Paramount Skydance Cuts Bridge Loan, Expands Bank Group for $111 Billion Deal

Paramount Skydance cut its bridge loan from $54 billion to $49 billion and spread the debt across 18 banks, racing to lock in permanent financing ahead of a WBD shareholder vote on April 23.

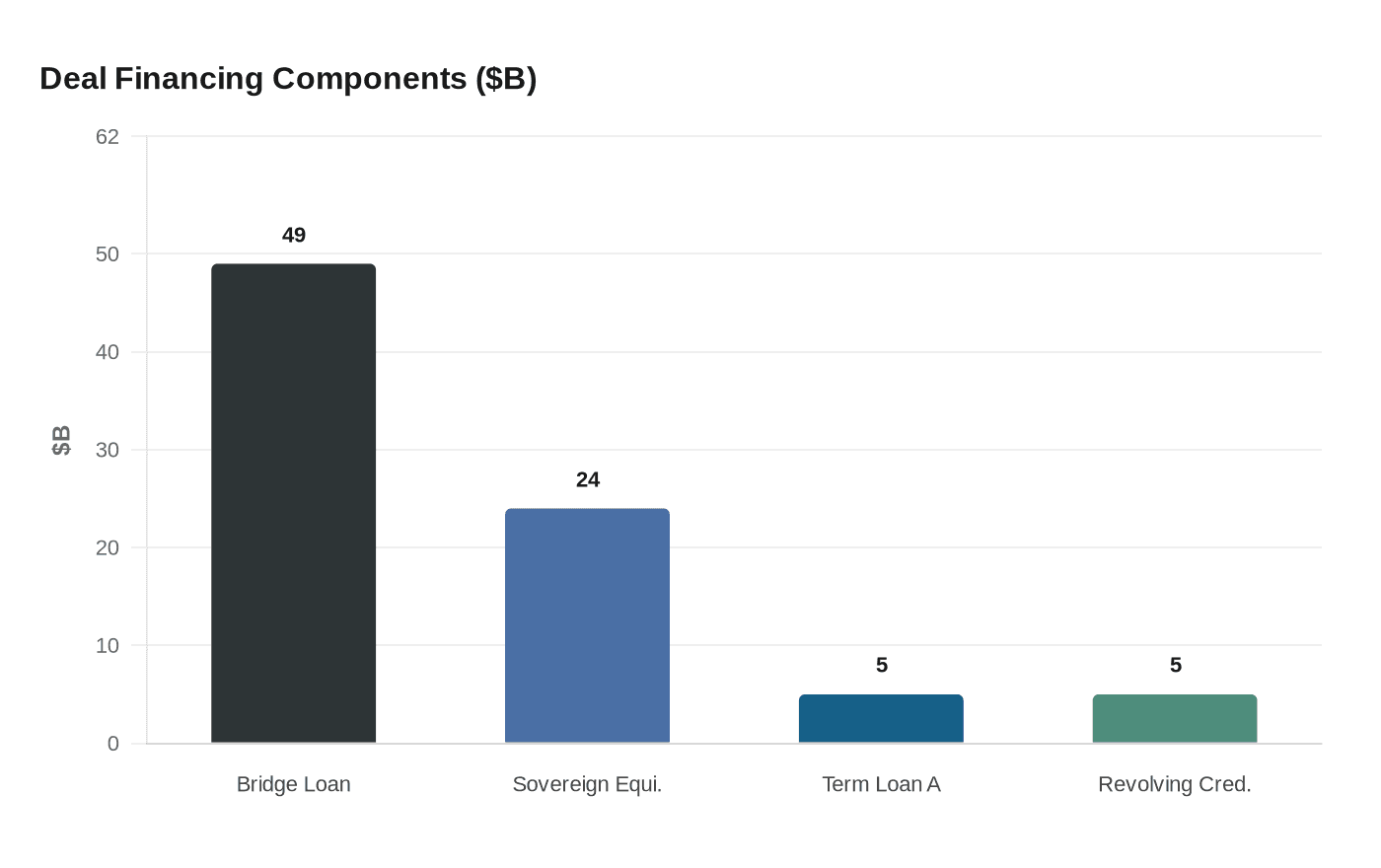

The size of the debt alone makes every financing move worth watching. Paramount Skydance's proposed $111 billion takeover of Warner Bros. Discovery would leave the combined company carrying $87 billion in total pro forma gross debt and nearly $80 billion in net debt, a leverage ratio of approximately 7 times projected 2026 EBITDA before synergies. That context is what gives Thursday's SEC filing its weight: Paramount restructured the bridge loan backing the deal, cutting it from $54 billion to $49 billion and spreading the exposure across 18 banks rather than concentrating it almost entirely with the original three lead arrangers, Bank of America, Citigroup, and Apollo Global Management.

The syndication reduces concentration risk at the top of the capital structure and provides a clearer signal of how broadly the lending market is willing to underwrite what would be the largest leveraged buyout in corporate history. Alongside the syndication, Paramount locked in a $5 billion Term Loan A and a new $5 billion revolving credit facility as permanent financing intended to sit inside the combined company's capital structure after the deal closes. A previously disclosed $3.5 billion revolving credit commitment was reduced to zero, replaced by the larger facility and an expanded $5 billion unsecured revolver. Latham & Watkins advised Paramount Skydance on the permanent financing component.

The calendar is pressing hard. Warner Bros. Discovery shareholders are scheduled to vote April 23, 2026, and Paramount has agreed to pay WBD $650 million per quarter for each quarter the deal fails to close beyond year-end. That penalty structure reflects how much closing certainty matters to the target's board and how much leverage lenders retain over the timeline. Any deterioration in the financing market or lender sentiment between now and close carries real cost.

Even with 18 banks distributed across the bridge, the debt covenants embedded in a package this size carry consequences for the combined company's operations. Loan documents at this scale typically include financial maintenance tests and cash flow restrictions that would constrain management's ability to accelerate spending on streaming, content acquisition, or distribution infrastructure during the paydown period. Rating agencies will scrutinize those provisions closely once full loan documentation becomes available.

The equity side of the financing adds further texture. Gulf sovereign wealth funds, including Saudi Arabia's Public Investment Fund with roughly $10 billion committed, along with sovereign funds from Qatar and Abu Dhabi, collectively brought close to $24 billion in equity to the deal. That cushion reduces the proportion of the $111 billion price covered by debt, but it does not change the leverage ratio that will govern the balance sheet from day one after close.

With the shareholder vote 13 days out, the reworked bridge and the 18-bank syndicate represent Paramount Skydance's most concrete response to skeptics who questioned whether the debt market would absorb an LBO of this magnitude in a higher-rate environment. Eighteen institutions now have skin in the answer.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?