Novo Nordisk tops first-quarter estimates, raises outlook amid obesity-drug rivalry

Novo Nordisk beat profit estimates, but its U.S. pricing squeeze and Lilly rivalry show the obesity boom is turning into a margin war.

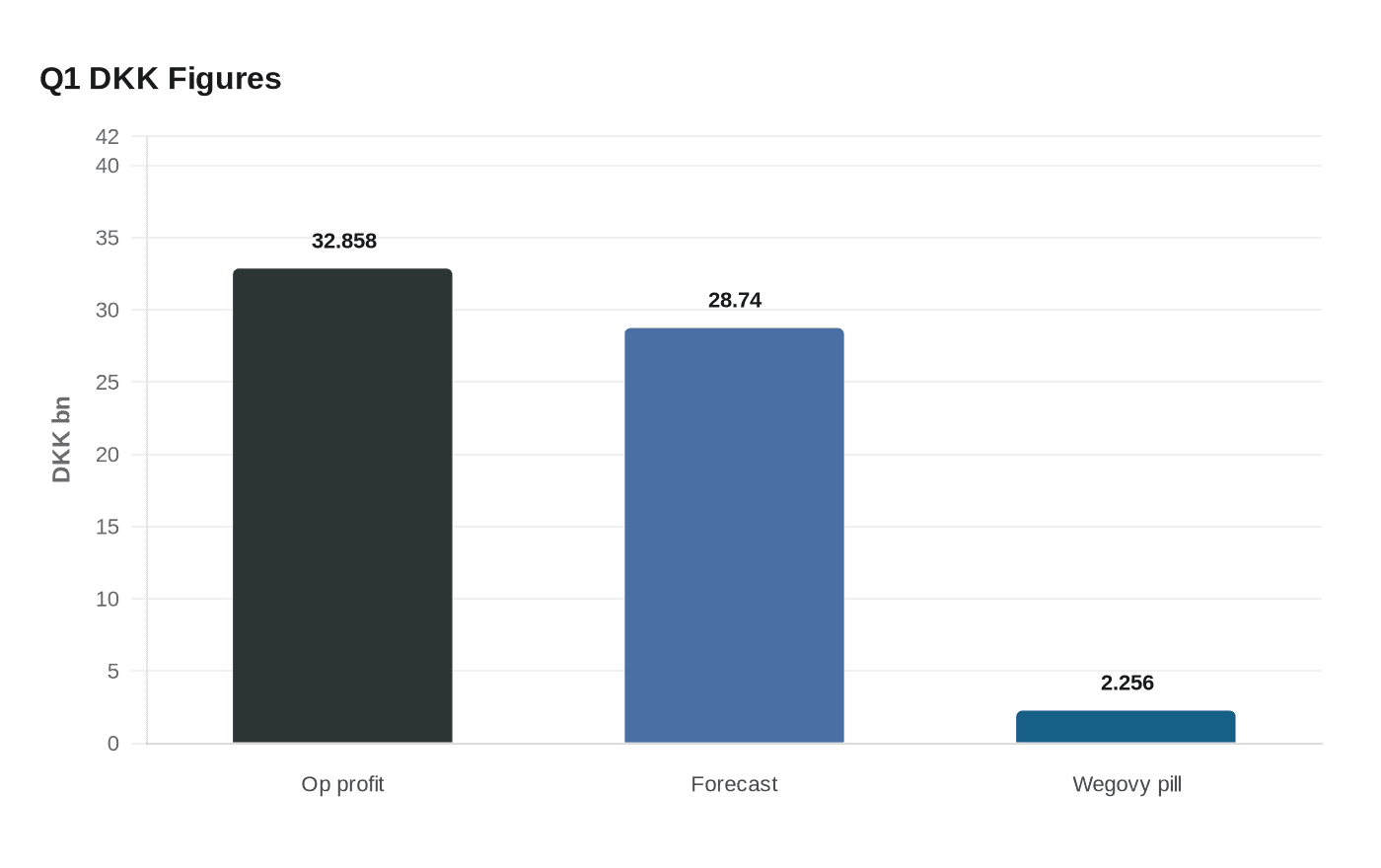

Novo Nordisk posted adjusted operating profit of DKK 32.858 billion in the first quarter, comfortably above the company-compiled forecast of DKK 28.74 billion, and nudged up its 2026 outlook as investors kept a close watch on the weight-loss market. The Danish drugmaker still has to prove that Wegovy and its new pill can keep driving growth as competition from Eli Lilly intensifies and the obesity-drug category moves from explosive expansion to harder price negotiation.

The cleaner read in the numbers was less flattering. Novo said reported sales rose 32% at constant exchange rates, but adjusted sales excluding a $4.2 billion 340B Drug Pricing Program reversal fell 4% at CER because lower realized prices partly offset GLP-1 volume growth. The company also raised its 2026 outlook while warning that, excluding the 340B reversal, adjusted sales growth for the year is now expected to land between minus 4% and minus 12% at constant exchange rates.

The strongest evidence of demand came from the Wegovy pill launch. Novo launched the oral version in the United States on 5 January, said weekly prescriptions topped 200,000 in the week ending 17 April, and said total prescriptions in the first quarter were about 1.3 million, with more than 2 million written since launch. Novo said first-quarter sales for the pill reached DKK 2.256 billion, though pre-launch pipeline fill with wholesalers and telehealth partners boosted that figure, and the first launches outside the United States are expected in the second half of 2026, pending regulatory decisions.

That is why the quarter matters beyond one earnings beat. Novo is trying to prove that obesity drugs can move from shortage-driven scarcity to a durable mass-market business, but that transition depends on supply, insurer coverage and pricing discipline as much as on clinical demand. If Eli Lilly keeps pressing and prices keep falling, the category can still grow fast while Novo’s margins narrow, which is exactly the trade-off investors are now trying to price.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)