Most Americans lose key ACA sign-up window as costs rise

Open enrollment for most ACA plans has closed, leaving millions facing much higher premiums and uncertainty about whether federal subsidies will return.

Open enrollment for Affordable Care Act marketplace plans has closed in most states, officials say, leaving millions of Americans to confront substantially higher premiums for 2026 and uncertainty about whether federal subsidies will be restored.

Federal open enrollment for 2026 ran from November 1, 2025, through January 15, 2026, according to Blue Cross and Blue Shield materials. After January 15, consumers can enroll or change plans only if they qualify for a Special Enrollment Period. Several jurisdictions set different windows: California, New Jersey, New York, Rhode Island and Washington, D.C. extended their deadlines through January 31; Massachusetts extended through January 23; Idaho ran an earlier window from October 15 to December 15, 2025. About ten states that operate their own marketplaces also offered later or extended deadlines to give residents extra time.

Interim federal data released in the run-up to the deadline produced differing tallies of enrollment. One federal release showed roughly 22.8 million Americans had signed up for 2026 coverage at that point, about 800,000 fewer than at a comparable point last year, a decline of roughly 3.5 percent. Another federal metric indicated enrollment was down by about 1.4 million from last year. Last year marked a record enrollment year, with roughly 24 million people purchasing marketplace plans, and officials warned that enrollment could shrink further as consumers react to cost increases.

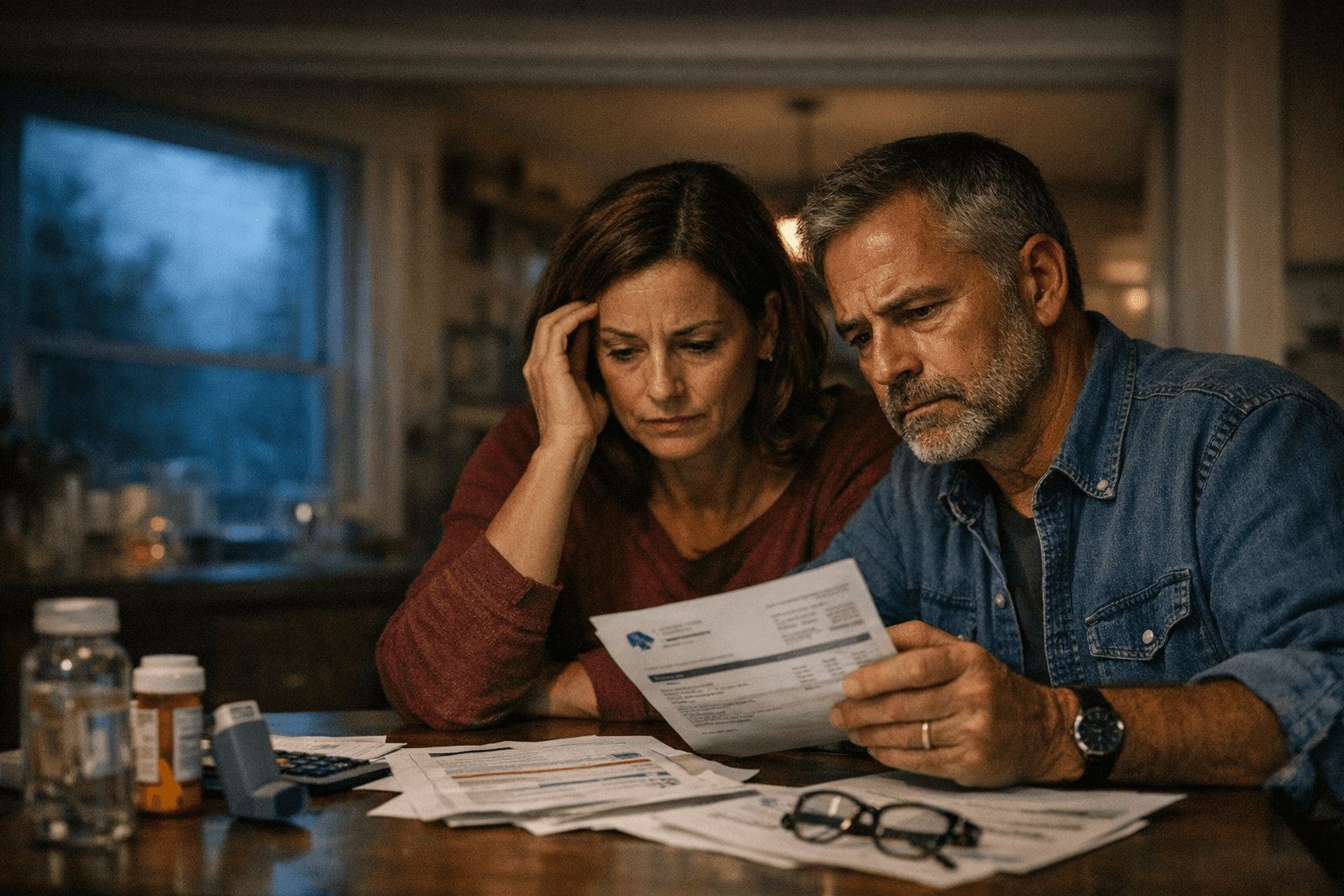

The primary driver of higher costs is the expiration, on January 1, 2026, of COVID-era expansions to premium tax credits. Analysis by the Kaiser Family Foundation indicates that the average subsidized enrollee would face more than double their monthly premium in 2026 compared with 2025. Without renewed federal tax credits, more than 20 million people who received enhanced subsidies could see sharp jumps in monthly premiums, straining household budgets and testing state safety nets.

The subsidy lapse has shaped consumer behavior during the enrollment window. Many people delayed signing up or enrolled tentatively while awaiting signals from Congress about a possible deal to extend assistance. Some consumers enrolled with the intention of canceling later if lawmakers did not act. State officials in several jurisdictions said they were considering measures to help residents, though the extent and specifics of state-funded assistance varied and remained incomplete as deadlines closed.

The fiscal and political standoff in Washington left little prospect for immediate relief at the close of enrollment. Lawmakers remained divided over whether to revive the expanded credits, and the White House indicated a willingness to veto certain proposals. Political uncertainty compounded the market disruption, as insurers and state marketplaces struggled to anticipate enrollment and claims patterns for the year ahead.

Consumers left out of the open window can still enroll if they qualify for special circumstances such as job loss, family changes, or other life events. Residents in states that extended their deadlines have additional time to shop. For millions of others, the confluence of higher premiums and unresolved federal policy means 2026 will bring steeper out-of-pocket costs and renewed pressure on states and Congress to find a fix.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?