September 2025. But the central bank paused at its January, March, and April 2026 meetings while weighing low job gains, elevated inflation, little change in unemployment, higher global energy prices, and uncertainty tied to Middle East conflict. That combination suggests rates may drift lower over time, but not quickly enough to revive the pandemic-era era of ultra-cheap borrowing.

Which loan types deserve a closer look

Today’s range also rewards borrowers who compare programs instead of fixing on one headline number. Fortune reported a 30-year jumbo mortgage at 6.550%, a 30-year FHA mortgage at 6.186%, a 30-year VA mortgage at 5.957%, and a 30-year USDA mortgage at 6.070% on May 14, 2026. For eligible borrowers, those government-backed options can offer meaningful savings versus a standard conventional loan, even before you factor in the different down payment and insurance requirements.

The refinance market shows the same pattern. Bankrate’s table put the 15-year fixed refinance average at 6.07%, the 30-year FHA refinance average at 6.61%, and the 30-year VA refinance average at 6.52%. If you qualify for those programs, the lower rates can improve the case for refinancing, but the real question remains whether the monthly savings and long-term interest savings outweigh closing costs.

The bottom line

A mid-6% mortgage is not a catastrophe, but it is not soft enough to ignore the budget math either. For buyers, the right move is to focus less on the headline rate and more on whether the monthly payment still leaves room for maintenance, taxes, insurance, and life itself. For refinancers, the threshold for action is higher. Unless your current rate is clearly worse than today’s averages, waiting may be the more disciplined choice while the market slowly searches for a lower floor.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?