S&P 500 rally faces test as hot inflation dims Fed rate-cut hopes

Hot April inflation jolted rate-cut bets just as the S&P 500 and Nasdaq extended six-week winning streaks and set records.

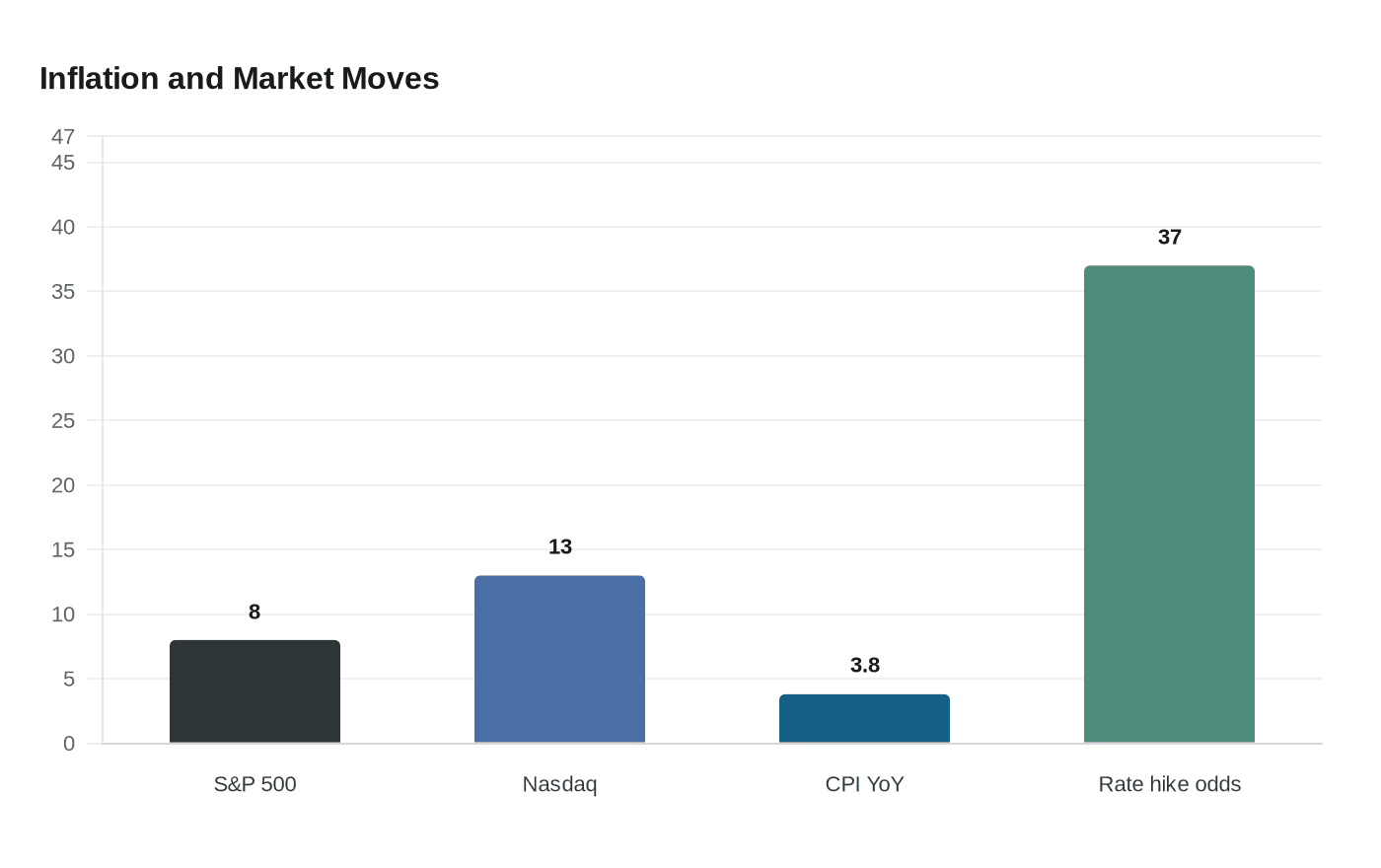

Wall Street’s rally kept climbing even as the macro backdrop turned less forgiving. The S&P 500 and Nasdaq had each logged six straight weekly gains in early May, their longest winning streak since October 2024, and both indexes had set record closing highs even after the latest inflation data showed prices were still running hotter than investors had hoped.

The April consumer price index rose 0.6% from March and 3.8% from a year earlier, according to the U.S. Bureau of Labor Statistics, the fastest annual pace since May 2023. Energy prices jumped 3.8% in the month and shelter climbed 0.6%, two of the biggest drivers behind the increase. That report immediately pushed traders to scale back expectations for Federal Reserve rate cuts and to price in a higher chance that the central bank could be forced to raise rates later in 2026.

Around noon on May 13, market pricing implied about a 37% probability of a rate increase before year-end. That shift matters because the S&P 500’s advance has depended on a delicate balance: strong corporate earnings and a resilient U.S. economy on one side, and the threat of tighter financial conditions on the other. Susan Collins, president of the Boston Federal Reserve, said rates may need to rise if inflation pressures do not ease.

The contradiction is clear. Investors have pushed the S&P 500 about 8% higher so far in 2026 and driven the Nasdaq up roughly 13%, even as hotter inflation makes it harder for the Fed to justify an easier policy path. Treasury yields could rise further if markets conclude rate cuts are off the table, which would put pressure on valuations that have already been lifted by optimism around technology and artificial intelligence shares.

Earnings have been doing much of the heavy lifting. FactSet estimated first-quarter 2026 S&P 500 earnings growth at 27.7%, which would be the strongest since the fourth quarter of 2021 if confirmed. That kind of profit growth has helped investors look through macro risk for now. The question is how long that can last if inflation stays elevated, the Fed stays on hold or turns more hawkish, and the market’s best-case assumptions start to fade.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)